What Is Jewelry Insurance? How It Really Works

That engagement ring on your finger or the family heirloom in your jewelry box is more than just an asset. It’s a story. It’s a memory. But what happens if it’s lost, stolen, or damaged? Many people assume their homeowners or renters policy has them covered, but that’s a costly mistake. These standard policies often cap jewelry coverage at a shockingly low $1,500, leaving your most precious pieces vulnerable. Getting the right jewelry insurance isn’t just a smart financial move; it’s how you protect what’s truly irreplaceable.

If you own valuable jewelry, you need dedicated coverage. Contact Insurance Underwriters at 305-900-2823 to get a personalized jewelry insurance quote today.

Jewelry insurance is a specialized form of coverage designed to protect your most valuable personal items from loss, theft, damage, and even mysterious disappearance. Whether you recently purchased an engagement ring or you have built a significant collection over decades, understanding your insurance options is the first step toward real peace of mind.

This guide covers everything you need to know about insuring your jewelry, from the different policy types available to cost factors, appraisal requirements, the claims process, and how to make sure you never face a devastating uninsured loss.

So, What Exactly Is Jewelry Insurance?

Jewelry insurance is a type of personal property coverage that specifically protects high-value jewelry items. Unlike a standard homeowners or renters policy, which groups jewelry under “personal property” with low sub-limits, jewelry insurance provides full coverage based on the appraised value of each individual piece.

There are two primary ways to structure jewelry insurance:

- Scheduled personal property endorsement (rider/floater): An add-on to your existing homeowners or renters policy that lists individual jewelry items and their appraised values.

- Standalone jewelry insurance policy: A separate policy from a specialty insurer that covers your jewelry independently from your home or renters insurance.

Both options provide significantly more protection than relying on your base homeowners or renters policy alone. The right choice depends on your collection size, total value, and coverage needs.

What Does Your Jewelry Insurance Policy Cover?

A comprehensive jewelry insurance policy typically covers:

- Theft: Protection if your jewelry is stolen during a burglary, robbery, or pickpocketing incident.

- Accidental damage: Coverage for broken prongs, chipped gemstones, cracked settings, or other physical damage.

- Loss: Protection if you lose a piece of jewelry, including dropping it down a drain or leaving it behind while traveling.

- Mysterious disappearance: Coverage when a piece goes missing without a clear explanation of how it was lost. Not all policies include this, so verify before purchasing.

- Fire and natural disasters: Protection against damage from fires, floods, earthquakes, and other catastrophic events.

- Worldwide coverage: Most jewelry policies protect your items anywhere in the world, not just inside your home.

Specific Coverage Features to Look For

Not all jewelry insurance policies are the same. The fine print contains crucial details that determine how well your assets are actually protected. When you’re comparing options, it’s important to look beyond the premium and examine the specific features included in the coverage. A great policy anticipates potential issues and provides solutions before they become major problems. Think of it as a proactive strategy for protecting your most cherished items. The best coverage offers comprehensive protection that accounts for everything from routine upkeep to market fluctuations, ensuring you’re never caught off guard.

Preventive Maintenance

Some of the best policies go beyond just covering major disasters. They also include provisions for preventive maintenance to keep your jewelry in excellent condition. This can cover small but critical repairs like tightening a loose stone, fixing a bent prong, or replacing a worn-out clasp. Think of it as routine healthcare for your jewelry. By addressing these minor issues early, you can prevent a more significant loss, like a diamond falling out of its setting. This feature demonstrates a carrier’s commitment to preservation, not just replacement, and it’s a key indicator of a high-quality policy.

Inflation Protection

The value of precious metals and gemstones can change significantly over time. A piece of jewelry appraised at $15,000 five years ago might be worth much more today. Without the right protection, you could find yourself underinsured when you need to file a claim. That’s why inflation protection is so important. Top-tier policies will automatically adjust your coverage amount periodically, often annually or every two years, to reflect the current market value of your items. This ensures your coverage keeps pace with appreciation, so you’re always protected for the full replacement cost.

Loose Stone Coverage

Your jewelry is especially vulnerable when it’s not fully assembled. Are you having a custom engagement ring designed or resetting a family heirloom? A specialized policy should offer loose stone coverage. This protects a gemstone while it is being set by a jeweler or is otherwise temporarily unmounted. It’s a specific but vital protection that covers a high-risk period that many standard policies overlook. This kind of detailed coverage gives you the freedom to create or modify your pieces without worrying about potential accidents during the process.

