Florida Auto Insurance: 2026 Law Changes & Rates

Let’s be honest: finding affordable Florida auto insurance is a challenge. We pay some of the highest car insurance premiums in the nation, with many drivers seeing annual costs soar past $2,300. Our state’s unique no-fault laws are also changing in 2026, adding another layer of complexity, especially for drivers in cities like Miami. Understanding your coverage options is more than just a legal requirement—it’s a critical step in protecting your finances. This guide will show you how to choose the right policy without overpaying. For more details, see our guide on travel insurance coverage.

Get a personalized auto insurance quote from Insurance Underwriters or call 305-900-2823 to speak with a Florida auto insurance specialist who can help you find the right coverage at the best price.

Key Takeaways

- Florida auto insurance is mandatory. All registered vehicles must carry minimum insurance coverage. Current requirements include $10,000 in Personal Injury Protection (PIP) and $10,000 in Property Damage Liability (PDL).

- Major changes take effect July 1, 2026. Florida eliminates its no-fault PIP system and shifts to a fault-based liability model requiring 25/50/10 bodily injury and property damage coverage.

- Florida drivers pay an average of $2,305 per year for auto insurance ($192/month), with full coverage averaging $2,716 annually.

- Miami has the highest rates in Florida, with drivers paying an average of $3,287 to $4,901 per year depending on coverage levels.

- Uninsured/underinsured motorist coverage is critical because roughly 20% of Florida drivers carry no insurance at all.

Florida’s 2026 Auto Insurance Changes: What You Need to Know

Florida law requires every vehicle owner to maintain auto insurance as a condition of vehicle registration. The state’s insurance requirements are changing significantly in 2026, making it critical to understand both current and upcoming mandates.

Florida’s Minimum Coverage (Until July 2026)

Until the new law takes effect, Florida operates under a no-fault insurance system requiring two types of coverage:

- Personal Injury Protection (PIP): $10,000 minimum. Covers your own medical expenses, lost wages (60%), and death benefits regardless of who caused the accident.

- Property Damage Liability (PDL): $10,000 minimum. Covers damage you cause to other people’s property.

Under this system, drivers file claims with their own insurance after an accident, regardless of fault. PIP includes a critical 14-day rule: you must seek medical treatment within 14 days of an accident to qualify for benefits. If your injury is not classified as an emergency medical condition, PIP benefits cap at $2,500 instead of $10,000.

What’s Changing on July 1, 2026?

Florida is eliminating its 50-year-old no-fault system and transitioning to a fault-based liability model. The new minimum coverage requirements, known as “25/50/10,” include:

- Bodily Injury Liability: $25,000 per person / $50,000 per accident

- Property Damage Liability: $10,000 per accident

- Medical Payments (MedPay): $5,000 (replaces PIP’s medical coverage component)

Under the new system, the person who causes an accident becomes responsible for the other party’s damages. This is a fundamental shift that changes how every accident claim is handled in Florida.

Florida Auto Insurance Laws You Need to Know

Florida’s insurance laws are specific and strictly enforced. Whether you’re a lifelong resident, a new transplant, or just spending the winter here, knowing the rules is the first step to staying protected and avoiding serious penalties. From maintaining continuous coverage to understanding the requirements for your specific situation, these regulations form the foundation of your responsibilities as a Florida driver. Getting it right from the start saves you time, money, and a lot of potential headaches down the road. Let’s walk through the essential laws every driver in the Sunshine State should know.

Rules for Vehicle Registration and Coverage

Staying compliant with Florida’s auto insurance laws starts with understanding the rules tied directly to your vehicle’s registration. These regulations are not suggestions; they are strict requirements that every vehicle owner must follow to legally operate on state roads. From the moment you register your car, you are responsible for maintaining specific types of coverage without any gaps. Failing to follow these procedures can lead to severe penalties, including the loss of your driving privileges. Here’s a breakdown of the core rules you need to manage.

Continuous Coverage Requirement

To legally register and operate a vehicle in Florida, you must maintain continuous insurance coverage. The state mandates that every driver carry a minimum of $10,000 in Personal Injury Protection (PIP) to cover your own medical bills and $10,000 in Property Damage Liability (PDL) to pay for damages you cause to another person’s property. According to the Florida Department of Highway Safety and Motor Vehicles, this isn’t a one-time requirement at registration; the coverage must remain active for as long as your vehicle has a valid Florida license plate. This ensures that all drivers on the road have a baseline of financial responsibility.

