How Much Does Business Insurance Cost? A Full Guide

Insurance premiums can feel like a huge drain on your budget, especially for a small or mid-sized business. It’s often one of your biggest recurring expenses, right up there with payroll and rent. But that final number isn’t random. Whether you’re launching a startup or looking to trim overhead, getting a handle on your business insurance cost is key. This guide breaks down exactly what drives your rates and gives you actionable ways to present your company as a lower risk—helping you protect your bottom line while keeping the great coverage you need. For more details, see our guide on insurance for startups.

Looking for competitive business insurance rates? Get a free quote from Insurance Underwriters.

This comprehensive guide breaks down business insurance costs by coverage type, explains the factors that affect your premiums, and offers practical strategies for reducing your expenses without sacrificing protection. By the end, you will have a clear picture of what to expect when budgeting for business insurance and how to get the best value from your coverage.

How Much Does Business Insurance Cost?

The average small business in the United States pays between $1,000 and $3,000 per year for a basic insurance package. Business insurance costs vary significantly depending on the type of coverage, your industry, location, revenue, and claims history. Businesses in high-risk industries or those requiring multiple policy types can pay substantially more, sometimes exceeding $10,000 annually for a complete coverage program.

Here is a general overview of average annual premiums for the most common types of business insurance:

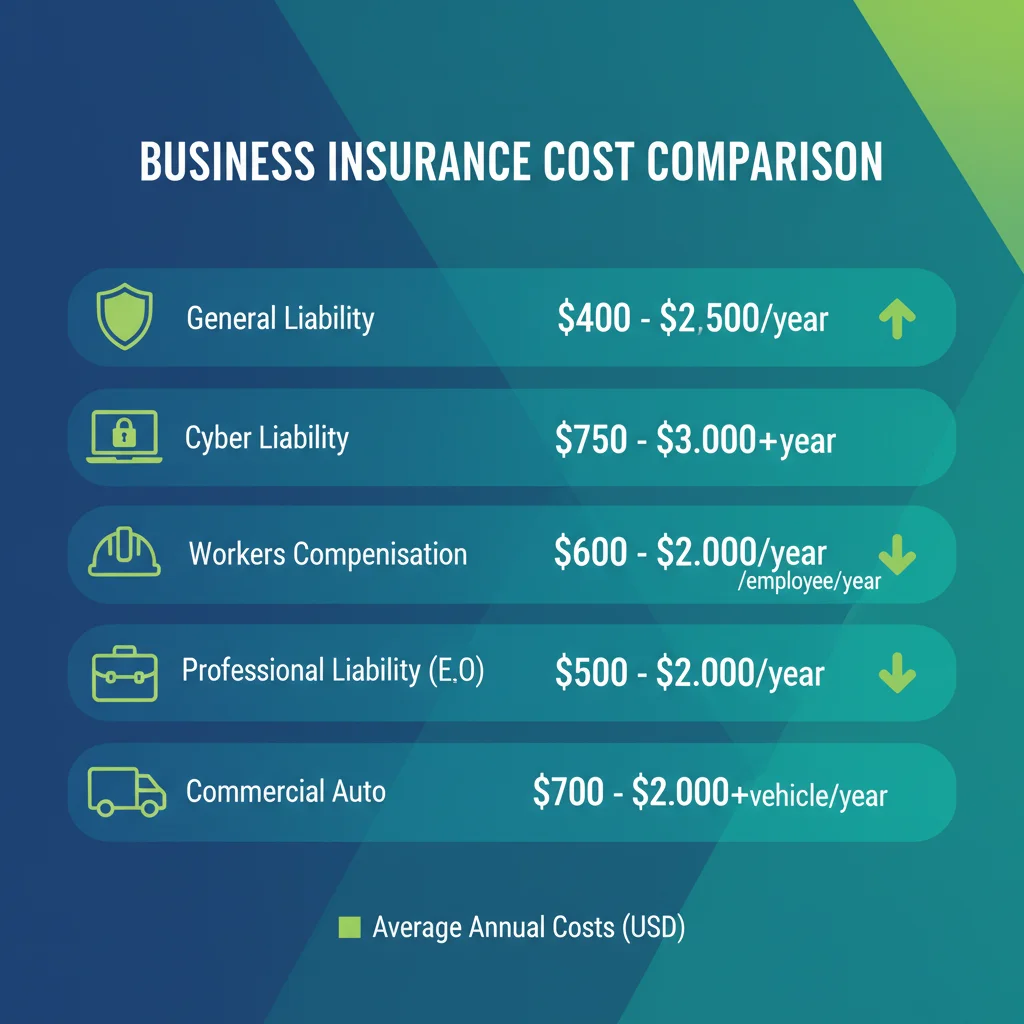

- General Liability Insurance: $400 to $1,500 per year

- Professional Liability (E&O): $500 to $2,500 per year

- Business Owner’s Policy (BOP): $500 to $3,500 per year

- Workers’ Compensation: $500 to $5,000+ per year (varies heavily by state and payroll)

- Commercial Auto Insurance: $1,200 to $2,400 per year per vehicle

- Cyber Liability Insurance: $500 to $5,000 per year

- Commercial Property Insurance: $500 to $3,000 per year

- Business Interruption Insurance: $750 to $2,500 per year

These figures represent averages for small businesses with annual revenue under $1 million. Larger companies, those in higher-risk industries, or businesses with significant assets will typically pay more. Keep in mind that many businesses need multiple types of coverage, so your total annual insurance spend could be the sum of several of these categories.

It is also important to note that premiums can change from year to year. Market conditions, regulatory changes, natural disaster trends, and your own claims experience all influence renewal pricing. Building insurance costs into your annual budget as a variable expense rather than a fixed cost helps avoid surprises.

