What Is Professional Liability Insurance, Really?

Mistakes happen. Even with the best intentions, a client might claim your professional services or advice caused them financial harm. A lawsuit over an error, a missed deadline, or unmet expectations can be incredibly stressful and expensive. This is exactly what Professional Liability Insurance is for. Also known as errors and omissions (E&O) insurance, it covers your legal fees, settlements, and judgments. For healthcare providers, medical malpractice insurance provides similar crucial protection. You can also learn more about typical E&O insurance costs.

Get a Professional Liability Insurance Quote or call Insurance Underwriters at (305) 900-2823 for a free consultation.

If your business provides services, consulting, or specialized expertise to clients, professional liability insurance is one of the most important policies you can carry. A single client dispute can generate six-figure legal costs, even when the claim has no merit.

This guide explains what professional liability insurance covers, who needs it, how much it costs, and how to choose the right policy for your business.

Key Takeaways

- Professional liability insurance (also called E&O insurance) covers claims that your professional services caused a client financial harm.

- Coverage pays for legal defense costs, settlements, and judgments, even for frivolous lawsuits.

- Most policies operate on a claims-made basis, meaning coverage depends on when a claim is filed, not when the work was performed.

- Anyone providing professional services, advice, or specialized expertise should carry this coverage.

- The national average cost is approximately $56 per month for a small business with a $1 million per-claim policy.

- Professional liability is different from general liability insurance, which covers bodily injury and property damage instead of financial harm from services.

What Is Professional Liability Insurance, Really?

Professional liability insurance is a type of business insurance designed specifically for companies and individuals that provide professional services or advice. Unlike general liability insurance, which covers bodily injury and property damage claims, professional liability insurance addresses financial losses that clients allege were caused by your professional work.

The core purpose of this coverage is straightforward: when a client claims your services harmed them financially, professional liability insurance pays for your legal defense and any resulting settlements or judgments, up to your policy limits.

How Does This Insurance Actually Work?

Most professional liability policies operate on a claims-made basis, meaning coverage applies based on when a claim is filed, not when the alleged error occurred. This is an important distinction that affects how your coverage works in practice.

Here is how the claims-made structure works:

- Retroactive date: Your policy defines how far back in time your work is covered. Any claims related to work performed before this date are not covered.

- Policy period: Claims must be reported during the active policy period to trigger coverage.

- Tail coverage: If you cancel your policy or switch insurers, you may need extended reporting period (tail) coverage to protect against claims filed after your policy ends but related to work performed while you were insured.

Professional liability policies also include two key financial limits:

- Per-claim limit: The maximum amount the insurer will pay for any single claim.

- Aggregate limit: The total amount the insurer will pay across all claims during the policy period.

Most small businesses start with a $1 million per-claim and $1 million or $2 million aggregate policy, though businesses in high-risk professions may need higher limits.

Is Professional Liability the Same as E&O Insurance?

One of the most common questions about this coverage is whether professional liability insurance and errors and omissions (E&O) insurance are the same thing. The short answer: yes. These terms describe identical coverage.

The terminology difference is largely industry-driven:

- Professional liability insurance is the broader, more formal term used across most industries.

- Errors and omissions (E&O) insurance is the preferred term in technology, real estate, financial services, and insurance industries.

- Professional indemnity insurance is the term commonly used in the United Kingdom and other international markets.

Regardless of what your insurer or industry calls it, the coverage protects against the same core risks: claims that your professional services, advice, or work product caused a client financial harm.