Penalties for a Coverage Lapse

Letting your auto insurance lapse in Florida carries significant consequences. If you fail to maintain the required PIP and PDL coverage, the state can suspend your driving privileges, vehicle registration, and license plate for up to three years. It’s important to understand that there are no hardship or temporary licenses granted for this type of suspension, meaning you could be left without the ability to drive legally for an extended period. Reinstating your license and registration after a lapse also involves paying hefty fees, which can range from $150 to $500, making a coverage gap a very costly mistake.

How to Cancel Your Insurance Correctly

If you plan to sell your car or move out of state, there is a specific process you must follow to cancel your Florida auto insurance without facing penalties. Before you contact your insurance provider to terminate your policy, you must first surrender your Florida license plate and registration at a driver license office or tax collector’s office. This action officially informs the state that the vehicle is no longer in operation in Florida. By turning in your plate first, you prevent the system from flagging your vehicle for a coverage lapse, which would trigger an automatic suspension and associated fines.

Working With a Licensed Florida Insurer

Your auto insurance policy is only valid for registration purposes if it is issued by an insurance company that is officially licensed to do business in Florida. Using an out-of-state provider, even if you have a policy with them in another state, will not satisfy Florida’s legal requirements. This rule ensures that the insurer is financially sound and compliant with state regulations designed to protect consumers. Partnering with an experienced brokerage like InsuranceUnderwriters.com guarantees that you are placed with a reputable, state-licensed carrier, ensuring your policy is fully compliant while also helping you find the most competitive rates available.

Rules for New and Temporary Residents

Florida’s popularity means a constant flow of new and temporary residents, and the state has clear insurance rules to accommodate them. Whether you’re a “snowbird” escaping colder climates for a few months or making a permanent move to the Sunshine State, you need to know when and how to secure Florida-compliant auto insurance. Understanding these timelines is essential for a smooth transition and helps you avoid the fines and registration issues that can arise from not complying with local laws in a timely manner. Here’s what you need to know about establishing your auto insurance as a temporary or new resident.

The 90-Day Rule for Temporary Stays

Florida’s insurance laws also apply to part-time residents and long-term visitors. If you have a vehicle in Florida for more than 90 days over a 365-day period, you are required to purchase Florida PIP and PDL coverage. This rule, often relevant for seasonal residents or those on extended work assignments, is cumulative and does not require the 90 days to be consecutive. According to the Florida Department of Financial Services, this ensures that even temporary drivers contribute to the state’s system and have appropriate coverage while using its roads.

Insurance Requirements for New Residents

The timeline for becoming a Florida resident for insurance purposes is faster than many people expect. If you move to the state and either accept employment or enroll your children in a public school, you have just 10 days to register your vehicle in Florida. This process includes getting a Florida license plate and securing a Florida-compliant auto insurance policy that meets the state’s minimum requirements. Waiting longer than this 10-day grace period can result in fines and complications with your registration, so it’s a critical first step to take care of immediately upon establishing these residency ties.

Moving Out of Florida

Just as there’s a correct way to start your insurance in Florida, there’s a correct way to end it when you move. You should not cancel your Florida auto policy until after you have successfully registered your vehicle in your new state of residence. Once you have your new plates and registration, you can then surrender your Florida plates and cancel your old policy. This order of operations is crucial because it prevents a potential coverage lapse in Florida’s system, which could lead to a suspension of your Florida driver’s license, even if you no longer live there.

Special Cases and Exceptions

While the standard insurance rules apply to most drivers, Florida law recognizes that some situations require a different approach. From commercial vehicles that carry greater risk to the unique circumstances of military personnel, the state has specific provisions and exceptions. It’s also possible, though rare, for individuals or businesses to self-insure if they meet very strict financial criteria. These special cases highlight the importance of understanding that auto insurance isn’t a one-size-fits-all product. Your specific needs determine the type and amount of coverage you are legally required to carry.

Requirements for Taxis and Commercial Vehicles

The standard minimum insurance requirements do not apply to all vehicles. Taxis, for example, are subject to stricter rules and must carry higher limits of Bodily Injury Liability (BIL) and Property Damage Liability (PDL) coverage to protect their passengers and the public. Similarly, other commercial vehicles have their own unique insurance needs based on their use, weight, and the goods they transport. If you operate a business vehicle, it’s essential to secure a commercial auto policy that is specifically designed to cover those risks, as a personal policy will not provide adequate protection.