Understanding Median vs. Average Costs

It’s easy to get fixated on average cost figures, but they don’t always tell the full story. Averages can be misleading because a few high-risk businesses with very high premiums can pull the number up, making it seem higher than what a typical company pays. Instead of focusing on a single number, it’s more effective to think of your total premium as a unique combination of different types of coverage tailored to your specific operations. Remember, these costs aren’t static. Premiums can change at renewal due to market shifts, new regulations, or your claims history. Treating insurance as a variable expense in your budget helps you stay prepared and avoid financial surprises.

What Determines Your Business Insurance Cost?

Business insurance premiums are determined by the level of risk your company presents to the insurer. Understanding the key pricing factors gives you the ability to take proactive steps that lower your costs over time. Insurers use sophisticated models to evaluate risk, but the core variables are consistent across carriers.

Your Industry and Type of Business

Your industry is one of the biggest factors influencing your premiums. A construction company faces significantly higher liability and workers’ compensation costs than an accounting firm. Insurers classify businesses by industry codes (NAICS or SIC codes) and assign risk ratings accordingly. Restaurants, contractors, healthcare providers, and manufacturers generally pay more than professional service firms or technology companies.

Matching Coverage to Specific Industry Risks

Beyond the broad industry category, insurers look at the specific day-to-day operations of your business. For example, a restaurant faces risks like customer slip-and-falls and food poisoning, requiring robust general liability coverage. A marketing consultant, on the other hand, is more concerned with professional errors that could cause a client financial loss, making professional liability insurance a top priority. Businesses with higher inherent risks, like construction or healthcare, naturally require more complex and comprehensive coverage, which directly impacts the final premium. This is why a one-size-fits-all policy rarely works; your coverage must be tailored to your unique operational risks to be effective.

Your Business Size and Revenue

Larger businesses with higher revenue, more employees, and greater assets generally pay more for coverage. Revenue is a common rating factor for general liability policies, while payroll drives workers’ compensation costs. The number of locations, vehicles, and pieces of equipment you operate also factor into your premium calculations. As your business grows, expect your insurance costs to grow proportionally.