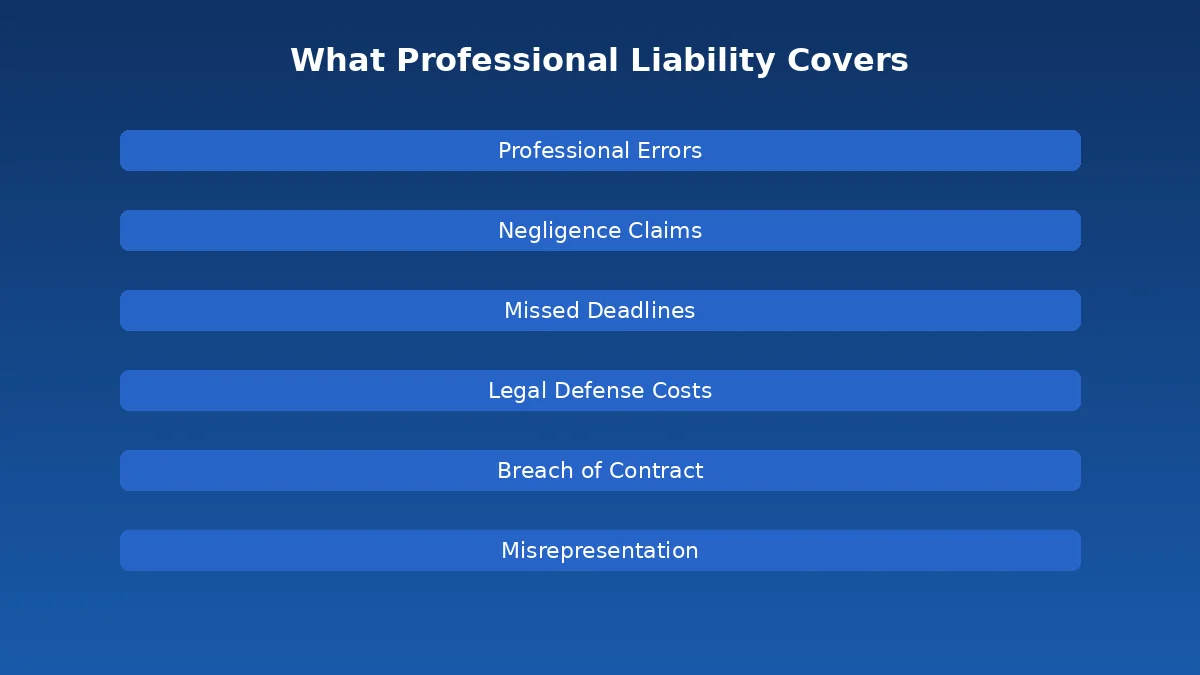

What Does Professional Liability Insurance Actually Cover?

Professional liability insurance covers a specific set of risks tied to the delivery of professional services. Understanding exactly what falls under this coverage helps you evaluate whether your current policy is adequate or whether you need additional protection.

Claims and Scenarios Your Policy Covers

| Claim Type | What It Covers | Example |

|---|---|---|

| Professional errors and mistakes | Mistakes in your work product or deliverables that cause a client financial loss | An accountant files incorrect tax returns, resulting in IRS penalties for the client |

| Negligence | Failure to meet the professional standard of care expected in your industry | A consultant’s flawed market analysis leads a client to make a costly business decision |

| Missed deadlines | Late deliverables or missed filing dates that cause financial harm | A law firm misses a statute of limitations, eliminating a client’s ability to file suit |

| Misrepresentation | Allegations that your statements about services or results were misleading | A marketing agency overstates projected campaign ROI, and the client relies on those projections |

| Breach of contract | Failure to deliver services as outlined in your contract | A software developer fails to deliver a functional product by the agreed deadline |

| Legal defense costs | Attorney fees, court costs, expert witnesses, and related defense expenses | A frivolous lawsuit requires $50,000 in legal defense costs before being dismissed |

Intellectual Property and Reputational Harm

Your professional work creates valuable intellectual property, but it also opens the door to risks that can damage your company’s reputation. Professional liability insurance often extends to cover claims that can cause significant reputational harm, like defamation, disparagement, and copyright infringement. If a competitor accuses you of stealing a design, or a client alleges your marketing materials were misleading, your policy can be a financial backstop. It helps cover the steep costs of legal defense, settlements, and damages that result from these allegations. This protection is crucial, as intellectual property insurance helps shield your business from claims that you infringed on another party’s IP, saving you from paying for a costly legal battle on your own.

Key Coverage Details You Can’t Ignore

Professional liability insurance protects your business regardless of whether the legal claims against you have merit. This is a critical point that many business owners overlook. Even frivolous lawsuits require legal defense, and those costs add up fast. Average defense costs for professional liability claims range from $3,000 to $150,000 per claim, depending on complexity.