Considerations for Military Members

Active-duty military members often face unique circumstances, and Florida’s insurance laws provide some flexibility. If you are a Florida resident in the military but are stationed in another state, you may not be required to maintain Florida PIP coverage, provided your vehicle is not physically in Florida. However, the rules can be complex, and it’s always best to verify your specific requirements with the FLHSMV and your insurance advisor to ensure you remain compliant while serving out of state. This prevents any unintended penalties or issues with your registration while you are away on duty.

The Self-Insurance Option

While most drivers purchase a policy from an insurer, Florida law does allow for a self-insurance option, though it is quite rare. To qualify, an individual or company must demonstrate significant financial stability by providing a substantial bond or proof of net worth to the state. This essentially means you are setting aside your own funds to cover potential claims up to the required limits. Because the financial threshold is so high, this option is typically only feasible for large corporations or exceptionally high-net-worth individuals who can meet the state’s strict self-insurance certificate requirements.

Your Florida Auto Insurance Options, Explained

Understanding each coverage type helps you build a policy that protects your finances without overpaying. Here is a breakdown of every coverage type available to Florida drivers.

Liability Coverage

Liability coverage is the foundation of any auto insurance policy and will become the primary required coverage in Florida starting July 2026. It includes:

- Bodily Injury Liability (BIL): Pays for medical expenses, lost wages, pain and suffering, and legal defense costs when you cause injury to another person in an accident.

- Property Damage Liability (PDL): Covers the cost to repair or replace property you damage in an accident, including other vehicles, fences, buildings, and guardrails.

While the new Florida minimums are 25/50/10, insurance advisors recommend carrying at least 100/300/100 to protect against the full cost of a serious accident. A single hospitalization can easily exceed $100,000 in medical bills.

Collision Coverage

Collision coverage pays to repair or replace your own vehicle after an accident with another vehicle or object, regardless of fault. This coverage is optional under Florida law but is typically required by lenders if your vehicle is financed or leased.

Comprehensive Coverage

Comprehensive coverage protects your vehicle from non-collision events. In Florida, this coverage is particularly important due to the state’s exposure to hurricanes, tropical storms, flooding, and hail. It also covers theft, vandalism, fire, falling objects, and animal strikes.

Personal Injury Protection (PIP) and MedPay

PIP is currently mandatory in Florida ($10,000 minimum) but will be eliminated on July 1, 2026. It covers 80% of medical expenses and 60% of lost wages regardless of fault. The replacement, Medical Payments coverage (MedPay), will provide $5,000 in medical expense coverage for you and your passengers after an accident.

Breaking Down PIP Benefits

Think of Personal Injury Protection (PIP) as your first line of financial defense after an accident. As the foundation of Florida’s current no-fault system, it provides up to $10,000 to cover your own essential costs, regardless of who was at fault. This includes 80% of your medical bills, 60% of lost wages if you can’t work, and death benefits. This immediate access to funds is designed to help you start recovering without waiting for a lengthy fault determination process.

However, there are a couple of important rules to know. First is the 14-day rule: you must seek medical treatment within two weeks of the accident to be eligible for your full PIP benefits. If you wait longer, you could forfeit your claim. Second, the full $10,000 is only available if a medical professional diagnoses you with an “emergency medical condition.” Otherwise, your benefits are capped at just $2,500. This makes getting a prompt and thorough medical evaluation absolutely critical after any accident.

Uninsured/Underinsured Motorist Coverage (UM/UIM)

With approximately 20% of Florida drivers carrying no insurance, UM/UIM coverage is one of the most important protections you can add to your policy. It covers your medical bills and damages when the at-fault driver has no insurance or not enough insurance to cover your losses. This coverage becomes even more critical under the new fault-based system starting in 2026.

Additional Optional Coverages to Consider

Beyond the standard liability and physical damage protections, several other coverages can add significant financial security and convenience to your policy. While not required by law, these options address specific situations that can otherwise lead to major out-of-pocket costs and logistical headaches. Think of them as valuable tools that help you build a policy tailored to your vehicle and lifestyle, ensuring your protection matches your real-world needs without unnecessary expense.

Loan/Lease Gap Coverage

If you finance or lease your vehicle, gap coverage is a financial lifesaver. A new car’s value depreciates the moment you drive it off the lot, and it often drops faster than you pay down your loan. If your car is totaled in an accident, your collision or comprehensive coverage will only pay its actual cash value at the time of the loss. This amount can be thousands of dollars less than what you still owe your lender. Gap coverage pays that difference, preventing you from making payments on a car you can no longer drive and protecting your finances from a significant and unexpected debt.