Understanding Coverage Limits

Relying on your standard homeowners or renters insurance for your jewelry is one of the biggest mistakes you can make. These policies typically have very low coverage limits for valuables, often capping jewelry protection at just $1,500. They also come with high deductibles and a long list of exclusions that might not cover common scenarios like accidental damage or simple loss. A dedicated personal insurance policy for your jewelry closes these gaps, providing “all-risk” coverage based on each item’s full appraised value. This is the only way to guarantee you can repair or replace your pieces without significant out-of-pocket costs.

Know the Exclusions: What Isn’t Covered

Understanding exclusions is just as important as understanding what is covered:

- Normal wear and tear: Gradual deterioration from daily use is not covered. Regular maintenance helps prevent this.

- Manufacturing defects: Flaws in craftsmanship or materials fall under warranty, not insurance.

- Intentional damage: Any deliberate damage or fraudulent claims are excluded.

- Undocumented items: Jewelry without a valid appraisal or proof of ownership may not be covered.

- Pre-existing damage: Damage that existed before the policy start date is typically excluded.

Damage from Pests

This might sound like an unusual exclusion, but it’s a standard one you should be aware of. If a rodent chews on a jewelry box and damages the items inside, or if insects cause some other unforeseen harm, your policy likely won’t cover the repairs or replacement. Insurers generally view pest-related damage as a preventable home maintenance issue rather than a sudden, accidental event like theft. While it’s certainly a rare scenario, it underscores the importance of proper storage and understanding that insurance is designed to protect against specific perils, not every imaginable circumstance. It’s a good reminder to keep your home secure in every sense of the word.

Damage from Resizing or Cleaning

Taking your jewelry to a professional for resizing, cleaning, or repairs is a key part of responsible ownership. However, if your piece gets damaged during this process, your personal jewelry insurance policy probably won’t cover it. This type of incident usually falls under standard policy exclusions for maintenance or poor workmanship. The responsibility typically lies with the jeweler, who should have their own business liability insurance to cover accidents that happen while an item is in their care. Before leaving your valuable pieces with anyone, it’s always a smart move to ask about their insurance coverage for client property.

