What Is Commercial Property Insurance? A Guide

You’ve poured everything into your business. But what if a fire, storm, or break-in wiped out your physical assets overnight? Many business owners mistakenly believe their general liability or landlord’s policy has them covered. That’s a costly assumption. Those policies don’t protect your inventory, equipment, or office space. For that, you need dedicated Commercial Property Insurance. This guide breaks down exactly what it covers, how much it costs, and how to choose the right policy to protect your livelihood and long-term growth.

Ready to protect your business property? Get a free commercial property insurance quote today or call our team at 305-900-2823 for expert guidance.

What Is Commercial Property Insurance?

Commercial property insurance is a type of business insurance that protects company-owned buildings, equipment, inventory, furniture, and other physical assets against covered perils such as fire, theft, vandalism, and certain natural disasters. It is sometimes called business property insurance or commercial building insurance, and it forms the foundation of most commercial insurance programs. Learn more about inland marine insurance.

Unlike homeowners insurance, which covers personal residences, commercial property insurance is designed specifically for properties used in business operations. This includes owned buildings, leased spaces, and the business personal property inside them.

Most commercial property policies fall into one of two categories:

- Named-perils policies cover only the specific risks listed in the policy, such as fire, lightning, windstorm, hail, explosion, and theft.

- Open-perils (all-risk) policies cover any cause of loss that is not specifically excluded, providing broader protection.

Open-perils policies typically cost more but offer significantly greater peace of mind, especially for businesses in areas prone to hurricanes, flooding, or other unpredictable events.

Is It Different From a Business Owner’s Policy (BOP)?

Many small business owners encounter commercial property insurance as part of a Business Owners Policy (BOP). A BOP bundles commercial property insurance with general liability insurance at a discounted rate. However, businesses with higher property values, unique risks, or complex operations often need a standalone commercial property policy with higher limits and more tailored coverage.

What Does Commercial Property Insurance Cover?

Coverage for Your Physical Building

This covers the physical structure of your commercial building, including walls, roof, foundation, permanently installed fixtures, and building systems such as HVAC, plumbing, and electrical. If you own the building where your business operates, building coverage is essential.

Your Inventory, Equipment, and Furniture

BPP coverage protects the contents inside your commercial space, including:

- Office furniture, desks, and chairs

- Computers, servers, and IT equipment

- Inventory and raw materials

- Tools and specialized equipment

- Signage and decorations

This coverage applies whether you own or lease the space. If you are a tenant, your landlord’s insurance typically covers only the building structure, not your property inside it.

Coverage for Property Outside Your Building

Your commercial property insurance doesn’t stop at the front door. This coverage extends to protect other important assets on your premises, such as fences, detached outdoor signs, and even landscaping. These features are often the first thing a customer sees, and they represent a significant investment. A well-structured policy ensures that the property you rely on to secure your location and attract business is covered from physical damage or loss. This includes protection against common risks like storms, fire, theft, and vandalism, so you aren’t left paying out-of-pocket to replace a costly sign or rebuild a damaged fence.

Beyond the physical repairs, think about how damage to your property—both inside and out—can impact your ability to operate. If a fire or severe storm forces you to close temporarily, business interruption coverage becomes a financial lifeline. This essential protection, often added to a commercial property policy, helps cover lost income and ongoing expenses like rent, utilities, and payroll while your business gets back on its feet. It’s the component that bridges the gap between protecting your physical assets and ensuring the financial continuity of your entire operation, giving you the stability to rebuild without draining your cash reserves.

Recovering Lost Income After an Interruption

If a covered event forces your business to temporarily close, business income coverage replaces the revenue you would have earned during the shutdown period. It can also cover ongoing expenses like payroll, rent, and loan payments. This is often called business interruption insurance, and it can be the difference between surviving a disaster and closing permanently.

Covering Extra Costs to Stay in Business

This pays for additional costs incurred to keep your business running during and after a covered loss, such as renting a temporary workspace, expedited shipping for replacement equipment, or overtime labor to restore operations.

Coverage for Your Renovations and Improvements

If you lease your space and have made improvements, such as built-in shelving, upgraded flooring, or custom lighting, this coverage protects those investments. Without it, you could lose thousands in leasehold improvements after a fire or storm.