Rental Car Reimbursement

Life doesn’t pause when your car is in the repair shop. Rental car reimbursement coverage helps you stay mobile by covering the cost of a rental vehicle while yours is being fixed after a covered claim. This is especially useful in a state like Florida, where daily life often depends on having a car. Instead of scrambling for rides or relying on limited public transportation, this affordable add-on ensures you can continue your daily routine—getting to work, running errands, and managing family commitments—with minimal disruption. It’s a small price for maintaining your independence and avoiding the high cost of last-minute rental fees after an accident.

Roadside Assistance

There’s never a good time for a flat tire, a dead battery, or locking your keys in the car. Roadside assistance coverage offers peace of mind for these unexpected and stressful situations. For a minimal addition to your premium, you gain access to a network of professionals who can provide towing, battery jump-starts, fuel delivery, and lockout services 24/7. It saves you the hassle of searching for a reputable tow truck company and paying steep, one-time fees out of pocket. This coverage is a simple and cost-effective way to ensure you’re never truly stranded when a minor roadside emergency occurs.

Which Florida Auto Insurance Coverage Is Right for You?

| Coverage Type | What It Covers | Required in FL? | Typical Cost Impact |

|---|---|---|---|

| Bodily Injury Liability | Other people’s injuries you cause | Required after July 1, 2026 (25/50) | Major premium component |

| Property Damage Liability | Other people’s property you damage | Yes ($10,000 min) | Moderate |

| PIP (through 6/30/2026) | Your medical bills, lost wages | Yes ($10,000 min) until 7/1/2026 | Moderate |

| MedPay (after 7/1/2026) | Your medical expenses after accident | Required ($5,000 min) after 7/1/2026 | Low to moderate |

| Collision | Your vehicle (accident damage) | No (lenders may require) | Moderate to high |

| Comprehensive | Your vehicle (theft, weather, etc.) | No (lenders may require) | Low to moderate |

| UM/UIM | Your injuries from uninsured drivers | No (strongly recommended) | Low to moderate |

How Much Does Auto Insurance Cost in Florida?

Florida ranks among the most expensive states for auto insurance. Here are the current average costs based on 2026 data:

- Average annual premium: $2,305 ($192/month)

- Full coverage average: $2,716 per year ($226/month)

- Minimum coverage average: $1,731 per year ($144/month)

These figures represent state averages. Your actual premium depends on your driving record, age, vehicle, ZIP code, coverage limits, and credit history.

