Your Complete Guide to Flood Insurance in Florida

Living in Florida means living with the risk of flooding. It’s our most common and costly natural disaster, fueled by everything from hurricanes to heavy summer rains. But here’s a critical fact many homeowners miss: your standard insurance policy offers zero protection against flood damage. This coverage gap leaves your property vulnerable to catastrophic financial loss. Protecting your home requires a separate policy, and we’ll walk you through the essentials of flood insurance Florida so you can find the right coverage.

Protect your Florida property from flood risk. Contact Insurance Underwriters for a personalized flood insurance consultation or call 305-900-2823.

This guide covers everything Florida property owners need to know about flood insurance, whether you own your home or carry landlord insurance on a rental property, from NFIP and private coverage options to flood zone designations, cost factors, coverage details, and strategies to lower your premiums. Whether you own a home in Miami, a condo in Fort Lauderdale, or commercial property anywhere in the Sunshine State, understanding flood insurance is essential for protecting your investment.

Key Takeaways

- Standard homeowners insurance in Florida does not cover flood damage. A separate flood insurance policy is required for protection.

- Flood insurance is mandatory for federally backed mortgages in high-risk flood zones (A and V zones). Citizens Property Insurance now requires all policyholders to carry separate flood coverage.

- NFIP policies cap dwelling coverage at $250,000 and contents at $100,000. Private flood insurance offers higher limits up to $10 million.

- Florida flood insurance costs average $700 to $1,363 per year through NFIP, but premiums range from $400 in low-risk zones to over $12,000 for coastal high-hazard properties.

- FEMA’s Risk Rating 2.0 now prices each property individually based on flood frequency, distance to water, elevation, and rebuilding cost.

- Nearly 25% of all NFIP claims nationally come from properties outside high-risk flood zones.

Is Flood Insurance a Must-Have in Florida?

Florida’s geography makes it uniquely vulnerable to flooding. The state has the longest coastline in the continental United States, low average elevation, a high water table, and sits directly in the path of Atlantic hurricanes. Miami-Dade County alone has more NFIP policies than any other county in the nation.

Many property owners assume their homeowners insurance covers flood damage. It does not. Whether the water comes from a hurricane storm surge, heavy rainfall, overflowing drainage systems, or rising rivers, flood damage requires a separate flood insurance policy.

Why No Part of Florida is Truly Flood-Proof

Flood risk in Florida extends far beyond coastal properties and designated high-risk zones. According to FEMA data, nearly one-third of all NFIP flood insurance claims come from outside high-risk flood areas. Poor drainage, summer thunderstorms, construction runoff, and rising groundwater can cause flooding in any neighborhood.

South Florida faces particular risk due to its limestone bedrock, which allows water to seep upward during heavy rain events, and the region’s low elevation relative to sea level. Miami-Dade and Broward counties experience frequent localized flooding even during routine afternoon thunderstorms.

The Reality of Flood Damage and Federal Aid

Understanding the Financial Risk of Flooding

Let’s get straight to the numbers. Flooding isn’t just an inconvenience; it’s the most expensive natural disaster Florida faces. The average flood claim is over $30,000, and for severe damage, repair costs can easily soar past $100,000. Here’s the critical piece of information every property owner needs to know: your standard homeowners insurance policy will not cover a single dollar of this damage. That’s why a separate flood policy is so essential. And don’t make the mistake of thinking you’re safe just because you’re not in a designated high-risk zone. National data shows that nearly a quarter of all flood insurance claims are filed by property owners in moderate-to-low-risk areas, proving that when it rains, it can flood anywhere.

Why Federal Disaster Aid Isn’t a Safety Net

Another common misconception is that if a major flood hits, federal disaster aid will cover the losses. Unfortunately, this belief can lead to devastating financial consequences. While FEMA assistance is crucial for immediate needs after a disaster, it’s not a substitute for insurance. Federal disaster grants are often limited to between $10,000 and $15,000—a fraction of what’s needed to recover from significant water damage. Even the maximum grant amount rarely exceeds $37,000. Relying on this aid is a gamble you can’t afford to take. True recovery depends on having a robust flood insurance policy designed to restore your property, not just provide a small grant for temporary relief.