Your policy typically covers:

- Attorney fees and legal representation

- Court costs and filing fees

- Expert witness fees

- Investigation expenses

- Settlement payments (up to policy limits)

- Judgments awarded by a court (up to policy limits)

- Administrative hearing costs for licensed professionals

Understanding Shrinking (Eroding) Limits

It’s essential to know that most professional liability policies have limits that “shrink” or “erode.” This means that the money an insurer spends on your legal defense is subtracted from your total coverage available for that claim. For example, if you have a $1 million per-claim limit and your legal fees reach $150,000, you now have only $850,000 remaining to pay for a potential settlement or judgment. This detail is critical because defense costs can quickly diminish your available protection, especially in a complex or prolonged lawsuit.

Your policy will outline two primary financial caps: a per-claim limit, which is the most the insurer will pay for a single incident, and an aggregate limit, the total amount payable for all claims during your policy period. When your defense costs erode your per-claim limit, you could be left with insufficient funds to cover a settlement, forcing you to pay the difference out of pocket. That’s why choosing the right limits isn’t just about the worst-case judgment; it’s about ensuring you have enough coverage for the entire legal process. A strategic risk advisor can help you determine the appropriate limits for your profession.

The Details on Tail Coverage Costs and Benefits

Because professional liability policies are claims-made, a gap in coverage can leave your past work exposed. This is where tail coverage comes in. If you cancel your policy, retire, or sell your business, you may need an extended reporting period, or “tail,” to protect against claims filed after your policy ends but related to work performed while you were insured. Without it, a client could sue you years after a project was completed, and you would have no coverage for the legal battle.

Tail coverage is a one-time purchase, and its cost is typically a multiple of your final annual premium, often ranging from 150% to 300%. While it’s a significant investment, the benefit is invaluable. It provides lasting peace of mind by closing the door on future liability for your past professional services. For any professional planning a career change or retirement, securing tail coverage is a fundamental step in protecting your personal assets from future claims.

Potential Coverage for Lost Wages

While the primary function of professional liability insurance is to cover legal defense and settlement costs, some policies offer an additional, often overlooked, benefit: reimbursement for lost wages. If you are required to attend a trial, hearing, or deposition for a covered claim, you can’t be at work generating income. This policy feature provides a daily stipend (e.g., $500 per day) to help compensate for that lost time. It’s a valuable provision that reduces the personal financial strain of a lawsuit.

It’s important to note that this is not a standard feature on every policy and usually comes with its own sub-limit. The core protection your policy provides is for the major financial burdens of a lawsuit. Your policy is built to cover attorney fees, court costs, expert witness fees, investigation expenses, and, of course, settlements and judgments up to your policy limits. When reviewing your options, ask about coverage for lost wages as an added layer of financial security. You can learn more about what drives E&O insurance costs on our blog.

What Isn’t Covered by Professional Liability Insurance?

Understanding exclusions is just as important as knowing what is covered. Professional liability insurance is not a catch-all policy. It has specific boundaries that leave certain risks unprotected.

What Your Policy Will Likely Exclude

- Bodily injury and property damage: If a client is physically injured at your office or their property is damaged, those claims fall under general liability insurance, not professional liability.

- Employee-related claims: Lawsuits from employees alleging wrongful termination, discrimination, or harassment require Employment Practices Liability Insurance (EPLI). Insurance Underwriters offers EPLI coverage as part of comprehensive commercial insurance packages.

- Intentional or criminal acts: Deliberate fraud, criminal conduct, or intentional wrongdoing is never covered under professional liability.

- Cyber incidents: Data breaches, ransomware attacks, and cyber-related claims require dedicated cyber liability insurance.

- Prior knowledge: Claims you knew about or should have reasonably anticipated before the policy start date.

- Pre-existing claims: Any claim or circumstance reported to a previous insurer.

Fraud, Dishonest Acts, and Assumed Liability

Professional liability insurance is built to cover negligence—the “oops” moments—not intentional harm. Every policy contains exclusions for claims arising from fraudulent, criminal, or dishonest acts. If a claim alleges you intentionally misled a client or committed a crime, your insurer will likely deny coverage. The purpose of this insurance is to protect you from the financial fallout of professional errors and omissions, not to shield you from the consequences of deliberate wrongdoing. Similarly, be cautious about “assumed liability” in contracts. If you agree to take on liability that you wouldn’t otherwise have under the law, your policy may not cover it. It’s always a good idea to have your contracts reviewed to ensure you aren’t taking on uninsurable risks.