Where Your Business is Located

Where your business operates affects costs in multiple ways. State regulations, local weather risks, crime rates, litigation trends, and the legal environment all influence premiums. Businesses in Florida, for example, may pay more for property coverage due to hurricane risk. Companies in states with higher minimum wage or generous workers’ compensation benefits may see elevated workers’ comp premiums. Even the zip code of your office or jobsite can impact your rates.

State Laws on Required Coverage

Your state’s laws create the baseline for your mandatory insurance coverage. The most common example is workers’ compensation insurance, which is a legal requirement in almost every state if you have employees. Some states also mandate commercial auto insurance for any vehicles used for business purposes. However, legal mandates are just one piece of the puzzle. While a state may not legally require you to carry general liability insurance, a landlord or a major client will almost certainly demand proof of coverage before they sign a lease or a contract with you. These legal and contractual obligations establish the minimum policies you must have, forming the foundation of your total insurance costs.

Your Claims History

A history of filed claims will increase your premiums. Insurers view past claims as indicators of future risk. Your loss history typically follows you for three to five years, so a single large claim can impact your rates for multiple renewal cycles. Maintaining a clean claims record is one of the most effective ways to keep costs down over the long term.

Your Coverage Limits and Deductibles

Higher coverage limits mean higher premiums. Conversely, choosing a higher deductible (the amount you pay out of pocket before insurance kicks in) can lower your premium. The key is finding the right balance between affordability and adequate protection. Many contracts and lease agreements specify minimum coverage limits, so make sure your limits meet those requirements before opting for a lower tier to save money.

What is an Aggregate Limit?

Think of your policy’s aggregate limit as the total amount of money in the insurance “bucket” for the year. It’s the absolute maximum your insurer will pay for all combined claims during your policy period. This is different from your per-occurrence limit, which caps the payout for a single incident. For example, your policy might have a $1 million per-occurrence limit and a $2 million aggregate limit. If you have three separate claims in one year, each costing $700,000, your insurer would cover the first two in full ($1.4 million). For the third claim, however, they would only pay the remaining $600,000 in your aggregate “bucket,” leaving you responsible for the other $100,000. Once that aggregate limit is reached, your coverage for that policy term is exhausted. Understanding this number is critical for ensuring your business insurance coverage truly aligns with your potential risk exposure and prevents unexpected financial gaps.

Your Time in Business

New businesses typically pay higher premiums because they lack a track record. As your business matures and demonstrates stability, lower claims frequency, and consistent revenue, insurers may offer better rates. Businesses with more than five years of operating history often qualify for preferred pricing tiers.

Your Credit History

In many states, insurers use business credit scores as a rating factor. Companies with strong credit profiles may receive more favorable rates. Maintaining good business credit, paying bills on time, and keeping debt manageable can positively influence your insurance costs alongside other business benefits.

The Value of Your Business Equipment

The value of your physical assets, from computers and office furniture to specialized machinery and tools, directly impacts your commercial property insurance costs. Insurers need to know the replacement cost of your equipment to calculate the potential payout in case of a fire, theft, or other covered event. Naturally, if you use expensive tools or equipment, your insurance rate might be higher because the financial risk for the insurer is greater. This is especially true for industries like manufacturing, construction, and healthcare, where specialized equipment can be worth hundreds of thousands of dollars. Properly documenting and valuing your assets ensures you have enough coverage without overpaying for protection you don’t need.

Why an LLC Still Needs Insurance

Many business owners believe that forming a Limited Liability Company (LLC) is all the protection they need. While an LLC is a fantastic tool for shielding your personal assets from business debts, it doesn’t make your business immune to risk. Forming an LLC protects your personal money from some business debts, but it doesn’t protect you from lawsuits, workplace injuries, or property damage. You still need insurance. If a client sues your business for negligence, an employee is injured on the job, or a fire destroys your inventory, your business assets are still on the line. Insurance is what protects the company itself, ensuring a single incident doesn’t threaten its financial stability.