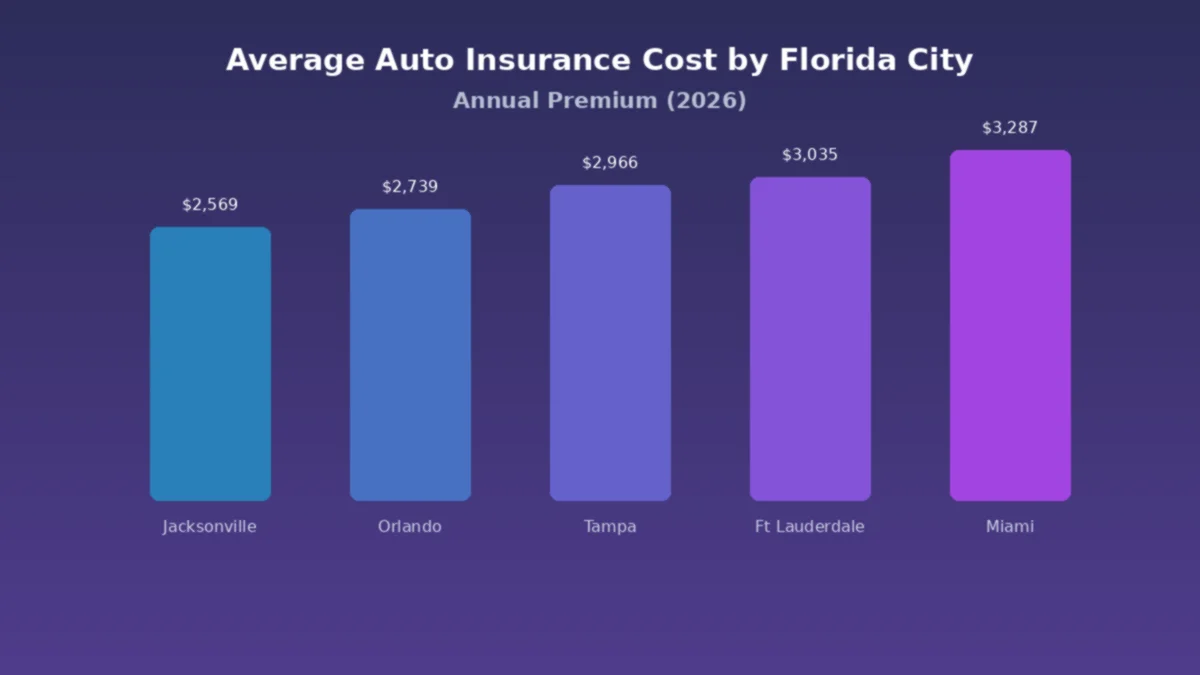

Average Car Insurance Costs by Florida City

Where you live in Florida significantly impacts your premiums. Urban areas with higher traffic density, accident rates, and vehicle theft produce higher insurance costs.

| City | Average Annual Cost | Difference from State Average |

|---|---|---|

| Jacksonville | $2,569 | +$264 |

| Orlando | $2,739 | +$434 |

| Tampa | $2,966 | +$661 |

| Fort Lauderdale | $3,035 | +$730 |

| Miami | $3,287 | +$982 |

Miami drivers face the highest auto insurance costs in Florida, paying nearly $1,000 more than the state average annually. Insurance Underwriters is headquartered in Miami and understands the unique challenges South Florida drivers face when it comes to finding affordable, comprehensive coverage.

How Your Age Affects Your Insurance Rate

| Age Group | Average Annual Cost (FL) |

|---|---|

| 16-year-old | $5,984 |

| 18-year-old | $4,855 |

| 20s | $2,367 |

| 30s | $1,794 |

| 40s | $1,756 |

| 50s | $1,641 |

| 60s | $1,672 |

| 70s | $2,028 |

What Factors Affect Your Florida Auto Insurance Rates?

Insurance companies evaluate multiple risk factors to calculate your premium. Understanding these factors helps you take steps to lower your costs.

Driving record. Accidents, traffic violations, and DUI convictions significantly increase premiums. A single at-fault accident adds approximately $598 per year to your Florida auto insurance costs. A DUI adds roughly $2,740 annually.

Age and driving experience. Teen drivers pay three to four times more than experienced adults. Premiums decrease steadily through your 30s, 40s, and 50s before increasing slightly for seniors over 70.

Location. Your ZIP code is one of the strongest pricing factors. Miami, Fort Lauderdale, and Tampa consistently have higher rates than Jacksonville or smaller cities due to population density, traffic, and claim frequency.

Vehicle type. Newer, more expensive vehicles cost more to insure. Sports cars and luxury vehicles carry higher premiums than sedans or minivans. Safety features and crash test ratings also affect your rate.

Coverage limits and deductibles. Higher liability limits provide better protection but increase your premium. Higher deductibles lower your premium but increase your out-of-pocket cost when filing a claim.

Credit history. Florida insurers use credit-based insurance scores to help determine rates. Drivers with higher credit scores typically pay lower premiums.

Annual mileage. The more you drive, the higher your risk of an accident. Drivers with shorter commutes or lower annual mileage often qualify for reduced rates.

Why Is Auto Insurance So Expensive in Florida?

Florida auto insurance costs rank among the highest in the country for several interconnected reasons:

- High uninsured driver rate. Nearly 20% of Florida drivers carry no insurance, which shifts costs to insured drivers through UM/UIM claims and higher premiums.

- Severe weather exposure. Florida faces hurricanes, tropical storms, flooding, and hail that generate billions in comprehensive claims each year.

- High population density and tourism. Florida is the third most populous state with over 22 million residents plus millions of annual tourists, creating heavy traffic and more accidents.

- Fraud. Florida has historically had some of the highest auto insurance fraud rates in the nation, particularly staged accidents and inflated medical claims under the PIP system.

- Litigation costs. Before the 2023 tort reform, Florida’s legal environment contributed to higher claim costs. The 2023 reforms and 2026 PIP elimination aim to reduce these costs over time.

Talk to an Insurance Underwriters advisor about strategies to reduce your Florida auto insurance premium without sacrificing the coverage you need. Call 305-900-2823 for a free consultation.