Identifying Potential Gaps in Your Coverage

The prior acts exclusion is one of the most significant gaps in professional liability coverage. If your policy has a retroactive date that does not extend back to when you started providing professional services, you could have years of past work without protection. When switching insurers, always negotiate the earliest possible retroactive date.

Beyond professional liability, many business owners also benefit from umbrella insurance, which adds an extra layer of liability protection that extends across multiple policies.

Who Needs Professional Liability Insurance?

Any business or individual that provides professional services, advice, or specialized expertise to clients should carry professional liability coverage. The risk of a client alleging that your work caused them financial harm exists across virtually every service-based profession.

Is Your Profession on This List?

Financial and legal professionals:

- Accountants and CPAs

- Financial advisors and wealth managers

- Attorneys and paralegals

- Tax preparers and enrolled agents

- Mortgage brokers and loan officers

Technology and consulting:

- IT consultants and managed service providers

- Software developers and engineers

- Management consultants and business advisors

- Marketing agencies and public relations firms

- Data analysts and business intelligence professionals

Healthcare providers:

- Physicians and surgeons

- Nurses and nurse practitioners

- Dentists and dental hygienists

- Mental health professionals

- Physical and occupational therapists

Real estate and insurance:

- Real estate agents and brokers

- Property managers

- Insurance agents and brokers

- Appraisers and inspectors

Creative and design professionals:

- Architects and engineers

- Interior designers

- Graphic designers and web developers

- Freelance writers and editors

When Is This Insurance Legally Required?

Professional liability insurance is not universally mandated by federal law, but several situations make it effectively mandatory:

- State licensing requirements: Many states require professionals in regulated fields (attorneys, medical professionals, architects, engineers) to carry minimum professional liability coverage.

- Client contracts: Most corporate and government clients require proof of professional liability insurance before signing a services agreement.

- Industry standards: Professional associations and licensing boards in fields like accounting, law, and healthcare set coverage expectations for their members.

- Lease and vendor agreements: Many commercial leases and vendor contracts include insurance requirements that specify professional liability coverage.

How Much Does Professional Liability Insurance Cost?

Professional liability insurance costs vary widely depending on your industry, business size, location, and risk profile. However, most small businesses can expect to pay between $30 and $70 per month for standard coverage.

What Can You Expect to Pay?

| Risk Level | Professions | Monthly Cost Range | Annual Cost Range |

|---|---|---|---|

| Low risk | Freelance writers, notaries, consultants | $25 – $50 | $300 – $600 |

| Medium risk | IT professionals, contractors, marketers | $51 – $100 | $612 – $1,200 |

| High risk | Attorneys, financial advisors, medical professionals | $100 – $166+ | $1,200 – $2,000+ |

The national average for professional liability insurance sits at approximately $56 per month ($675 per year) for a small business with one to four employees and a $1 million per-claim / $2 million aggregate policy.

A Look at Average and Median Costs

While the national average of around $56 per month is a helpful benchmark, it’s important to know what that figure represents. Averages can be skewed higher by professions with significant risk, like architects or financial advisors managing large portfolios. This means the median cost—the price point where half of businesses pay more and half pay less—is often a more realistic indicator for a typical small business. For many service providers, the cost falls comfortably within the $30 to $70 per month range for a standard $1 million policy. Ultimately, these numbers are just a starting point. The only way to know your exact cost is to get a personalized quote based on your specific operations and risk profile.

What Determines Your Insurance Rate?

Several factors directly influence how much you pay for professional liability coverage:

- Industry and profession: Higher-risk professions (law, medicine, financial services) pay significantly more than lower-risk fields.

- Business size and revenue: More employees and higher revenue typically correlate with higher premiums because there are more opportunities for claims.

- Claims history: A clean claims history keeps premiums low, while prior claims increase costs substantially.

- Coverage limits: Higher per-claim and aggregate limits result in higher premiums.

- Deductible amount: Choosing a higher deductible lowers your premium but increases your out-of-pocket cost per claim.