When Your Essential Equipment Breaks Down

Some policies include or offer optional equipment breakdown coverage, which pays for repairs or replacement when essential equipment like boilers, HVAC systems, electrical panels, or refrigeration units fail mechanically. This is especially valuable for restaurants, manufacturers, and healthcare facilities.

What Kinds of Damage Does Your Policy Cover?

A standard commercial property insurance policy typically covers loss or damage caused by:

- Fire and smoke damage — the leading cause of commercial property claims

- Windstorm and hail — particularly critical in hurricane-prone states like Florida

- Lightning strikes — which can destroy electrical systems and cause fires

- Explosion — including gas leaks and equipment malfunctions

- Theft and burglary — covering stolen property and break-in damage

- Vandalism — protecting against intentional damage to your property

- Vehicle damage — if a car crashes into your building

- Water damage from burst pipes — not the same as flood damage

- Civil unrest and riot — covering property destruction during unrest

Understanding Common Policy Exclusions

Understanding exclusions is just as important as understanding coverage. Standard commercial property policies generally do not cover:

- Flood damage — requires a separate flood insurance policy through FEMA’s National Flood Insurance Program or a private insurer

- Earthquake damage — requires a separate earthquake policy or endorsement

- Wear and tear — gradual deterioration is a maintenance issue, not an insurable event

- Employee theft — typically covered under a crime or fidelity bond

- Cyber attacks — data loss and system compromise require cyber liability insurance

- Intentional damage by the owner — insurance fraud is excluded and illegal

- War and nuclear hazard — standard exclusions in virtually all property policies

For Florida businesses, flood insurance is particularly important. Many commercial properties in Miami-Dade, Broward, and Palm Beach counties sit in FEMA-designated flood zones where flood insurance may be required by lenders.

Unsure what your business needs? Request a personalized commercial property insurance quote or call 305-900-2823 to speak with an advisor who can evaluate your specific risks.

Business Vehicles

While your commercial property policy protects the building your business operates in, it does not extend to the cars, trucks, or vans you use for work. If a company vehicle is damaged in an accident, stolen, or vandalized, you’ll need a separate commercial auto insurance policy to cover the costs. This specialized coverage is designed to protect company-owned or leased vehicles, helping pay for repairs, replacement, and legal fees related to accidents involving your business vehicles.

Employee Injuries

Commercial property insurance is designed to protect physical assets, not people. If an employee is injured on the job—whether they slip and fall in the office or get hurt while operating machinery—your property policy will not cover their medical bills or lost wages. This is the specific role of workers’ compensation insurance. This coverage is legally required in most states and is essential for protecting your business from costly lawsuits while ensuring your employees get the care they need.

Tools and Equipment Used Off-Site

A standard commercial property policy provides excellent coverage for equipment and tools located at your primary business address. However, that protection often stops once the property leaves the premises. For businesses like contractors, photographers, or IT consultants who take valuable equipment to different job sites, this creates a significant coverage gap. To protect these assets while in transit or at a temporary location, you need inland marine insurance, which is specifically designed to cover mobile property.

Damage From Terrorism

Nearly all standard commercial property insurance policies include an exclusion for damage caused by acts of terrorism. While it’s an unsettling thought, businesses located in major urban centers or near high-profile landmarks may want to consider this risk. To secure protection, you must purchase a separate terrorism insurance policy. This coverage can typically be added as an endorsement to your existing policy and is a crucial consideration for a comprehensive risk management strategy.

How Much Does Commercial Property Insurance Cost?

The cost of commercial property insurance varies widely based on several factors. On average, small to mid-size businesses pay between $500 and $3,000 per year for a basic commercial property policy, but premiums can be significantly higher for larger properties, high-risk industries, or businesses in disaster-prone areas.

Average Costs and Common Policy Limits

While annual premiums vary, it can be helpful to break it down. Many small businesses pay an average of about $108 per month for commercial property insurance. Of course, the total annual cost can range from under $350 to over $15,000, depending on your property’s value, location, and industry risks. A primary factor that influences your premium is the coverage limit you choose. Most businesses select policies with a $1 million per-occurrence limit and a $2 million aggregate limit. This structure provides up to $1 million for a single covered event and a total of $2 million for all claims filed during the policy year, offering a solid foundation of protection for many small and mid-sized companies.

