Umbrella Insurance: What It Is and Why You Need It

Your standard auto and homeowners insurance policies cover a lot, but they have limits. When a lawsuit or serious accident pushes past those limits, the remaining costs come out of your personal savings, investments, retirement accounts, and even future earnings. That is where umbrella insurance steps in.

Get your free umbrella insurance quote or call (305) 900-2823 to speak with an advisor at Insurance Underwriters today.

A personal umbrella policy adds $1 million or more in additional liability protection on top of your existing coverage, and it typically costs less than $1 per day. For anyone with assets worth protecting, or anyone who could face a lawsuit exceeding standard policy limits, umbrella insurance is one of the most cost-effective forms of financial protection available.

This guide explains what umbrella insurance is, how it works, what it covers (and what it does not), how much it costs, and how to determine whether you need it.

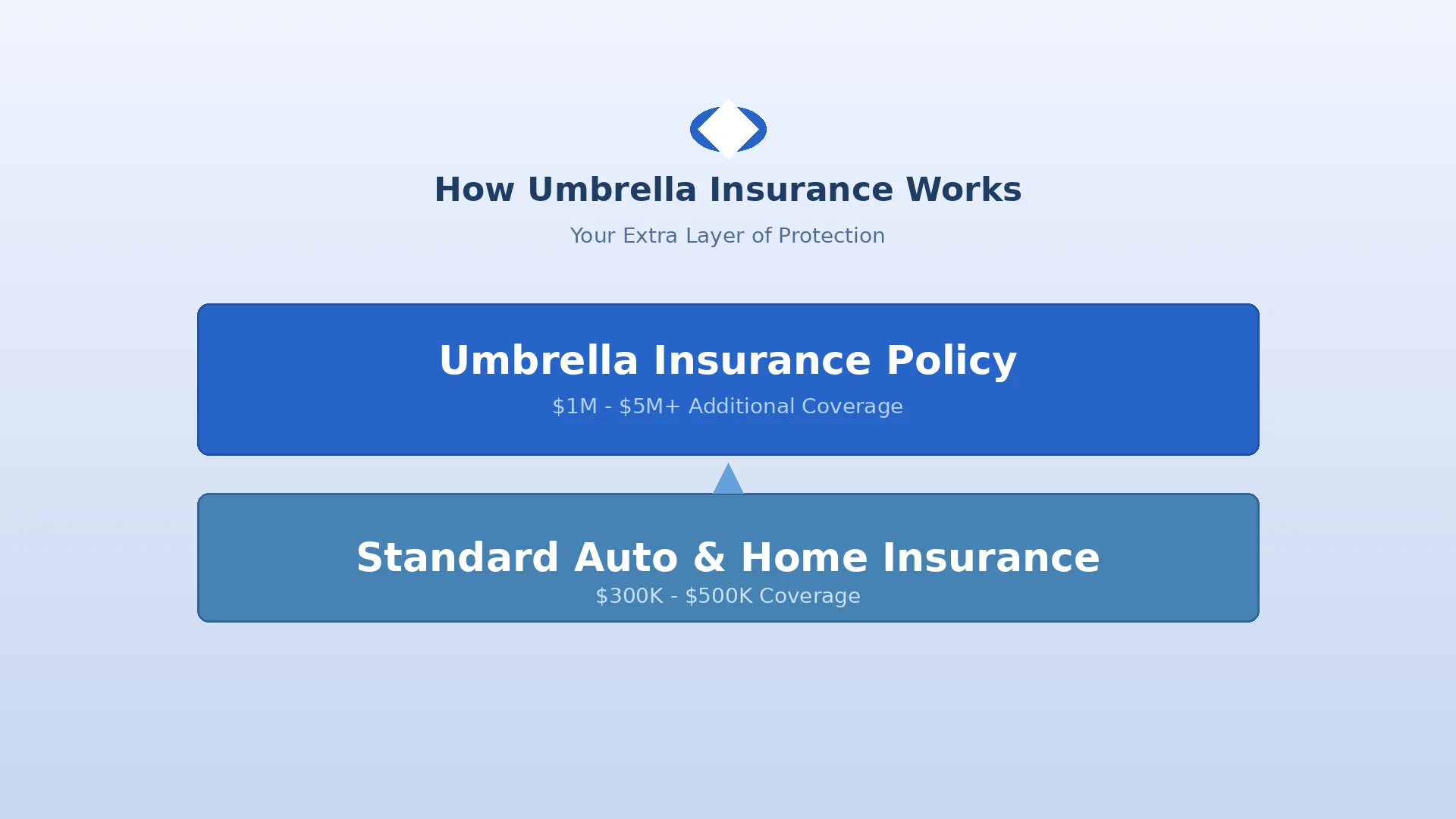

What Is Umbrella Insurance?