- Geographic location: Some states and metro areas have higher litigation rates, which drives up premiums.

- Years of experience: Newer businesses may face higher rates until they establish a track record.

Need help determining the right professional liability coverage for your business? Request a free quote or call (305) 900-2823 to speak with an experienced advisor at Insurance Underwriters.

Professional vs. General Liability: What’s the Difference?

Understanding the difference between professional liability and general liability insurance is critical because they protect against completely different risks. Most service-based businesses need both.

| Feature | Professional Liability | General Liability |

|---|---|---|

| What it covers | Financial losses from professional services | Bodily injury and property damage |

| Claim trigger | Client alleges your work or advice caused financial harm | Third party is injured or property is damaged |

| Policy type | Claims-made (when claim is filed) | Occurrence-based (when incident happens) |

| Common claims | Errors, negligence, missed deadlines, misrepresentation | Slip-and-fall injuries, advertising injury, product liability |

| Average cost | $56/month (small business) | $42/month (small business) |

| Who needs it | Any business providing professional services | Most businesses with physical operations |

A general liability policy will not cover claims arising from the professional services you provide. If a client sues you because your consulting advice led to a failed business initiative, that is a professional liability claim. If that same client trips over a cable in your office and breaks their arm, that is a general liability claim.

Other Policies to Round Out Your Coverage

Professional liability insurance works best as part of a comprehensive commercial insurance program. Depending on your business type, you may also need:

- Directors and Officers (D&O) Insurance: Protects company leadership against personal liability for management decisions.

- Cyber Liability Insurance: Covers data breaches, ransomware, and other cyber incidents.

- Workers’ Compensation: Required in most states for businesses with employees.

- Commercial Property Insurance: Covers your business property, equipment, and inventory.

- Business Owner’s Policy (BOP): Bundles general liability and commercial property coverage at a discounted rate.

How to Choose the Right Professional Liability Policy

Selecting the right professional liability insurance policy involves more than comparing premiums. The cheapest policy is not always the best fit for your business. Here is what to evaluate when comparing options.

How to Set Your Coverage Limits and Deductible

Start with adequate coverage limits. The most common configuration for small businesses is $1 million per claim and $1 million or $2 million aggregate. However, businesses in high-risk professions or those with large client contracts may need $2 million to $5 million in coverage.

Your deductible (the amount you pay out of pocket before coverage kicks in) directly affects your premium. A $1,000 deductible is standard, but opting for a $2,500 or $5,000 deductible can meaningfully reduce your annual premium.

Decoding Split Limits (e.g., $1M/$3M)

When you see policy limits written as a pair of numbers, like $1M/$3M, you’re looking at what are called split limits. This structure is common in professional liability insurance and is simpler to understand than it looks. The first number is your per-claim limit—that’s the maximum amount your insurer will pay for any single lawsuit. The second number is your aggregate limit, which is the total amount the insurer will pay for all claims combined during your policy period, usually one year. So, with a $1M/$3M policy, your insurer would cover up to $1 million for one specific client dispute. If you were unlucky enough to face three separate claims that year, your total coverage for all of them together would be capped at $3 million.

Understanding Your Policy’s Retroactive Date

The retroactive date determines how far back your policy covers past work. Always push for the earliest possible retroactive date, ideally going back to when you first started providing professional services.

Claims-Made vs. Occurrence Policies

The distinction between claims-made and occurrence policies is one of the most critical concepts in professional liability insurance. The structure of your policy determines when coverage is triggered, which directly impacts your protection, especially if you switch insurers or retire. Most professional liability policies are written on a claims-made basis, while general liability policies typically use an occurrence structure. Understanding how each works is essential for preventing unexpected gaps in your coverage. It’s not just a technical detail; it’s the foundation of how your policy will respond when you need it most.

How Claims-Made Policies Work

Most professional liability policies operate on a claims-made basis, which means coverage applies based on when a claim is filed against you, not when the professional service was performed. For a claim to be covered, it must be made and reported during your active policy period. This structure relies on a “retroactive date,” which is the date from which your past work is covered. Any work performed before this date is excluded. If you cancel your policy or switch to a new provider, you lose coverage for all past work unless you purchase an extended reporting period, commonly known as “tail coverage,” to protect against future claims.