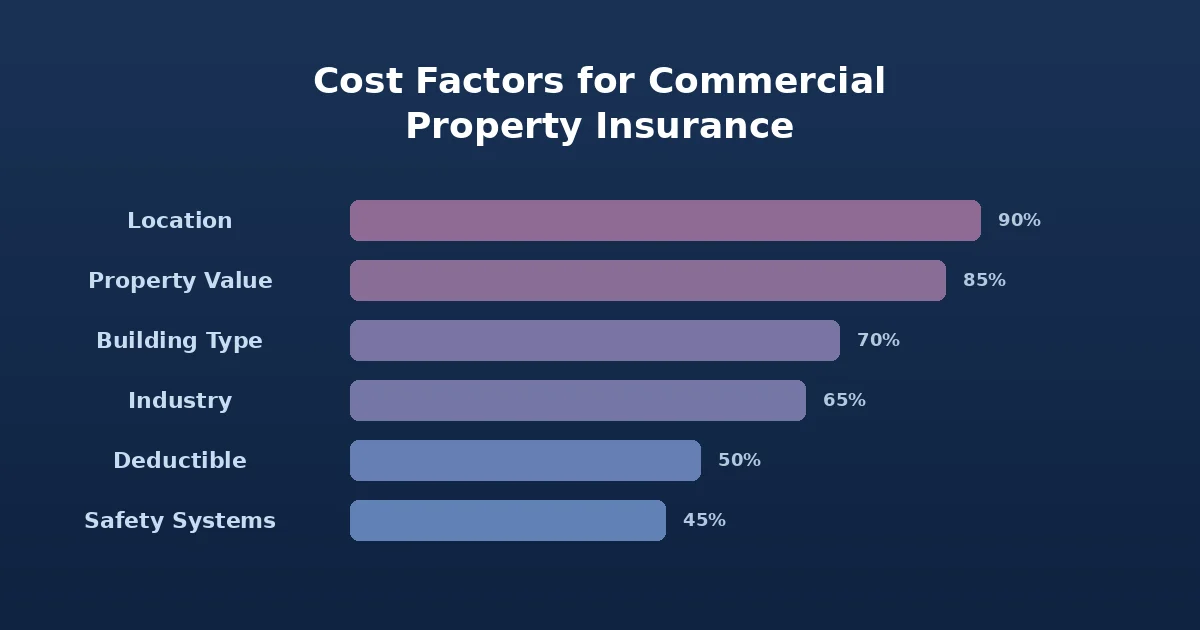

What Determines Your Insurance Premium?

| Factor | Impact on Cost |

|---|---|

| Property value and replacement cost | Higher property values mean higher premiums |

| Location and natural disaster risk | Coastal, flood-zone, and earthquake-prone areas pay more |

| Building age and construction type | Newer buildings with fire-resistant materials cost less to insure |

| Occupancy and business type | Restaurants and manufacturers pay more than office tenants |

| Security and safety systems | Alarm systems, sprinklers, and fire extinguishers reduce premiums |

| Claims history | A history of previous claims increases your rates |

| Deductible amount | Higher deductibles lower your monthly premium |

| Coverage limits and endorsements | Higher limits and additional riders add to the cost |

Your Proximity to a Fire Station

It might seem like a small detail, but your property’s distance from a fire station plays a surprisingly large role in what you pay for insurance. From an underwriter’s perspective, it’s all about response time. A business located just a few blocks from a fire station is likely to get help much faster than one in a remote area. This quick response can be the difference between minor smoke damage and a total loss, significantly reducing the insurer’s risk. As a result, carriers often reward this favorable location with lower premiums. This is considered a critical safety feature, much like having fire hydrants nearby. Similarly, investing in internal protections like modern sprinkler systems and monitored fire alarms can also help lower your cost by demonstrating a proactive approach to risk management.

Replacement Cost vs. Actual Cash Value: Which Is Right for You?surety bond and how it protects all parties involved. Actual Cash Value

When choosing a policy, you will encounter two valuation methods:

- Replacement cost pays to replace damaged property with new items of similar kind and quality, without deducting for depreciation. This is the recommended option for most businesses.