What Does General Liability Insurance Cost?

General liability insurance is the foundation of most business insurance programs, covering third-party claims for bodily injury, property damage, and advertising injury. For most small businesses, general liability policies cost between $400 and $1,500 per year, though businesses in high-risk industries may pay $2,000 or more.

Several factors influence general liability costs, including your industry classification, annual revenue, number of employees, and claims history. Contractors and retail businesses tend to pay more than office-based professionals because they face greater exposure to third-party injuries. The standard policy provides $1 million per occurrence and $2 million aggregate limits, which is sufficient for many small businesses.

General liability is often the first policy a business purchases and is frequently required by landlords, clients, and contract agreements. It does not cover professional errors (that requires professional liability) or employee injuries (that requires workers’ compensation). You can learn more in our detailed guide to general liability insurance and our breakdown of business general liability insurance costs.

What Does Professional Liability Insurance Cost?

Professional liability insurance, also known as errors and omissions (E&O) insurance, protects businesses that provide professional services or advice against claims arising from mistakes, negligence, or failure to deliver promised services. Annual premiums typically range from $500 to $2,500 for small service-based businesses, with higher costs for professions that carry greater risk, such as medical practitioners or financial advisors.

The cost depends on your profession, revenue, number of employees, contract requirements, and the specific risks associated with your work. Consultants, accountants, architects, IT professionals, real estate agents, and healthcare providers are among the most common purchasers. Unlike general liability, professional liability policies are usually written on a claims-made basis, meaning the policy in effect when the claim is reported (not when the incident occurred) responds to the loss.

If your business provides any form of advice, consulting, design, or professional service, this coverage is essential. Many clients will require proof of E&O coverage before signing a contract. For a deeper look at coverage options, see our guide to professional liability insurance.

What Does a Business Owner’s Policy (BOP) Cost?

A business owner’s policy (BOP) bundles general liability and commercial property insurance into a single package, often at a lower cost than purchasing each policy separately. Most small businesses pay between $500 and $3,500 per year for a BOP, making it one of the most popular and cost-effective insurance products available.

BOPs are designed for small to mid-sized businesses and typically include coverage for property damage, liability claims, and business interruption. They represent one of the most cost-effective ways to obtain comprehensive coverage with a single premium payment. Many insurers also allow you to add endorsements such as cyber liability, professional liability, hired and non-owned auto, or equipment breakdown to your BOP for additional protection at a fraction of the cost of standalone policies.

The BOP is ideal for businesses that operate from a physical location, own business property or equipment, and face standard liability exposures. Retail shops, offices, restaurants, and service businesses frequently find that a BOP provides the best value for their insurance dollar.

Want to find out how much your business could save with a bundled policy? Get a personalized quote from Insurance Underwriters today.

What Does Workers’ Comp Insurance Cost?

Workers’ compensation insurance covers medical expenses and lost wages for employees injured on the job, and it is legally required in nearly every state for businesses with employees. Costs vary widely, typically ranging from $500 to more than $5,000 per year for small businesses, with the final premium driven by your payroll size and the type of work your employees perform.

Workers’ comp premiums are calculated using a formula that multiplies your total payroll by a rate tied to each employee’s classification code (which reflects the risk level of their work), then adjusts by your experience modification rate (EMR). The EMR compares your claims history to other businesses of similar size in your industry. A lower EMR means lower premiums. Businesses in high-risk industries like construction, manufacturing, or transportation pay significantly more than those in low-risk office environments.

Investing in workplace safety programs, return-to-work programs, and employee training can lower your EMR over time and reduce your workers’ compensation costs substantially. Florida businesses should review our guide to workers’ compensation insurance in Florida for state-specific requirements and cost factors.