How Occurrence Policies Work

Occurrence policies provide a more straightforward form of protection. They cover incidents that happen during the policy period, regardless of when the claim is eventually reported. This means if an error occurs while your policy is active, you are covered, even if the client doesn’t file a lawsuit until years later, long after your policy has expired. This structure provides long-term certainty and eliminates the need for tail coverage. While less common for professional liability, occurrence policies are the standard for other types of insurance, such as general liability, because the events they cover (like a slip-and-fall) are typically discovered immediately.

Customizing Your Coverage with Policy Add-Ons

Depending on your industry, consider these common endorsements:

- Cyber liability endorsement: Adds basic cyber coverage to your professional liability policy.

- Regulatory defense coverage: Covers legal costs related to regulatory investigations and licensing board inquiries.

- Subcontractor coverage: Extends protection to work performed by subcontractors under your supervision.

- Worldwide coverage: Expands the policy to cover claims from international clients.

Why Your Insurance Carrier’s Reputation Matters

Choose an insurer with strong financial ratings (A.M. Best rating of A or higher) and a reputation for fair claims handling. A policy is only as good as the insurer standing behind it.

Real-Life Claim Examples by Industry

Understanding how professional liability claims play out in practice helps illustrate why this coverage matters. Here are common scenarios across different industries.

Consulting and Advisory Services

A management consultant recommends a restructuring strategy to a manufacturing client. The strategy leads to operational disruptions and a 15% revenue decline. The client sues, claiming the consultant’s advice was negligent and failed to account for supply chain dependencies. Professional liability insurance covers the legal defense and eventual settlement.

Technology and IT Services

An IT firm deploys a new software system for a retail chain. (For comprehensive protection, technology insurance bundles professional liability with cyber and other critical coverages.) A coding error causes the point-of-sale system to miscalculate sales tax for three months. The retailer faces $200,000 in back taxes and penalties, and sues the IT firm for the errors. The firm’s E&O policy covers the defense costs and the settlement.

Accounting and Financial Services

A CPA firm prepares annual tax filings for a small business. An error in depreciation calculations results in the client significantly underpaying taxes. When the IRS audits the client two years later, the resulting penalties and interest total $85,000. The client files a claim against the CPA firm, and professional liability insurance covers the costs.

Healthcare Professionals

A physical therapist develops a treatment plan that aggravates a patient’s existing condition, resulting in extended recovery time and additional medical expenses. The patient files a malpractice claim alleging negligent treatment. The therapist’s professional liability policy covers the legal defense and settlement.

Managing Your Policy and Proving Coverage

Once you have your professional liability policy in place, the next step is knowing how to manage it effectively. This isn’t just about paying your premiums on time; it’s about understanding the mechanics of your coverage so you can use it when you need it most. Two of the most critical aspects of policy management are knowing exactly when and how to report a potential claim and being able to provide proof of your insurance to clients and partners. Getting these two things right ensures your policy works as a strategic asset, protecting your business and giving your clients the confidence to work with you.

The Importance of Timely Claim Reporting

Most professional liability policies operate on a claims-made basis, which is a crucial detail to understand. This means your coverage is triggered based on when a claim is filed, not when the professional error allegedly happened. For your policy to respond, the claim must be reported during your active policy period. If you wait too long—even if the work in question was done while you were insured—you could lose your coverage for that incident. This makes prompt communication with your insurer absolutely essential. The moment you become aware of a situation that could lead to a claim, you should report it. Don’t wait for a formal lawsuit to be filed.

Requesting a Certificate of Liability Insurance

A Certificate of Liability Insurance (COI) is your official proof of coverage, and clients will frequently ask for one before signing a contract. This document confirms that you have an active policy and shows your coverage limits. It’s important because clients need to know you have the right kind of protection. For instance, a general liability policy covers things like bodily injury, but it won’t help if a client sues you for financial losses caused by your professional advice. The COI proves you have the specific professional liability coverage they require. Getting a COI is typically a straightforward process; your insurance advisor can issue one for you, often within the same day, so you can finalize contracts without delay.