Umbrella insurance is a type of personal liability insurance that provides extra coverage beyond the limits of your underlying policies, including homeowners insurance, auto insurance, renters insurance, and watercraft insurance. It is called an “umbrella” because it extends broad protection over multiple existing policies under a single supplemental layer.

When a covered liability claim exceeds the limit of your primary policy, the umbrella policy kicks in to pay the difference, up to its own limit. Most umbrella policies start at $1 million in coverage and are available in increments up to $5 million or $10 million.

For example, if you carry $300,000 in liability coverage on your auto policy and are found liable for an accident resulting in a $1.2 million judgment, your auto insurance pays the first $300,000. Without umbrella insurance, you owe the remaining $900,000 out of pocket. With a $1 million umbrella policy, that gap is covered.

Umbrella insurance is classified as excess liability coverage. Unlike your primary policies, which cover specific assets or vehicles, an umbrella policy sits on top of everything and provides a unified additional layer of defense.

Key Features of Umbrella Insurance

- Excess liability coverage: Pays claims that exceed the limits of your underlying policies

- Broader protection: Covers certain liability claims that standard policies may exclude, such as libel, slander, defamation, and false arrest

- Drop-down coverage: Can act as primary coverage for claims not addressed by underlying policies, subject to a self-insured retention (SIR) or deductible

- Worldwide coverage: Most policies provide protection regardless of where the incident occurs

- Household coverage: Typically extends to all members of the policyholder’s household

How Does Umbrella Insurance Work?

Umbrella insurance functions as a second layer of protection. It does not replace your existing policies; it supplements them.

Here is how the process works in practice:

- An incident occurs where you are found liable for bodily injury, property damage, or personal injury to another person.

- Your primary policy responds first. Your auto, homeowners, or other relevant policy pays up to its liability limit.

- If the claim exceeds your primary limit, the umbrella policy activates and covers the remaining amount, up to its own limit.

- Legal defense costs are typically covered in addition to the policy limit, meaning they do not reduce your available coverage.

A Real-World Example

Suppose you host a gathering at your home and a guest slips on your patio, suffering a severe spinal injury. Medical expenses and lost wages total $1.5 million, and the guest sues. Your homeowners policy carries $500,000 in personal liability coverage. Here is how the claim breaks down:

| Layer | Amount Paid |

|---|---|

| Homeowners liability | $500,000 |

| Umbrella policy ($2 million) | $1,000,000 |

| Your out-of-pocket cost | $0 |

Without the umbrella policy, you would owe $1 million personally, potentially forcing you to liquidate assets, drain retirement savings, or face wage garnishment.

Drop-Down Coverage

One of the most valuable features of umbrella insurance is drop-down coverage. This means the umbrella can provide primary coverage for certain claims that your underlying policies do not cover at all. Examples include:

- Defamation or libel: If you are sued for something you said or wrote that damaged someone’s reputation

- False arrest or wrongful detention: If you are involved in a situation where someone claims they were unlawfully detained

- Invasion of privacy: Claims related to violating another person’s privacy

In these cases, you typically pay a self-insured retention (SIR), usually between $250 and $10,000, and the umbrella policy covers the rest.

What Does Umbrella Insurance Cover?

Umbrella insurance provides broad liability protection. While policy details vary by insurer, most umbrella policies cover:

Bodily Injury Liability

This is the most common type of umbrella claim. If someone is physically injured due to your negligence, whether in a car accident, at your home, or at another location, umbrella insurance covers medical bills, rehabilitation costs, lost wages, and pain and suffering damages beyond your primary policy limits.

According to industry data, approximately 78% of personal umbrella claims originate from auto accidents. A single serious car crash can generate medical and legal costs well into seven figures.

Property Damage Liability

If you accidentally damage someone else’s property and the costs exceed your primary coverage, your umbrella policy covers the excess. This can include situations like causing a multi-vehicle accident, accidentally starting a fire that spreads to a neighbor’s home, or damage caused by your watercraft.

Personal Injury Liability

Beyond physical injuries, umbrella policies cover personal injury claims, which include:

- Libel and slander: Written or spoken statements that damage someone’s reputation

- Defamation: False statements presented as facts that cause harm

- Wrongful eviction: If you are a landlord and a tenant claims unlawful eviction

- Malicious prosecution or false arrest: Claims arising from legal actions taken against another person

These types of claims are increasingly common in the age of social media, where a single post can lead to a defamation lawsuit.

Legal Defense Costs

Umbrella policies typically cover attorney fees, court costs, and other legal expenses associated with defending covered claims. In many cases, defense costs are paid in addition to the policy limit, so hiring an attorney does not reduce the coverage available to pay a judgment.