Florida Rates vs. the National Average

It’s no secret that Florida is one of the most expensive states for auto insurance. When you look at the numbers, it becomes clear just how much drivers are paying compared to other parts of the country. The average annual premium in the Sunshine State is around $2,305, which breaks down to about $192 per month. For those with full coverage, that figure climbs to $2,716 annually, while minimum coverage averages $1,731. Of course, your location within the state plays a huge role. Drivers in Miami, for example, often pay nearly $1,000 more per year than the state average, a challenge we understand well as a Miami-based brokerage. Your actual premium will depend on your unique profile, but these averages highlight the high-cost environment all Florida drivers face.

Other Factors Driving Up Costs

So, why are Florida’s rates so high? It’s a combination of unique environmental, demographic, and legal factors that create a perfect storm for insurers. A significant issue is the sheer number of uninsured drivers—nearly one in five people on the road have no coverage, shifting the financial burden onto insured drivers when accidents happen. The state’s constant exposure to severe weather like hurricanes and flooding leads to a high volume of expensive comprehensive claims. Add in a dense population, millions of annual tourists creating congested roads, and a history of widespread insurance fraud, and you have a recipe for some of the highest premiums in the nation. While recent legal reforms aim to address litigation costs, these other core issues continue to drive up prices for everyone.

7 Ways to Save on Florida Auto Insurance

Florida drivers can take several concrete steps to reduce their auto insurance costs without compromising essential coverage.

1. Shop Around and Compare Quotes

Rates vary significantly between insurers. Working with an independent insurance brokerage like Insurance Underwriters gives you access to quotes from multiple carriers so you can compare coverage and pricing in one place.

Information Needed for an Accurate Quote

To make the comparison process as smooth and effective as possible, it helps to have a few key pieces of information ready. When you request a quote, providing complete and accurate details allows an advisor to build a policy that truly fits your needs and uncover every discount you’re eligible for. Think of it as preparing a clear snapshot of your household’s driving profile. This ensures the quotes you receive aren’t just generic estimates but are tailored specifically to you, preventing any surprises down the road and helping you make a confident decision about your coverage. Be prepared to provide:

- Driver Details: Full name, date of birth, and driver’s license number for every licensed driver in your home. This helps insurers accurately assess the driving experience of everyone who will be using the vehicles.

- Vehicle Information: The year, make, model, and Vehicle Identification Number (VIN) for each car. You can usually find the VIN on your vehicle’s dashboard on the driver’s side or on your current insurance card. The VIN provides specific details about your car’s safety features, which can impact your rate.

- Driving and Claims History: A clear record of any accidents, tickets, or claims for all drivers over the past three to five years. Honesty here is key, as insurers will pull official reports anyway. Being upfront helps your advisor find the right carrier for your specific history.

- Current Insurance Policy: Your current policy’s declarations page is incredibly useful. It outlines your exact coverage limits and deductibles, allowing for a true apples-to-apples comparison to ensure you maintain or improve your protection without any gaps.

2. Bundle Your Home and Auto Insurance

Combining your auto insurance with homeowners insurance, umbrella insurance, or other policies often qualifies you for multi-policy discounts ranging from 5% to 25%. Visit our house insurance page for homeowners coverage options.

3. Keep Your Driving Record Clean

Every accident and violation you avoid keeps your rates lower. Some insurers offer accident forgiveness programs for long-term customers with clean records.

4. Choose a Higher Deductible

Raising your collision and comprehensive deductible from $500 to $1,000 or $2,500 can reduce your premium by 15% to 30%. This strategy works best if you have savings to cover the higher out-of-pocket cost.

5. Don’t Forget to Ask for Discounts

Common discounts include safe driver, good student, defensive driving course, anti-theft device, low mileage, military/veteran, and pay-in-full discounts. Ask your insurance advisor which discounts apply to your situation.

6. Re-evaluate Your Coverage Every Year

As your vehicle ages and depreciates, you may want to adjust collision and comprehensive coverage. An annual policy review with your insurance advisor ensures you are not overpaying for coverage you no longer need.

7. Work on Your Credit Score

Since Florida insurers factor credit into pricing, improving your credit score through on-time payments, reducing debt, and correcting errors on your credit report can translate to lower insurance premiums over time.

Florida’s No-Fault to At-Fault Transition: What It Means for You

The shift from Florida’s no-fault system to an at-fault model on July 1, 2026, represents the most significant change to the state’s auto insurance landscape in over 50 years. Here is what you need to know.