How Workers’ Compensation Costs Are Calculated

The formula for calculating workers’ compensation premiums is fairly straightforward. It starts with your total payroll, which is multiplied by a rate based on each employee’s job function. These roles are sorted by “classification codes” that reflect their risk level—an office administrator’s code has a much lower rate than a roofer’s. This base premium is then adjusted by your Experience Modification Rate (EMR), which is essentially your company’s safety report card. The EMR compares your claims history to the industry average, so a score below 1.00 earns you a discount, while a score above 1.00 adds a surcharge. This means you can directly influence your costs by implementing effective workplace safety programs and return-to-work initiatives, turning a mandatory expense into a reflection of your company’s commitment to safety.

What Does Commercial Auto Insurance Cost?

Commercial auto insurance covers vehicles owned or used by your business, providing liability protection, collision coverage, and comprehensive coverage for company cars, trucks, vans, and fleets. Annual premiums generally range from $1,200 to $2,400 per vehicle, though businesses operating heavy trucks, delivery fleets, or vehicles in high-traffic urban areas can pay considerably more.

The cost depends on the type of vehicles, how they are used (commuting vs. long-haul transport), driver records, annual mileage, cargo type, and your coverage limits. Businesses that employ drivers with moving violations or accidents on their records will pay higher rates. Fleet discounts may be available for companies insuring multiple vehicles with the same carrier. If your employees drive their personal vehicles for business purposes, you may need hired and non-owned auto coverage as well.

For details on coverage options and how to structure your policy, visit our guide to commercial auto insurance.

Personal vs. Commercial Auto Policies

It’s a common question we hear: if I use my personal car for work, is my regular auto insurance enough? The short answer is almost always no. Personal auto policies are designed for commuting and personal errands, and they typically have specific exclusions for business-related activities. Using a personal vehicle for business tasks—like visiting clients, making deliveries, or transporting equipment—without the right coverage can lead to a denied claim after an accident. This leaves your business financially exposed to liability costs and potential legal issues, creating a significant and unnecessary risk.

If your business owns a vehicle, the need is even clearer, as it absolutely must be covered by a dedicated commercial auto policy. Personal policies almost never extend to company-owned assets. The distinction between personal and commercial coverage isn’t just about following rules; it’s about closing a critical gap in your company’s risk management strategy. Having the correct policy in place is a fundamental step in protecting your business from liability claims that could otherwise be financially devastating.

What Does Cyber Liability Insurance Cost?

Cyber liability insurance protects businesses against financial losses from data breaches, cyberattacks, ransomware, and other digital threats. Premiums typically range from $500 to $5,000 per year for small businesses, though companies handling large volumes of sensitive data, payment card information, or protected health records may pay significantly more.

Factors that influence cyber insurance costs include the volume and type of data you store, your cybersecurity practices and controls, industry, revenue, and whether you have experienced previous incidents. Insurers increasingly require businesses to demonstrate basic cybersecurity hygiene (multi-factor authentication, endpoint protection, employee training, backup protocols) before issuing coverage. Businesses that cannot meet these requirements may face higher premiums or difficulty obtaining coverage altogether.

As cyber threats continue to grow in frequency and sophistication, this coverage has become essential for businesses of all sizes, not just large corporations. A single data breach can cost tens of thousands of dollars in notification, legal, and recovery expenses. Learn more in our guide to cyber liability insurance.

What Does Commercial Property Insurance Cost?

Commercial property insurance protects the physical assets of your business, including your building, equipment, inventory, and furniture, from events like fire, theft, and natural disasters. For small businesses, the average cost of commercial property insurance is around $108 per month, which comes out to about $1,296 annually. This figure is just a starting point, as your actual premium will depend heavily on the specific assets you need to protect and the risks associated with your location and industry.

Several key factors determine your final cost. The value of your property is the most significant driver; a large warehouse full of expensive equipment will cost more to insure than a small office with standard furniture. Your location also plays a huge role. Businesses in areas prone to hurricanes, floods, or wildfires will face higher premiums. Insurers also look at the construction of your building (a fire-resistant brick building is cheaper to insure than a wood-frame one) and the security measures you have in place, such as fire alarms and sprinkler systems. For a complete overview, explore our guide to commercial property insurance.