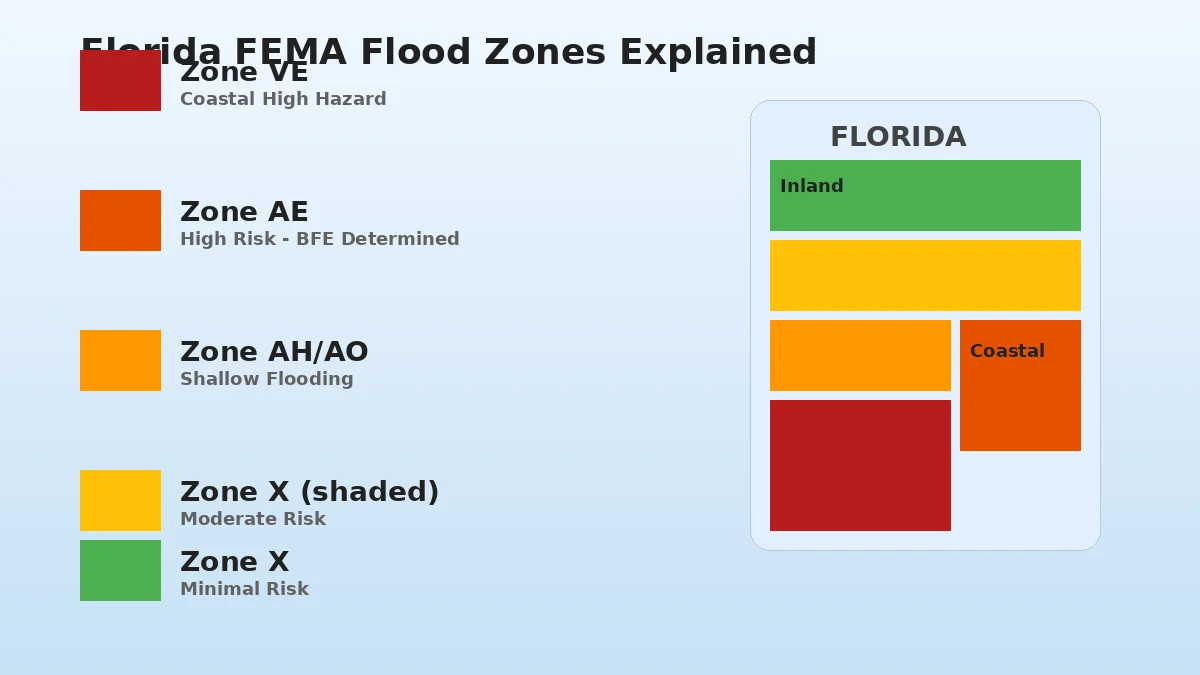

What Are Florida’s Flood Zones?

FEMA designates flood zones across Florida using Flood Insurance Rate Maps (FIRMs). Your property’s flood zone designation is the single biggest factor determining your insurance requirements and premium costs.

Defining High-Risk Flood Zones (SFHAs)

These zones carry a 1% or greater annual chance of flooding (often called the “100-year floodplain”):

- Zone A: Areas subject to flooding from inland rivers and streams. No base flood elevation (BFE) has been determined.

- Zone AE: The most common high-risk designation in Florida. Areas with a 1% annual flood chance where BFE has been established through detailed studies.

- Zone AH: Areas subject to shallow flooding (1 to 3 feet) where ponding occurs, common in flat inland areas.

- Zone AO: Areas subject to shallow sheet flooding (1 to 3 feet), typically along sloped terrain.

- Zone VE: Coastal high-hazard areas subject to storm surge with wave action of 3 feet or more. These zones carry the highest flood insurance premiums in Florida.

Living in a Moderate or Low-Risk Flood Zone

- Zone X (shaded): Moderate risk. Areas between the 100-year and 500-year floodplain. Flood insurance is not required by lenders but is strongly recommended.