How the Current No-Fault System Works

Under the current system, after an accident you file a claim with your own insurance (PIP) regardless of who caused the crash. This system was designed to reduce lawsuits and speed up medical payments.

What Changes Under the At-Fault System

Starting July 1, 2026, the at-fault driver’s insurance becomes responsible for the other party’s damages. This means:

- Fault determination becomes central to every accident claim

- The at-fault driver’s bodily injury liability coverage pays the injured party’s medical bills and damages

- Under Florida’s modified comparative negligence rule (enacted in 2023), you cannot recover damages if you are 51% or more at fault

- Your personal health insurance becomes more important for covering immediate medical costs while fault is determined

How to Prepare for the Transition

- Review your current policy to understand your liability limits

- Consider increasing your bodily injury liability beyond the 25/50 minimums to protect your personal assets

- Add or increase UM/UIM coverage to protect yourself against uninsured drivers

- Verify your health insurance covers auto accident injuries, since PIP will no longer provide immediate medical coverage

- Contact your insurance advisor to discuss how the changes affect your specific situation

Do You Need an SR-22 or FR-44 in Florida?

If your license has been suspended or revoked due to serious traffic violations, you may need to file an SR-22 or FR-44 certificate with the Florida Highway Safety and Motor Vehicles (FLHSMV) to reinstate your driving privileges.

What Is an SR-22?

An SR-22 is a Certificate of Financial Responsibility, not a separate insurance policy. Your insurer files it electronically with FLHSMV to confirm you carry the required minimum liability coverage (currently 10/20/10: $10,000 bodily injury per person, $20,000 per accident, $10,000 property damage).

SR-22 filings are typically required for:

- Driving without insurance

- At-fault accidents while uninsured

- Reckless driving convictions

- Excessive point accumulation leading to suspension

The filing fee is generally $15 to $25, and you must maintain continuous coverage for three years. Any lapse in coverage triggers an SR-26 cancellation notice to the state, which can result in immediate license suspension.

What Is an FR-44?

Florida uses the FR-44 for DUI and DWI convictions. The FR-44 requires significantly higher liability limits than the SR-22, which makes it more expensive. If your notice specifies FR-44, an SR-22 filing will not satisfy the requirement.

Insuring a Teen Driver in Florida? Here’s What to Know

New and teen drivers face the highest auto insurance premiums in Florida. A 16-year-old driver pays an average of $5,984 per year, roughly three times more than a driver in their 40s or 50s.

Why Are Teen Insurance Rates So High?

Insurers base rates on risk, and statistics show that drivers aged 16 to 19 are significantly more likely to be involved in crashes due to inexperience. This elevated risk translates directly into higher premiums.

How to Save on Teen Car Insurance

- Add the teen to a parent’s policy rather than purchasing a separate policy, which is almost always cheaper

- Good student discount: Many insurers offer 5% to 15% discounts for students maintaining a B average or better

- Defensive driving courses: Florida-approved courses can reduce premiums

- Choose a safe, practical vehicle: Insuring a used sedan costs far less than insuring a sports car or new SUV

- Telematics programs: Usage-based insurance programs that monitor driving habits can reward safe teen drivers with lower rates

How to File an Auto Insurance Claim in Florida

The claims process in Florida depends on when the accident occurs relative to the July 2026 transition.

Filing a Claim Before July 1, 2026

- Seek medical attention within 14 days. This is a strict requirement under PIP. Missing this deadline can forfeit your benefits entirely.

- Report the accident to law enforcement if required (injuries, death, or property damage over $500).

- File a claim with your own insurance regardless of fault. Your PIP coverage handles your medical expenses and lost wages first.

- Document everything: photos of damage, police report number, witness information, medical records.

- For property damage claims, file against the at-fault driver’s PDL coverage.

Filing a Claim After July 1, 2026

- Document the accident thoroughly with photos, witness statements, and the police report. Fault determination is now critical.

- Seek medical attention promptly and use your MedPay or health insurance for immediate treatment.

- File a claim against the at-fault driver’s insurance for bodily injury and property damage.

- If you are not at fault, the other driver’s bodily injury liability coverage pays your medical bills and damages.

- If fault is disputed, Florida’s modified comparative negligence rule applies. You cannot recover if you are 51% or more at fault.

Is It Time to Increase Your Auto Insurance Coverage?