What Does Commercial Umbrella Insurance Cost?

Commercial umbrella insurance provides an extra layer of liability protection that goes beyond the limits of your existing policies, such as general liability and commercial auto. Think of it as a safety net for catastrophic claims that could otherwise exhaust your primary coverage and threaten your business’s financial stability. The cost for this added peace of mind typically ranges from $400 to $1,500 annually, depending on your coverage limits and the specific risks tied to your business operations.

The premium for an umbrella policy is influenced by the amount of underlying coverage you carry, your industry, and your claims history. For example, a construction company with a fleet of vehicles will likely pay more than a small consulting firm because its potential for a large liability claim is much higher. While it might seem like an optional expense, a commercial umbrella policy is a strategic investment in resilience. A single severe accident or lawsuit can easily result in damages exceeding a standard $1 million liability limit, and an umbrella policy is what stands between your business assets and a devastating financial loss.

What Do Employee Health Benefits Cost?

Beyond protecting your physical and financial assets, investing in your team is critical, and employee health benefits are often one of the most significant operational expenses a business will face. According to the Kaiser Family Foundation, the average annual premium for employer-sponsored health insurance is approximately $7,739 for single coverage and a staggering $22,221 for family coverage. Employers typically cover a large portion of these costs, making benefits a substantial part of your overall employee compensation package.

The cost of your group health plan depends on several variables. The demographics of your workforce, including age and location, play a major role, as do the types of plans you offer (like HMOs or PPOs) and the level of coverage you provide. A plan with a lower deductible and smaller co-pays will cost more than a high-deductible health plan. As a business owner, structuring a benefits package that is both attractive to employees and financially sustainable requires careful planning and a deep understanding of the employee benefits market.

The Role of Benefits in a Modern Workforce

While the cost is significant, it’s important to view employee benefits as a strategic investment rather than just an expense. Offering a competitive benefits package is crucial for attracting and retaining top talent in today’s job market. Companies that invest in comprehensive benefits often see a direct return through improved employee satisfaction, higher productivity, and lower turnover rates. A strong benefits program sends a clear message that you value your team’s well-being, which fosters loyalty and a more engaged workforce. This is a key part of building a resilient and successful company culture.

Using Technology to Manage Employee Benefits

As leaders in the employee benefits space, we at InsuranceUnderwriters.com have seen firsthand how a strategic approach can transform a company. Our proprietary AI-powered platform helps businesses streamline administration and reduce the time HR teams spend on repetitive questions, which directly impacts operational efficiency.

How to Lower Your Business Insurance Costs

While insurance is a necessary expense, there are proven strategies to manage and reduce your premiums without compromising your coverage. Implementing even a few of these approaches can result in meaningful savings over time.

Bundle Your Policies

Purchasing a business owner’s policy (BOP) or bundling multiple policies with a single carrier often results in discounts of 10% to 25%. Insurers reward loyalty and consolidated accounts with lower premiums. Ask your broker about multi-policy discounts and packaging options.

Increase Your Deductible

Opting for higher deductibles reduces your annual premium. This strategy works best for businesses with strong cash reserves that can absorb a larger out-of-pocket expense in the event of a claim. Increasing your deductible from $500 to $2,500, for example, can significantly lower your annual costs.

Create a Risk Management Plan

Investing in workplace safety, employee training, cybersecurity protocols, and loss prevention can significantly reduce your claims frequency. Insurers often provide discounts for businesses that demonstrate proactive risk management. Formalized safety programs, documented training records, and regular workplace audits all signal to underwriters that your business is a lower risk.

Maintain a Clean Claims History

Every claim you file can increase your premiums at renewal. Address small losses internally when practical, and focus on preventing claims through safety programs and thorough documentation. A three-to-five-year stretch without claims can qualify you for preferred pricing from most carriers.