- Actual cash value (ACV) pays the depreciated value of the property at the time of loss. Premiums are lower, but payouts can be significantly less than what it costs to actually replace your assets.

For a business with $500,000 in property, the difference between replacement cost and ACV coverage could mean tens of thousands of dollars in out-of-pocket expenses after a major loss.

Replacement Cost Value (RCV)

Replacement Cost Value (RCV) coverage is designed to restore your business to its pre-loss condition without a financial penalty. This policy pays the full cost to replace your damaged property with new items of a similar kind and quality, and it does not subtract for depreciation. For most business owners, this is the smartest and safest option. While the premiums are slightly higher, an RCV policy ensures you have the capital needed to buy new equipment, rebuild your space, and get back to work quickly. Choosing RCV is a strategic decision that protects your cash flow and prevents a major property loss from turning into a long-term financial crisis. It provides the most complete commercial insurance protection for your physical assets.

Actual Cash Value (ACV)

An Actual Cash Value (ACV) policy pays for the replacement cost of your property minus depreciation. This means the insurance payout reflects the age and wear-and-tear of your assets at the time of the loss. For example, if a fire destroys your five-year-old computer system, an ACV policy would pay you the value of a five-year-old system, not the cost to purchase a new one. While this approach results in lower insurance premiums, it can create a significant financial gap when it’s time to rebuild. You would be responsible for covering the difference out-of-pocket, which can strain your resources and slow down your recovery. ACV might seem like a way to lower your business insurance cost, but the potential for high out-of-pocket expenses makes it a riskier choice for most businesses.

Who Needs Commercial Property Insurance?

Almost every business that owns or uses physical assets needs commercial property insurance. This includes:

- Retail stores and restaurants with inventory, equipment, and customer-facing spaces

- Office-based businesses with computers, furniture, and leased improvements

- Manufacturers and distributors with specialized machinery and raw materials

- Healthcare providers with expensive medical equipment

- Construction companies working with tools and materials on job sites (often paired with builders risk insurance)

- Real estate investors who own commercial rental properties

- Nonprofits and religious organizations with owned or leased facilities

If your business has a physical location, physical assets, or both, you need this coverage. Even home-based businesses may need a commercial property rider if their homeowners policy does not cover business equipment.

Is Commercial Property Insurance Legally Required?

Commercial property insurance is not legally mandated in most states. However, it is often effectively required because:

- Landlords typically require tenants to carry property insurance as a lease condition

- Lenders require property insurance on any building used as collateral for a commercial mortgage or loan

- Contracts with clients, vendors, or government agencies may specify minimum property insurance limits

- Common sense dictates that operating without coverage exposes your business to catastrophic financial risk

How to Choose the Right Commercial Property Insurance Policy

Choosing the right policy requires a clear understanding of your risks, assets, and business operations. Here is a step-by-step approach:

Step 1: Take Stock of Your Business Assets

Create a detailed inventory of everything your business owns or is responsible for. This includes the building (if owned), furniture, equipment, inventory, signage, and any improvements made to leased spaces. Document values with receipts, appraisals, or replacement cost estimates.

Step 2: Identify Your Potential Risks

Consider the specific perils most likely to affect your business based on:

- Geographic location (hurricane, flood, earthquake zones)

- Industry (restaurants face fire risk; retail faces theft risk)

- Building characteristics (age, construction materials, fire protection systems)

Step 3: Decide How Much Coverage You Need

Set coverage limits that accurately reflect the full replacement cost of your property. Underinsuring to save on premiums is one of the most common and costly mistakes business owners make. If a total loss occurs and your policy limit is $300,000 but replacement costs are $500,000, you are personally responsible for the $200,000 gap.

Insure Your Building for Its Rebuild Cost

One of the most critical details to get right is insuring your building for its rebuild cost, not its market value or sale price. The market value of your property includes the land, location, and other economic factors that have nothing to do with the price of lumber and labor. If a fire destroys your building, the land will still be there. Your insurance needs to cover the actual cost to hire contractors and buy materials to reconstruct the building from the ground up. An accurate replacement cost calculation ensures that if the worst happens, you have the funds to fully restore your operations without facing a massive financial shortfall.