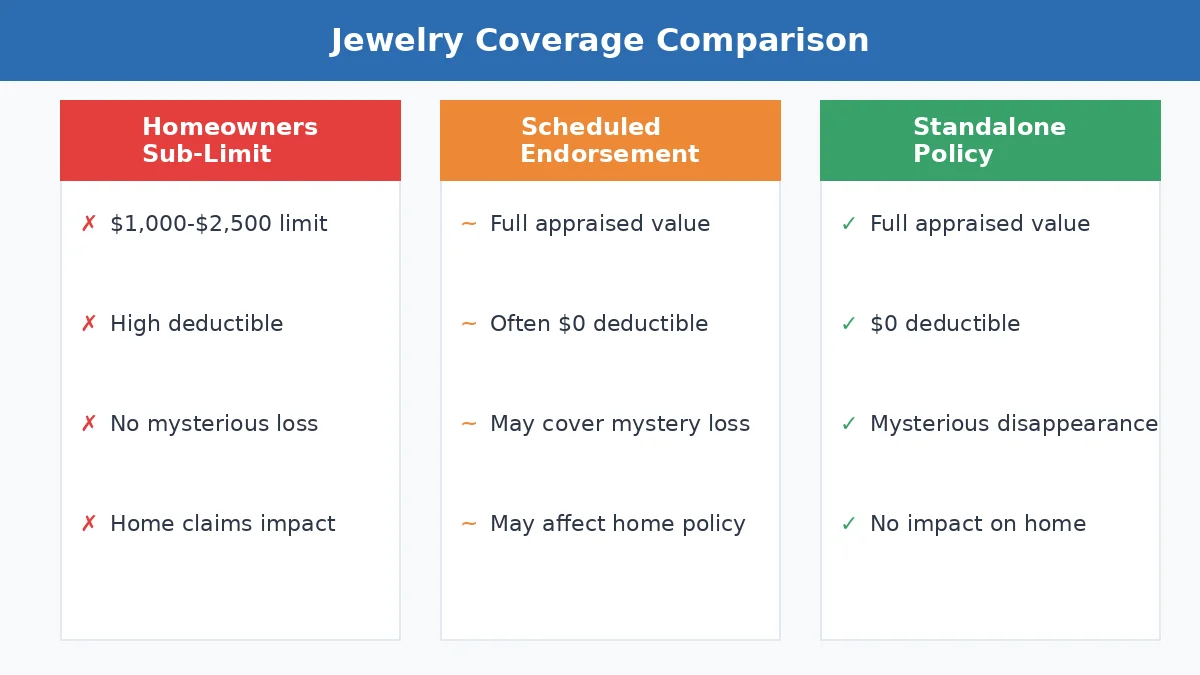

Homeowners vs. Jewelry Insurance: Which Is Better?

One of the most important decisions jewelry owners face is whether to rely on their existing homeowners insurance or to obtain dedicated jewelry coverage. Here is how the three main options compare:

| Feature | Homeowners Sub-Limit | Scheduled Endorsement (Rider) | Standalone Jewelry Policy |

|---|---|---|---|

| Coverage limit | $1,000 to $2,500 typical | Full appraised value per item | Full appraised value per item |

| Deductible | $500 to $2,500 (home deductible) | Often $0 | Often $0 or low ($25 to $100) |

| Mysterious disappearance | Usually not covered | Varies by insurer | Typically included |

| Worldwide coverage | Limited | Usually included | Usually included |

| Impact on home insurance | Claim raises home premium | Claim may raise home premium | No impact on home policy |

| Appraisal required | No | Yes, per item | Yes, per item |

| Cost | Included in home premium | $15-$30 per $1,000/year | $10-$25 per $1,000/year |

| Best for | Low-value costume jewelry | Moderate collections (under 5 items) | High-value or extensive collections |

For most owners of valuable jewelry, a scheduled endorsement or standalone policy is the better choice. The standard homeowners sub-limit leaves a significant coverage gap that could cost thousands of dollars in an uninsured loss.

Top Jewelry Insurance Providers

When you start looking for jewelry insurance, you’ll find two main types of providers: specialty insurers who focus exclusively on valuables, and major carriers who partner with these specialists. Each has its advantages, and the best fit depends on your collection’s value and your existing insurance relationships. Working with an independent broker like Insurance Underwriters can simplify this process, as we can help you compare policies from different providers to secure the right protection at a competitive price. Let’s look at some of the top names in the industry so you know what to expect.

Specialty Insurers

Specialty insurers live and breathe high-value personal property. Unlike general insurance companies that cover everything from cars to houses, these providers focus their expertise on protecting items like jewelry, fine art, and collectibles. This specialization often translates into more comprehensive coverage, a deeper understanding of the appraisal and claims process, and policies tailored specifically to the risks jewelry owners face. They are the experts in the field, offering policies designed from the ground up to protect your most cherished pieces.

Jewelers Mutual

You can’t talk about jewelry insurance without mentioning Jewelers Mutual. They’ve been in this business since 1913, so they have over a century of experience protecting valuable pieces. Their policies are known for being comprehensive, covering common issues like loss, theft, damage, and even mysterious disappearance. One of the standout features is their worldwide coverage, which gives you peace of mind when you travel. They also recognize that jewelry values can increase over time, offering to adjust your coverage every two years to ensure your items remain fully protected against inflation or market changes.

Lavalier

Another key player in the specialty market is Lavalier. They are known for offering “all-risk” coverage, which is a broad type of policy that protects against nearly every potential peril unless it’s specifically excluded. This includes worldwide protection for scenarios like losing your ring on vacation, having it stolen from your gym locker, or accidentally damaging it during daily wear. Lavalier’s coverage is designed to be straightforward, providing a safety net for your valuables against loss, damage, theft, and mysterious disappearance, making them a popular choice for engagement rings and other important pieces.

Chubb

For those with substantial or high-value collections, Chubb is a name that consistently comes up. They are a premier carrier known for catering to high-net-worth clients and offering flexible, robust coverage for jewelry and other valuables. Chubb’s policies are designed to handle complex situations and provide a high level of service, especially during the claims process. They understand the nuances of protecting significant assets and work to ensure your valuable pieces are properly insured against a wide array of risks, from theft to accidental damage, anywhere in the world.