Compare Quotes from Different Insurers

Insurance rates vary significantly between carriers, sometimes by 30% or more for the same coverage. Working with an independent broker like Insurance Underwriters gives you access to multiple carriers and ensures you get the most competitive rates available for your risk profile. An independent broker works for you, not for any single insurance company, and can negotiate on your behalf.

Prepare Your Information Before Getting Quotes

To get the most accurate and competitive quotes, you need to do a little homework first. Having key details about your business on hand makes the process smoother and ensures the pricing you receive is reliable. Before you start reaching out, gather your business’s industry classification (NAICS code), annual revenue, total employee payroll, and a record of any insurance claims from the past three to five years. Insurers use this information to accurately assess your risk profile and calculate your premium. Presenting a complete and organized picture of your operations not only speeds up the quoting process but also positions you as a well-managed risk, which can lead to more favorable terms from underwriters.

Review Your Policy Annually

Your business changes over time, and your insurance should reflect those changes. Review your policies each year to eliminate coverage you no longer need, adjust limits to match your current risk exposure, and update your payroll and revenue figures. Over-insuring is just as wasteful as under-insuring. A thorough annual review with your broker ensures you are paying for exactly the coverage you need.

Shop Around Every 2-3 Years

While an annual review is essential for fine-tuning your coverage, a full market comparison every two to three years is a critical financial strategy. The insurance market is dynamic; carrier appetites shift, new products become available, and pricing models are constantly updated. The insurer that offered the most competitive rate three years ago may no longer be your best option. Rates can vary by 30% or more between carriers for the exact same coverage, meaning loyalty doesn’t always translate to savings. This is where you can work with an independent broker to your advantage. Instead of spending hours gathering quotes yourself, a broker shops the market for you, leveraging their relationships with multiple carriers to find the optimal balance of cost and protection for your specific risk profile.

Classify Your Employees Correctly

Workers’ compensation premiums are heavily influenced by employee classification codes. Make sure your employees are classified correctly for the work they actually perform. Misclassification can lead to overpayment, and an audit correction can result in significant refunds or additional charges.

Pay Your Premiums Annually

While paying your insurance premiums in monthly installments can be convenient for cash flow, it often comes with extra administrative fees. Many insurance carriers offer a discount if you pay for the entire year’s premium upfront. This simple switch can reduce your total cost and simplifies your accounting with a single annual payment instead of twelve smaller ones. If your business has the available cash, ask your insurance broker about a pay-in-full discount. It’s a straightforward way to capture immediate savings on a necessary business expense.

Reduce Employee Turnover

A stable and experienced team is one of your best assets for risk management. High employee turnover often means having a less experienced workforce, which can lead to a higher rate of workplace accidents and workers’ compensation claims. Insurers recognize that a long-tenured, well-trained team is a safer team. By focusing on strategies to improve employee retention, you not only build a stronger company culture but also create a safer work environment that can lead to a lower experience modification rate and reduced insurance premiums over time.

Keep Accurate Payroll and Time Records

Your payroll figures are a primary factor in calculating your workers’ compensation premiums. Maintaining meticulous and accurate payroll records is essential for avoiding costly errors. Simple mistakes in payroll reporting or employee classification can cause you to overpay throughout the year. Even worse, inaccuracies discovered during an end-of-year insurance audit can result in unexpected lump-sum payments and potential penalties. Implementing a reliable system for payroll management ensures you pay the correct premium for your actual risk exposure.

Prioritize Legally Required Coverage First

When building your insurance program, start with the essentials. Before you consider optional coverages, make sure you have all the policies legally required by your state and industry. For most businesses with employees, this means securing workers’ compensation. If you use vehicles for work, commercial auto insurance is also a must. Fulfilling these legal requirements protects you from fines and penalties and establishes a solid foundation for your risk management plan. Once those core policies are in place, you can strategically add other coverages based on your specific risks and budget.