Value Your Inventory at Cost Price

When it comes to your inventory, the rule is simple: insure it for what it cost you to acquire, not what you sell it for. Your commercial property policy is designed to make you whole by replacing your lost assets, not to cover your potential profit margin. Insuring stock at its retail price means you’ll pay higher premiums for coverage you can’t actually use. The best practice is to maintain clear records of your inventory costs. This not only helps you set the right coverage limit but also streamlines the claims process, allowing you to get back to business faster after a loss.

Account for Seasonal Inventory Fluctuations

If your business experiences seasonal peaks, your standard inventory coverage might not be enough. A retailer, for example, may have double or triple the amount of stock on hand in the months leading up to the holidays. If a fire or theft occurs during this peak time, a policy based on your average inventory level could leave you severely underinsured. You can solve this by working with your insurance advisor to add a peak season endorsement to your policy. This provides increased coverage limits for specific months, ensuring your assets are protected when your business is at its busiest and most vulnerable.

Step 4: Choose a Deductible That Fits Your Budget

A higher deductible lowers your premium but increases your out-of-pocket cost when you file a claim. Choose a deductible your business can comfortably afford to pay in the event of a loss.

Step 5: Consider Optional Policy Add-Ons

Standard policies may not cover everything your business needs. Common endorsements include:

- Flood insurance endorsement or standalone policy

- Ordinance or law coverage to cover the cost of rebuilding to current building codes

- Spoilage coverage for perishable inventory (restaurants, food distributors)

- Valuable papers and records coverage

- Outdoor signage and fencing coverage

- Utility services interruption coverage

Step 6: Partner With an Insurance Professional

A knowledgeable insurance broker can compare policies across multiple carriers, identify coverage gaps, and negotiate better rates. At Insurance Underwriters, our team specializes in building commercial property insurance programs tailored to each client’s unique risk profile. We work with leading carriers to find the right balance of coverage, cost, and service.

How to Lower Your Premium

While securing comprehensive coverage is the top priority, managing the cost of your commercial property insurance is a close second. Smart business owners know that premiums aren’t set in stone. By taking a proactive approach to risk management and policy structure, you can find meaningful savings without cutting corners on protection. It’s about making strategic decisions that insurers recognize and reward. Here are a few effective ways to lower your premium.

Bundle Your Policies

One of the most straightforward ways to save is by bundling your coverage. Insurers often offer a package called a Business Owner’s Policy (BOP), which combines commercial property insurance with general liability insurance. According to the U.S. Small Business Administration, purchasing these essential coverages together in a BOP is typically more affordable than buying them as separate, standalone policies. This approach not only simplifies your insurance management but also creates cost efficiencies, making it a smart move for many small and mid-sized businesses.

Install Safety and Security Systems

Insurance is all about risk, and carriers are willing to offer better rates to businesses that actively work to minimize it. Installing and maintaining safety and security systems is a direct investment in lowering your risk profile. This includes monitored fire and burglar alarms, automatic sprinkler systems, and security cameras. These measures reduce the likelihood of a major loss from fire or theft, which are two of the most common commercial property claims. By demonstrating that you are a lower-risk client, you can often secure a notable discount on your premium.

Pay Your Premium Annually

If your business’s cash flow allows, opting to pay your entire insurance premium once a year instead of in monthly installments can lead to savings. Many insurance companies add administrative fees to monthly payment plans to cover the extra processing costs. Paying annually eliminates these fees, resulting in a lower overall cost for the exact same coverage. It’s a simple adjustment that can make a difference to your bottom line over the course of the year.

Commercial Property Insurance for Florida Businesses

Florida businesses face unique risks that make commercial property insurance especially important:

- Hurricane exposure — Florida is the most hurricane-prone state in the U.S. Wind damage claims are among the most common and most expensive commercial property claims filed in the state.

- Flood risk — Coastal cities like Miami, Fort Lauderdale, and Tampa have significant flood exposure. Standard commercial property policies do not cover flood damage; a separate flood policy is required.

- High replacement costs — Building materials and labor costs in South Florida have risen sharply, which means underinsurance is an increasingly common problem.

- Citizens Property Insurance — Many Florida businesses end up insured through Citizens, the state-backed insurer of last resort, when private market options are limited.