How to Reduce Your Professional Liability Insurance Costs

While you cannot eliminate the risk that comes with providing professional services, there are practical steps you can take to manage your premium costs:

Professionals who serve as benefit plan administrators or trustees should also evaluate fiduciary liability insurance, which specifically covers ERISA claims related to employee benefit plan management, including excessive fee allegations and imprudent investment selections.

- Maintain a clean claims history. The single biggest factor in your premium is your track record. Avoiding claims through careful work and strong client communication keeps costs low.

- Implement quality control processes. Documented procedures for client deliverables, peer review of work products, and formal project management reduce error rates.

- Use clear contracts. Well-drafted engagement letters and contracts that define scope, deliverables, timelines, and limitations reduce the likelihood of disputes.

- Bundle your policies. Purchasing professional liability alongside general liability and other coverages from the same insurer often qualifies for multi-policy discounts.

- Choose appropriate limits. Do not overpay for coverage limits you do not need. Work with an experienced broker to right-size your coverage.

- Review annually. As your business evolves, your risk profile changes. Annual policy reviews ensure your coverage matches your actual exposure.

- Complete risk management training. Some insurers offer premium discounts for businesses that complete approved risk management or continuing education programs.

Frequently Asked Questions About Professional Liability Insurance

What is the difference between professional liability and malpractice insurance?

Malpractice insurance is a specialized form of professional liability insurance designed for healthcare professionals. Both cover claims of professional errors and negligence, but malpractice policies are tailored to the specific risks and regulatory requirements of medical practice. For non-medical professionals, standard professional liability or E&O insurance provides equivalent protection.

Do I need professional liability insurance if I am a sole proprietor?

Yes. As a sole proprietor, your personal assets are at risk in a professional liability lawsuit. Without coverage, a single client claim could jeopardize your personal savings, home, and other assets. Professional liability insurance creates a financial barrier between your business activities and your personal wealth.

Does an umbrella insurance policy cover professional liability?

Typically, no. Standard commercial umbrella policies provide excess coverage over general liability, commercial auto, and employers’ liability. They generally exclude professional liability claims. If you need higher professional liability limits, you will need to increase your underlying professional liability policy limits or purchase a separate professional liability umbrella.

How much professional liability insurance do I need?

The right coverage amount depends on your industry, the size of your client contracts, and your risk exposure. A general guideline is that your per-claim limit should be at least as large as the largest contract you work on, since that represents your maximum potential exposure. Most small businesses start with $1 million per claim and scale up as they take on larger clients.

Can I get professional liability insurance with a claims history?

Yes, though it may cost more. Insurers evaluate the nature, frequency, and severity of past claims. A single minor claim from years ago will have less impact than multiple recent claims. Some insurers specialize in higher-risk placements and may offer competitive rates even with a claims history.

Is professional liability insurance tax deductible?

Yes. Professional liability insurance premiums are a deductible business expense for federal income tax purposes. Consult your tax advisor for specific guidance on how to categorize and report this deduction.

Protecting Your Work with the Right Coverage

Professional liability insurance is not optional for service-based businesses. It is a fundamental part of your risk management strategy. A single client claim, whether legitimate or frivolous, can cost tens or even hundreds of thousands of dollars in legal fees and settlements.

The right professional liability policy protects your business assets, preserves your professional reputation, and gives your clients confidence that you stand behind your work.

Insurance Underwriters provides professional liability insurance solutions tailored to your industry and risk profile. Our team evaluates your specific exposure, identifies coverage gaps, and structures policies that deliver comprehensive protection without unnecessary cost.

Get a Professional Liability Insurance Quote

Contact Insurance Underwriters at (305) 900-2823 to discuss your professional liability insurance needs with an experienced advisor.

Disclaimer: This article provides general information about professional liability insurance and is not intended as legal or insurance advice. Coverage details, exclusions, and availability vary by insurer and state. Consult a licensed insurance professional for guidance specific to your situation.

Related Articles

- Professional Liability Insurance: What It Covers and Why Your Business Needs It

- E&O Insurance Cost: A Complete Breakdown

- E&O Insurance: Complete Guide – Insurance Underwriters

- What General Liability Covers – Insurance Underwriters

- General Liability Insurance: What It Covers, Costs, and Why Your Business Needs It

Comments

Comments are closed.