Florida’s minimum coverage requirements provide a legal baseline, but minimums rarely provide adequate financial protection. Consider increasing your coverage if:

- You have significant assets (home, savings, investments) that could be at risk in a lawsuit exceeding your policy limits

- You commute in heavy traffic, especially in Miami, Fort Lauderdale, Tampa, or Orlando

- You finance or lease your vehicle, which typically requires full coverage including collision and comprehensive

- You have a new or expensive vehicle that would be costly to repair or replace

- You have teen drivers on your policy who face higher accident risk

- You want protection against uninsured drivers, which is critical in Florida given the 20% uninsured rate

An umbrella insurance policy provides an additional layer of liability protection above your auto and homeowners insurance limits, typically in $1 million increments.

How to Choose the Best Florida Auto Insurance Policy

Auto insurance in Florida is complex, expensive, and undergoing its most significant regulatory change in over five decades. Whether you are navigating the no-fault to at-fault transition, looking for ways to lower your premiums in Miami, or insuring a teen driver for the first time, working with an experienced insurance advisor makes the process straightforward.

Insurance Underwriters specializes in personal auto insurance for Florida drivers. Our team evaluates your specific situation, compares options across top-rated carriers, and structures a policy that balances protection with cost efficiency.

Get a Florida auto insurance quote today or call 305-900-2823 to speak with a personal auto insurance specialist.

Major Insurance Companies in Florida

The Florida auto insurance market is home to several major national providers, each with its own strengths. Understanding the key players can help you know what to look for when comparing quotes. Here are some of the most recognizable names you’ll encounter:

- State Farm: With a massive network of local agents, State Farm has over a century of experience and offers personalized service for everything from teen driver policies to electric vehicle coverage.

- Geico: Known for its competitive pricing, Geico is a popular choice for drivers looking to meet Florida’s insurance requirements affordably.

- Progressive: This carrier is recognized for its user-friendly online tools that help customers build a policy that fits their specific budget.

- Allstate: Offering a wide array of coverage options and discounts, Allstate is a strong choice for drivers who value bundling policies or being rewarded for safe driving habits.

- Travelers: A long-standing insurer, Travelers provides comprehensive coverage options and tools to help customers effectively manage their policies.

While these companies are major players, the best choice always depends on your unique circumstances. Working with an independent brokerage like Insurance Underwriters allows you to compare quotes from these carriers and others, ensuring you get the right protection at a competitive price without having to shop each one individually.

Frequently Asked Questions

Is auto insurance required in Florida?

Yes. Florida law requires all registered vehicle owners to maintain auto insurance. Currently, the minimum is $10,000 in PIP and $10,000 in PDL. Starting July 1, 2026, the requirement changes to $25,000/$50,000 in bodily injury liability and $10,000 in property damage liability, plus $5,000 in MedPay.

Why is auto insurance so expensive in Florida?

Florida auto insurance rates are among the highest in the country due to a combination of factors: approximately 20% of drivers are uninsured, the state faces severe weather events (hurricanes, flooding), high population density and tourism create heavy traffic, and Florida has historically had high rates of insurance fraud. The 2023 tort reforms and 2026 PIP elimination aim to reduce costs over time.

What is the average cost of auto insurance in Florida?

The average Florida driver pays approximately $2,305 per year ($192 per month) for auto insurance. Full coverage averages $2,716 per year ($226/month), while minimum coverage averages $1,731 per year ($144/month). Miami drivers pay the most at $3,287 to $4,901 annually.

What happens to PIP coverage on July 1, 2026?

PIP (Personal Injury Protection) will be eliminated on July 1, 2026, under Senate Bill 54. Florida is transitioning from a no-fault system to a fault-based liability model. PIP will be replaced by mandatory bodily injury liability coverage (25/50) and $5,000 in Medical Payments (MedPay) coverage.

What is considered full coverage auto insurance in Florida?

Full coverage typically combines liability insurance (bodily injury and property damage), collision coverage, and comprehensive coverage. It may also include uninsured/underinsured motorist coverage and MedPay. Full coverage is not a legal term but generally means you have protection for both damage you cause to others and damage to your own vehicle.

How much auto insurance do I need in Florida?

While minimums are 25/50/10 (starting July 2026), insurance professionals recommend at least 100/300/100 in liability coverage. You should also consider collision, comprehensive, and UM/UIM coverage. The right amount depends on your assets, vehicle value, driving habits, and risk tolerance. An insurance advisor can help you determine adequate coverage levels.

Comments

Comments are closed.