How Major Carriers Provide Coverage

You might be surprised to learn that many of the big-name insurance companies you see advertised everywhere don’t actually underwrite their own jewelry insurance policies. Instead of creating a specialized product from scratch, they partner with the experts—the specialty insurers we just discussed. This is a smart move because it allows them to offer their customers best-in-class coverage through a trusted brand. It’s a win-win: you get the convenience of working with your current insurer while benefiting from the deep expertise of a company that focuses solely on protecting jewelry.

Partnerships with GEICO and Progressive

Two great examples of this partnership model are GEICO and Progressive. GEICO works directly with Jewelers Mutual to offer its customers specialized jewelry protection. This means a GEICO customer can get a policy that covers things a standard homeowners policy won’t, like mysterious disappearance, all backed by Jewelers Mutual’s century of experience. Similarly, Progressive offers jewelry insurance through Lavalier, giving their clients access to comprehensive, all-risk coverage for valuable items like engagement rings and luxury watches. These partnerships make it easier for you to get the right protection without having to start your search from square one.

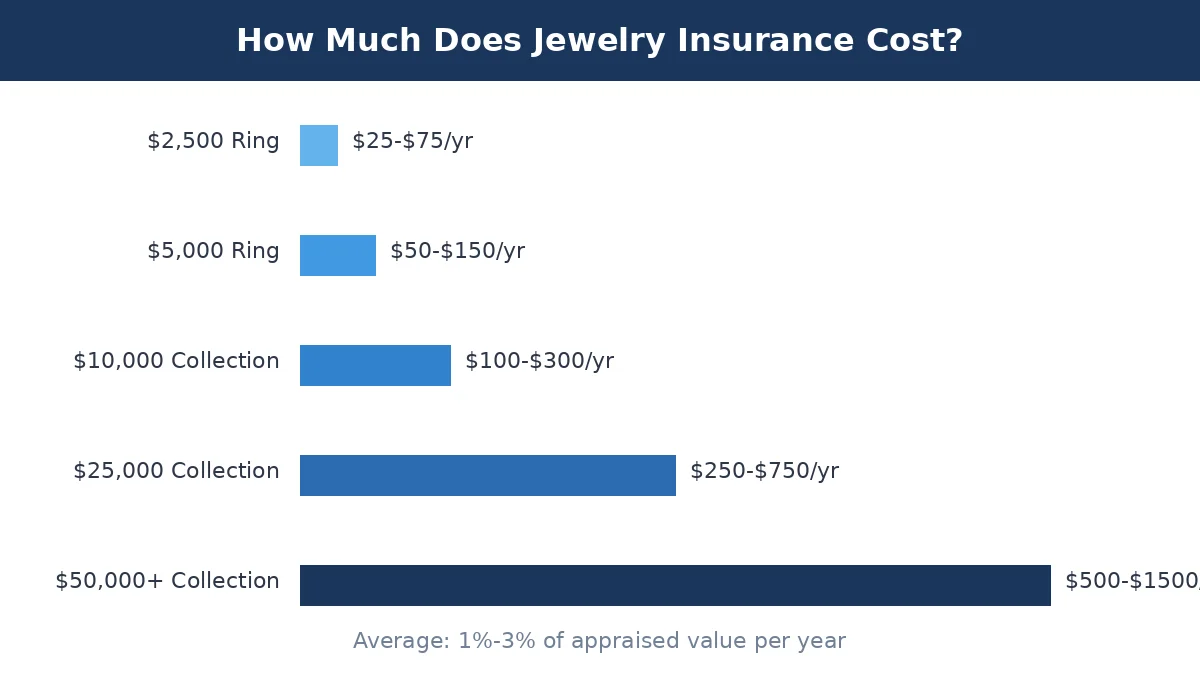

Let’s Talk Numbers: The Cost of Jewelry Insurance

Jewelry insurance is more affordable than most people expect. On average, you can expect to pay between 1% and 3% of the appraised value per year.

Here are some examples of typical annual premiums:

| Appraised Value | Annual Premium Range |

|---|---|

| $2,500 engagement ring | $25 to $75/year |

| $5,000 diamond ring | $50 to $150/year |

| $10,000 collection | $100 to $300/year |

| $25,000 collection | $250 to $750/year |

| $50,000+ high-value collection | $500 to $1,500+/year |

What Determines Your Jewelry Insurance Rate?