Landlord Liability

If you own rental properties, your umbrella policy generally extends to cover liability claims arising from those properties. This is particularly important for landlords who face exposure to tenant injury claims, premises liability, and habitability disputes.

What Umbrella Insurance Does Not Cover

Understanding exclusions is just as important as understanding coverage. Umbrella insurance does not cover:

- Your own injuries or property damage: Umbrella policies are liability-only. They protect you from claims by others, not from damage to your own property or injuries to yourself.

- Intentional acts: If you deliberately cause harm to another person or their property, no umbrella policy will cover the resulting claim.

- Business or professional liability: Personal umbrella policies do not cover claims arising from business activities. Business owners need commercial umbrella insurance or a separate commercial general liability policy.

- Contractual liability: Obligations you voluntarily assume under a contract are generally excluded.

- Workers’ compensation claims: These are handled by a separate workers’ compensation policy.

- Damage caused by certain breeds of dogs: Some insurers exclude specific breeds; others may cover them with restrictions.

- Damage from certain watercraft or vehicles: High-performance boats or vehicles may require separate endorsements. Boat and jet ski owners in particular benefit from umbrella policies. Learn more in our watercraft insurance guide.

If you have questions about specific exclusions, speak with an insurance advisor who can review your individual risk profile and recommend appropriate coverage.

How Much Does Umbrella Insurance Cost?

Umbrella insurance is one of the most affordable forms of coverage relative to the protection it provides. Here are typical costs:

| Coverage Amount | Annual Premium (Approximate) |

|---|---|

| $1 million | $150 to $350 |

| $2 million | $225 to $450 |

| $3 million | $300 to $550 |

| $5 million | $450 to $750 |

Several factors influence the exact cost of your umbrella policy:

- Number of properties you own: More properties mean more liability exposure

- Number of vehicles and drivers: Households with teen drivers or multiple vehicles typically pay more

- Driving record: A history of at-fault accidents or traffic violations raises premiums

- Owned watercraft or recreational vehicles: Boats, jet skis, and ATVs add liability exposure

- Rental properties: Landlords face higher premiums due to additional tenant-related risk

- Claim history: Previous umbrella or liability claims may increase costs

- Location: Premiums vary by state and metropolitan area

Most insurers require minimum underlying liability limits before issuing an umbrella policy. Common requirements include:

- Auto insurance: $250,000/$500,000 bodily injury liability (or $300,000 combined single limit)

- Homeowners insurance: $300,000 to $500,000 in personal liability coverage

Meeting these requirements may slightly increase your auto and homeowners premiums, but the total cost of the umbrella plus any underlying increases is typically modest.

Who Needs Umbrella Insurance?

The short answer: anyone whose assets and future income exceed their existing liability limits. But certain individuals and families face elevated risk and benefit most from umbrella coverage.

Homeowners

Owning a home automatically increases your liability exposure. Swimming pools, trampolines, tree houses, elevated decks, and even unfenced yards can all lead to injury claims from visitors, neighbors, or delivery workers. If someone is injured on your property and the claim exceeds your homeowners liability limit, an umbrella policy covers the difference.

Drivers and Families With Teen Drivers

Auto accidents are the single largest source of personal umbrella claims. If your household includes teen or young adult drivers, who statistically have higher accident rates, umbrella insurance becomes essential. A single at-fault accident causing severe injuries can easily generate a seven-figure judgment.

Landlords

Rental property owners face liability from tenant injuries, habitability claims, wrongful eviction lawsuits, and other premises-related incidents. Umbrella insurance extends coverage across all your rental properties.

High-Net-Worth Individuals

If you own significant assets, including investment portfolios, real estate, business equity, or high-value personal property such as jewelry, fine art, or watercraft, you are a larger target for lawsuits. An umbrella policy protects those assets from being seized to satisfy a judgment.

Dog Owners

Dog bite claims account for over one-third of all homeowners insurance liability payouts. The average cost of a dog bite claim is over $50,000, and severe cases can exceed $1 million.

Boat and Watercraft Owners

Boating accidents can result in serious injuries and substantial property damage. If you own a boat, jet ski, or other watercraft, umbrella insurance provides an additional layer of liability protection beyond your marine policy.

Volunteers and Community Leaders

Serving on a nonprofit board, coaching a youth sports team, or volunteering in other capacities can expose you to personal liability claims that umbrella insurance may cover under its personal injury provisions.

Active Social Media Users

In today’s digital environment, a social media post, review, or comment can lead to a defamation or libel lawsuit. Umbrella insurance provides drop-down coverage for these types of claims.