If you operate a business in Florida, it is critical to work with a broker who understands the state’s insurance market, carrier appetite, and regulatory environment. Insurance Underwriters is based in Miami and has deep expertise in commercial insurance programs for Florida businesses across construction, healthcare, hospitality, real estate, and professional services.

How to File a Commercial Property Insurance Claim

When property damage occurs, acting quickly and methodically improves your chances of a fair and timely settlement:

- Ensure safety first — evacuate if necessary and call emergency services

- Document everything — photograph and video all damage before making temporary repairs

- Notify your insurance carrier immediately — most policies require prompt notification

- Mitigate further damage — take reasonable steps to prevent additional loss (board up windows, tarp a damaged roof), as failure to mitigate can reduce your claim payout

- Keep all receipts — for temporary repairs, alternative workspace costs, and any other expenses

- Work with your broker — your broker can advocate on your behalf and help navigate the claims process

- Consider a public adjuster — for complex or high-value claims, a public adjuster can help ensure you receive the full payout you are entitled to

Timely documentation and professional guidance are the two biggest factors in successful commercial property insurance claims. When property damage forces a shutdown, business interruption insurance can replace the income your business loses during restoration.

Frequently Asked Questions About Commercial Property Insurance

Commercial Property vs. general liability insurance?

Commercial property insurance covers damage to your own business assets (building, equipment, inventory), while general liability insurance covers claims from third parties for bodily injury, property damage, or personal injury that your business allegedly caused. Most businesses need both, and they are often bundled in a Business Owners Policy (BOP).

How much commercial property insurance do I need?

Your coverage limit should reflect the full replacement cost of your building (if owned), business personal property, and any improvements to leased spaces. An experienced broker can help you conduct a property valuation to set appropriate limits.

Does commercial property insurance cover natural disasters?

Standard policies cover windstorm, hail, lightning, and fire. However, flood and earthquake damage are excluded and require separate policies. In Florida, hurricane wind coverage is included, but there is often a separate, higher hurricane deductible (typically 2-5% of the building value).

Can I get commercial property insurance if I rent my space?

Yes. Even if you do not own the building, you need commercial property insurance to cover your business personal property, tenant improvements, and potential business income losses. Your landlord’s policy does not cover your assets.

What is a coinsurance clause?

A coinsurance clause requires you to insure your property to a certain percentage (usually 80-90%) of its replacement cost. If you underinsure and file a claim, the insurer can reduce your payout proportionally. For example, if you insure a $1,000,000 building for only $600,000 under an 80% coinsurance clause, you are only insured to 75% of the required amount ($600,000 / $800,000), and your claim payout will be reduced by 25%.

How is commercial property insurance different from a Business Owners Policy?

A BOP bundles commercial property insurance with general liability insurance at a discounted rate. It is designed for small to mid-size businesses with standard risk profiles. Standalone commercial property insurance offers more flexibility in coverage limits, endorsements, and policy terms, making it better suited for businesses with higher property values or specialized needs.

Get the Right Coverage for Your Business Property

Commercial property insurance is not optional for any business that relies on physical assets to operate. The right policy protects your building, equipment, inventory, and income against events that could otherwise shut your doors permanently. Whether you are comparing policies for the first time or reviewing an existing program, working with a specialized broker ensures you get the coverage you need at a competitive price.

Insurance Underwriters provides expert commercial property insurance guidance for businesses across Florida and nationwide. Our advisors understand the nuances of commercial property risk and work with top-rated carriers to build tailored coverage programs.

Get your free commercial property insurance quote today or call 305-900-2823 to speak with an advisor.

Key Takeaways

- Cover your assets, not just your building: A comprehensive policy protects the contents essential to your operations, including equipment, inventory, and furniture. Adding business interruption coverage is also key, as it replaces lost income to help you cover payroll and rent during a shutdown.

- Choose replacement cost value for a full recovery: Always select Replacement Cost Value (RCV) coverage to ensure you can buy new replacements for damaged property without a deduction for depreciation. Insure your building for its rebuild cost, not its market sale price, to avoid a massive out-of-pocket expense.

- Identify and address common coverage gaps: Standard property insurance does not cover everything; common exclusions include flood damage, employee injuries, and business vehicles. You will need separate policies, like flood insurance and workers’ compensation, to protect your business from these specific risks.

Comments

Comments are closed.