Several variables influence how much you will pay for jewelry insurance:

- Appraised value: Higher-value items cost more to insure, though the per-dollar rate may decrease for larger collections.

- Deductible amount: Choosing a higher deductible lowers your premium but increases your out-of-pocket cost when filing a claim.

- Location: Crime rates and natural disaster risk in your area affect pricing. Urban areas and high-crime zip codes typically have higher premiums.

- Security measures: A home security system, safe, or safety deposit box can qualify you for premium discounts.

- Coverage type: Standalone policies from specialty insurers often offer lower per-item rates than homeowners endorsements.

- Claims history: A clean claims record helps keep premiums lower.

Wondering what your jewelry insurance would cost? Request a free jewelry and fine art insurance quote from Insurance Underwriters or call us at 305-900-2823. For comprehensive protection, explore our fine art insurance guide.

Available Discounts on Jewelry Insurance

Beyond choosing the right policy, you can take several proactive steps to lower your annual premium. Insurance companies reward policyholders who actively reduce the risk of loss, theft, or damage. By implementing simple security measures and maintaining proper documentation, you can often secure valuable discounts that make your coverage even more affordable. These savings reflect a partnership between you and your insurer, where your responsible ownership is recognized with lower rates. Let’s look at a few of the most common and effective ways to save on your jewelry insurance.

Home Safes and Alarms

One of the most direct ways to protect your jewelry at home is by investing in security. Insurers look favorably on homeowners who install monitored alarm systems or use a high-quality, bolted-down safe. These measures act as powerful deterrents to theft, significantly lowering the chance you’ll ever need to file a claim. According to the Insurance Information Institute, a good home security system can reduce home insurance premiums, and the same principle applies to jewelry coverage. When you demonstrate that you’re serious about security, insurers are often willing to offer a discount in return for your reduced risk profile.

Bank Vault Storage

For extremely valuable pieces or items you don’t wear often, storing them in a bank vault or safe deposit box is an excellent security strategy. This removes the item from your home, protecting it from burglary, fire, and other household perils. Insurers recognize this as a major reduction in risk and often provide substantial discounts for items kept in a vault. For example, some specialty insurers offer premium reductions of up to 10% or more for vaulted jewelry. This is a smart choice for family heirlooms or investment pieces, ensuring they remain protected while also helping you manage your insurance costs effectively.

Gemstone Grading Reports

While an appraisal determines your jewelry’s monetary value, a gemstone grading report provides the technical proof of its quality and authenticity. Submitting a report from a respected gemological laboratory, such as the Gemological Institute of America (GIA), gives your insurer confidence in what they are covering. This detailed documentation removes ambiguity about the gemstone’s characteristics—like cut, color, clarity, and carat weight—which helps the insurer accurately assess risk and price your policy. This level of transparency can sometimes lead to better rates, as it simplifies the valuation process and provides a clear benchmark for replacement in the event of a claim.

How to Insure Your Engagement Ring: A Simple Guide

Engagement rings are the single most commonly insured piece of jewelry, and for good reason. The average engagement ring in the United States costs between $5,000 and $7,000, making it one of the most valuable items many people own.

Here is a step-by-step process for insuring your engagement ring:

- Get a professional appraisal. Before you can insure your ring, you need a certified appraisal from a GIA-trained gemologist or accredited appraiser. The appraisal documents the ring’s specifications (carat weight, cut, color, clarity, metal type) and assigns a retail replacement value.

- Decide on your coverage type. Choose between adding a scheduled endorsement to your homeowners or renters policy, or purchasing a standalone jewelry policy. For engagement rings worth $5,000 or more, a standalone policy typically offers better coverage and lower deductibles.

- Document your ring. Take high-resolution photographs from multiple angles and store them securely. Keep your purchase receipt, appraisal certificate, and any grading reports (such as GIA or AGS certificates) in a safe location and create digital copies.

- Contact your insurance provider. Submit your appraisal and documentation to obtain a quote. Review the policy details carefully, paying special attention to coverage for mysterious disappearance, worldwide protection, and the claims process.

- Update your appraisal regularly. Precious metal and gemstone prices fluctuate over time. Update your appraisal every two to three years to ensure your coverage reflects current replacement values.

Most insurance professionals recommend insuring your engagement ring within days of purchase. There is no waiting period for most jewelry policies, so coverage can begin immediately.