Ready to protect your assets? Request a personalized umbrella insurance quote from Insurance Underwriters, or call us at (305) 900-2823 for a no-obligation consultation.

How Much Umbrella Insurance Do You Need?

Calculate Your Net Worth

Start with your total assets: home equity, savings, investments, retirement accounts, vehicles, and valuable personal property. Your umbrella coverage should at least equal your net worth.

Factor in Future Earnings

A court judgment can garnish your future wages for years. If you earn a strong income, consider adding coverage to protect those future earnings as well.

Assess Your Risk Profile

Consider how many properties you own, whether you have a pool or trampoline, the number and ages of drivers in your household, pet ownership, watercraft, and your social or community activities. Higher risk means you should carry more coverage.

General Guidelines

| Net Worth | Recommended Coverage |

|---|---|

| Under $500,000 | $1 million |

| $500,000 to $1 million | $1 to $2 million |

| $1 million to $3 million | $2 to $3 million |

| Over $3 million | $3 to $5 million+ |

Since umbrella insurance is sold in $1 million increments and additional millions cost relatively little ($75 to $150 per year per additional million), it usually makes sense to buy slightly more coverage than you think you need.

Umbrella Insurance vs. Excess Liability Insurance

These terms are sometimes used interchangeably, but they are not the same:

| Feature | Umbrella Insurance | Excess Liability Insurance |

|---|---|---|

| Coverage scope | Broader; can cover claims not in underlying policies | Narrower; only extends limits of underlying coverage |

| Drop-down coverage | Yes; can act as primary for uncovered claims | No; strictly follows underlying policy terms |

| Policy form | Its own separate terms and conditions | Mirrors the underlying policy (follow-form) |

| Best for | Individuals and families needing broad protection | Businesses seeking higher limits on specific policies |

For most individuals and families, a true umbrella policy is the better choice because of its broader coverage and drop-down provisions.

How to Get Umbrella Insurance

- Review your current coverage: Check your auto, homeowners, and any other liability policy limits to ensure they meet the minimums required by umbrella insurers.

- Assess your risk profile: Consider your assets, income, properties, vehicles, and lifestyle factors.

- Talk to an insurance advisor: An experienced advisor can help you determine the right coverage amount and find a policy that fits your needs and budget.

- Bundle when possible: Many insurers offer discounts when you purchase umbrella coverage alongside your auto and homeowners policies.

Insurance Underwriters works with multiple carriers to find the right umbrella policy for your specific situation. Whether you need personal umbrella coverage, commercial umbrella insurance, or a combination of both, our team evaluates your total risk exposure and recommends a tailored solution.

Frequently Asked Questions

Is umbrella insurance worth it?

Yes. For a cost of roughly $150 to $350 per year, you get $1 million in additional liability protection. Considering that a single serious lawsuit can exceed your standard policy limits by hundreds of thousands or even millions of dollars, umbrella insurance delivers significant value relative to its cost.

Do I need umbrella insurance if I do not have many assets?

Even if your current assets are modest, a lawsuit judgment can target your future earnings for years. Umbrella insurance protects not just what you own today, but what you will earn in the future.

Does umbrella insurance cover my business?

A personal umbrella policy does not cover business-related claims. If you are a business owner, you need a commercial liability policy or commercial umbrella insurance. Insurance Underwriters offers both personal and commercial coverage solutions.

Can I get umbrella insurance without owning a home?

Yes. Renters can purchase umbrella insurance. You will need an underlying renters insurance policy with sufficient liability limits, and most insurers also require auto insurance.

How does umbrella insurance apply to rental properties I own?

Personal umbrella policies generally extend to residential rental properties you own, provided you have the required underlying landlord insurance policy in place. Talk to your advisor to ensure your rental properties are properly scheduled on the policy.

Does umbrella insurance cover dog bites?

In most cases, yes. Umbrella insurance covers dog bite claims that exceed your homeowners liability limits. However, some insurers exclude certain breeds or impose restrictions. Discuss your specific situation with your insurance advisor.

Protect What Matters Most

Life is unpredictable, and even the most careful individuals can face unexpected lawsuits and liability claims. Umbrella insurance provides a critical safety net, protecting your home, savings, investments, and future earnings from a single event that could otherwise cause lasting financial damage.

At Insurance Underwriters, we help individuals and families across the United States build comprehensive protection strategies that include umbrella coverage tailored to their specific needs and risk profiles.

Get a liability umbrella quote today, or call us at 305-900-2823 to discuss your coverage options with one of our experienced advisors.

Looking for coverage for your personal valuables? Read our comprehensive guide to jewelry insurance guide to understand your options for protecting engagement rings, watches, and collections.

Comments

Comments are closed.