So, Is Business Insurance Worth the Cost?

The short answer is yes. Business insurance is not just a regulatory requirement in many cases; it is a financial safety net that protects your company from potentially devastating losses. A single lawsuit, property loss, or data breach can cost far more than years of insurance premiums combined. The question is not whether you can afford insurance, but whether you can afford to go without it.

Consider that the average general liability claim costs approximately $30,000 to resolve, and the average professional liability claim exceeds $50,000 when legal defense costs are included. A single workers’ compensation claim for a serious injury can easily surpass $100,000. These figures make annual premiums of a few thousand dollars look like a prudent investment.

Beyond financial protection, business insurance provides credibility. Clients, partners, and landlords often require proof of insurance before entering into contracts. Having adequate coverage demonstrates professionalism and financial responsibility. Many government contracts, commercial leases, and vendor agreements specify minimum insurance requirements that you cannot meet without active policies.

For businesses looking to understand their specific liability insurance costs, working with an experienced broker ensures you get coverage tailored to your needs at a competitive price. Business interruption insurance is another critical coverage that many owners overlook until it is too late.

Frequently Asked Questions

How much does business insurance cost per month?

Most small businesses pay between $100 and $300 per month for a comprehensive insurance package that includes general liability, property coverage, and other essential policies. Your actual cost depends on your industry, business size, location, and the specific coverages you need. Businesses in low-risk industries with minimal claims history may pay less, while high-risk operations could pay considerably more.

What is the cheapest type of business insurance?

General liability insurance is typically the most affordable business policy, with many small businesses paying under $50 per month. However, the cheapest option is not always the best. Your coverage needs should be determined by your specific business risks, not solely by cost. Skipping necessary coverage to save money can expose you to losses that far exceed any premium savings.

Do I need business insurance if I work from home?

Yes. Homeowner’s insurance policies typically do not cover business-related claims. If a client visits your home office and is injured, or if business equipment is stolen, your personal policy likely will not respond. A home-based business insurance policy or a BOP can fill these gaps affordably, often for just a few hundred dollars per year.

Can I get business insurance with no employees?

Absolutely. Solo entrepreneurs, freelancers, and independent contractors should carry at minimum general liability insurance and professional liability insurance if they provide services or advice. Many clients and contracts require proof of coverage regardless of your company size. Workers’ compensation is generally not required if you have no employees, though some states require sole proprietors in certain industries to carry it.

How can I get the lowest business insurance rates?

Work with an independent insurance broker who can compare rates across multiple carriers. Bundle your policies, maintain a clean claims record, invest in risk management, and review your coverage annually. Getting quotes from an experienced agency like Insurance Underwriters ensures you see competitive options tailored to your business. Avoid the temptation to simply choose the cheapest quote without understanding what is covered and what is excluded.

Does business insurance cover lawsuits?

Yes. General liability and professional liability policies cover legal defense costs, settlements, and judgments arising from covered claims. This protection is one of the primary reasons businesses purchase insurance, as legal expenses alone can be financially devastating even if a lawsuit is ultimately dismissed. Defense costs can easily reach $50,000 or more, even for a straightforward case.

Ready to find out exactly what business insurance will cost for your company? Contact Insurance Underwriters for a free, no-obligation quote and let our team build a coverage plan that fits your budget and protects your business.

Key Takeaways

- Know the Factors That Shape Your Rate: Your insurance premium isn’t a random number; it’s calculated based on your industry, revenue, location, and claims history. Understanding these key drivers is the first step toward managing your costs effectively.

- Implement Smart Strategies to Save Money: You can actively lower your premiums without sacrificing protection. Simple actions like bundling policies, increasing your deductible, and maintaining a strong safety record can make a significant financial impact.

- View Insurance as a Financial Safety Net: Think of your policy as protection for your company’s future, not just another bill. The cost of a single major claim can far exceed years of premiums, making the right coverage essential for financial resilience.

Comments

Comments are closed.