Have a Collection? Here’s How to Insure It

If you own multiple valuable pieces, insuring them as a collection can simplify your coverage and potentially reduce your per-item costs.

Smart Ways to Insure Your Jewelry Collection

- Inventory every piece. Create a detailed inventory with descriptions, photographs, appraisals, and purchase documentation for each item.

- Schedule high-value items individually. Any piece worth $5,000 or more should be individually listed on your policy with its own appraised value.

- Consider blanket coverage for lower-value items. Some policies allow you to cover multiple lower-value pieces under a single coverage amount rather than scheduling each one.

- Update your inventory annually. Add new purchases and remove items you have sold or gifted. This keeps your coverage accurate and prevents you from paying for pieces you no longer own.

- Store documentation securely. Keep appraisals, receipts, photographs, and your policy documents in a fireproof safe or secure cloud storage.

Collectors with significant holdings should also discuss specialized riders for items in transit, items on loan, or pieces stored in safety deposit boxes.

Getting Your Jewelry Appraised: What to Expect

An appraisal is the foundation of your jewelry insurance coverage. Without a valid, current appraisal, your insurer cannot determine the correct coverage amount and may deny or underpay a claim.

What’s in a Jewelry Appraisal Report?

A professional jewelry appraisal typically documents:

- Item description: Type of piece (ring, necklace, bracelet, watch), metal type and weight, setting style.

- Gemstone details: Carat weight, cut, color, clarity, shape, and any treatments or enhancements.

- Photographs: High-resolution images of the piece from multiple angles.

- Retail replacement value: The estimated cost to replace the item with one of similar quality in the current retail market.

- Appraiser credentials: The appraiser’s qualifications, certifications, and signature.

How Much Does a Jewelry Appraisal Cost?

A typical jewelry appraisal costs between $50 and $250 per item, depending on the complexity of the piece and the appraiser’s credentials. Always choose an appraiser who charges a flat fee or hourly rate rather than a percentage of the item’s value, which creates a conflict of interest.

How Often Should You Update Your Appraisal?

Most insurers recommend updating jewelry appraisals every two to three years. Gold, platinum, and gemstone prices fluctuate based on market conditions, and an outdated appraisal can leave you underinsured or overpaying for coverage you do not need.

Need to File a Claim? Here’s How

If your jewelry is lost, stolen, or damaged, follow these steps to file a claim:

- Report the incident immediately. Contact your insurance provider as soon as possible. For theft, also file a police report.

- Gather your documentation. Prepare your appraisal, photographs, purchase receipts, and any other supporting documents.

- Complete the claim form. Your insurer will provide a claim form. Fill it out with accurate, detailed information about the loss or damage.

- Cooperate with the investigation. Your insurer may investigate the claim, especially for high-value items. Cooperate fully and provide any additional information requested.

- Choose replacement or cash settlement. Depending on your policy, you may receive a cash settlement based on the appraised value or the option to select a replacement piece through the insurer’s network of jewelers.

Most jewelry insurance claims are resolved within two to four weeks. Having complete, up-to-date documentation significantly speeds up the process.

How the Claims Payout Process Works

Direct Payments to Your Jeweler

When you file a claim for a lost, stolen, or damaged piece, the process is designed to be as straightforward as possible. Many specialty jewelry insurance policies allow you to work directly with your preferred jeweler for any repairs or to select a suitable replacement. This gives you control over the quality and style of the final piece, ensuring it meets your standards. Once you approve the work or the new item, the insurance company pays the jeweler directly, minus your deductible. This direct payment system is a huge advantage, as it means you avoid paying a large sum out-of-pocket and waiting for reimbursement. The key to a fast resolution is having your documentation ready. A complete file with your appraisal, receipts, and photos helps substantiate your claim and can get it resolved in just a few weeks.

Simple Ways to Document and Protect Your Jewelry

Taking proactive steps to document and safeguard your jewelry can prevent losses and make the insurance process smoother:

- Photograph every piece. Take detailed photos from multiple angles, including close-ups of engravings, hallmarks, and gemstones.

- Store appraisals digitally. Keep scanned copies of all appraisals, receipts, and certificates in cloud storage so they are accessible even if your home is damaged.

- Use a home safe. A fireproof, waterproof safe provides an extra layer of protection for pieces you are not wearing.

- Remove jewelry during high-risk activities. Take off rings and bracelets during exercise, swimming, gardening, and cleaning to prevent damage or loss.

- Have jewelry inspected regularly. An annual inspection by a jeweler can catch loose prongs, worn settings, and other issues before they lead to a loss.

- Track precious metal and gemstone prices. Staying aware of market trends helps you know when it is time to update your appraisal.

Does Homeowners Insurance Cover Jewelry?

This is one of the most common questions about jewelry protection. The short answer is yes, but with significant limitations.

Standard homeowners insurance (HO-3 policies) typically includes jewelry under personal property coverage. However, most policies impose a sub-limit of $1,000 to $2,500 specifically for jewelry, regardless of your total personal property limit.

This means if you own a $10,000 engagement ring and it is stolen, your homeowners policy would only pay the sub-limit amount, leaving you to cover the remaining thousands of dollars out of pocket.

Additionally, most standard homeowners policies do not cover:

- Mysterious disappearance (losing a piece with no clear explanation)

- Accidental damage (dropping and chipping a stone)

- Individual item replacement at full appraised value

For jewelry worth more than your homeowners sub-limit, dedicated jewelry insurance or a scheduled personal property endorsement is essential.

If you already have homeowners insurance in Florida, ask your agent about adding a jewelry rider or explore a standalone policy for better protection. You can also read our guides on umbrella insurance for additional liability protection and boat insurance in Florida for other personal property coverage needs.

Frequently Asked Questions About Jewelry Insurance

Is jewelry insurance worth it?

For any piece of jewelry worth more than your homeowners sub-limit (typically $1,000 to $2,500), jewelry insurance is absolutely worth the investment. At just 1% to 3% of the appraised value per year, it provides comprehensive protection against loss, theft, damage, and mysterious disappearance. For a $5,000 engagement ring, that works out to roughly $50 to $150 per year for full coverage.

How much does jewelry insurance cost?

Jewelry insurance typically costs 1% to 3% of the appraised value per year. A $5,000 ring costs approximately $50 to $150 annually, while a $10,000 collection costs approximately $100 to $300 per year. Premiums depend on the item’s value, your location, deductible, and security measures.

Does renters insurance cover jewelry?

Renters insurance covers jewelry under personal property, but with the same low sub-limits as homeowners insurance, usually $1,000 to $2,500. For valuable pieces, you need a scheduled endorsement or standalone policy.

Can I insure inherited or antique jewelry?

Yes. You can insure inherited, antique, and vintage jewelry as long as you obtain a current professional appraisal documenting the item’s specifications and replacement value. Antique pieces may require a specialized appraiser familiar with period jewelry.

Agreed Value vs. Replacement Value: What’s the Difference?

Agreed value means you and your insurer agree on a fixed payout amount when you purchase the policy. Replacement value means the insurer pays what it costs to replace the item with a similar piece at current market prices. Replacement value policies adjust with the market but may require updated appraisals.

Do I need a separate policy for each piece of jewelry?

No. Most jewelry insurance policies allow you to schedule multiple items under a single policy. Each piece is listed individually with its own appraised value, but they are all covered under one policy with one premium payment.

Is Jewelry Insurance the Right Choice for You?

Your jewelry represents milestones, memories, and significant financial value. Do not leave it vulnerable to a coverage gap that could cost you thousands.

Insurance Underwriters specializes in jewelry and fine art insurance designed to protect high-net-worth individuals and their most valued possessions. Our team works with you to find the right coverage for your needs, whether you are insuring a single engagement ring or a comprehensive collection.

Get a jewelry insurance quote today or call 305-900-2823 to speak with one of our advisors.

Key Takeaways

- Standard insurance creates a major coverage gap: Your homeowners or renters policy is not enough to protect valuable jewelry, as it typically limits theft or loss coverage to a low amount like $1,500, leaving you financially exposed.

- Choose dedicated coverage for true protection: A standalone jewelry policy or a scheduled endorsement (a rider) is the best way to insure your pieces for their full appraised value. These options cover a wider range of situations, including accidental damage, loss, and mysterious disappearance, often with a zero deductible.

- A professional appraisal is your first step: To get the right coverage, you need a current appraisal that documents your jewelry’s value. This is the foundation of your policy and makes securing comprehensive protection, which typically costs just 1% to 3% of the item’s value per year, a simple process.

Comments

Comments are closed.