- Zone X (unshaded): Minimal risk. Areas outside the 500-year floodplain. Even in these zones, flooding can and does occur.

How to Find Your Property’s Flood Zone

You can look up your property’s flood zone designation using FEMA’s Flood Map Service Center by entering your address. Your mortgage lender, insurance agent, or local floodplain administrator can also help you determine your zone.

NFIP vs. Private Flood Insurance: Which is Right for You?

Florida property owners have two primary options for flood coverage: the National Flood Insurance Program (NFIP) and private flood insurance carriers. Each approach has distinct advantages depending on your property’s value, risk profile, and coverage needs.

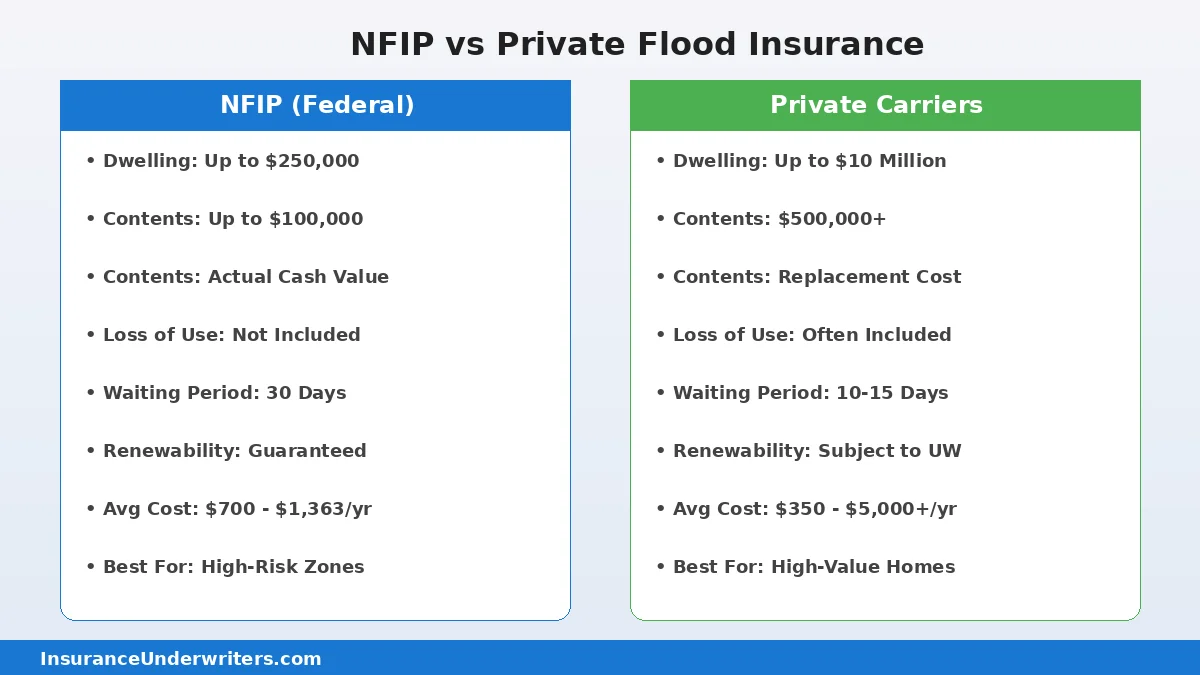

How the NFIP Works for Floridians

The NFIP is a federal program administered by FEMA that provides standardized flood insurance through participating insurance agents (the “Write Your Own” program). Key features include:

- Dwelling coverage: Up to $250,000 for residential properties

- Contents coverage: Up to $100,000

- Pricing: Standardized under Risk Rating 2.0, meaning premiums are the same regardless of which WYO carrier you purchase through

- Availability: Available in virtually all Florida communities (only nine Florida communities do not participate)

- Waiting period: 30 days from purchase before coverage takes effect

- Claims payment: Actual cash value for contents (depreciation applies)

The National Flood Insurance Program at a Glance

Think of the National Flood Insurance Program (NFIP) as the foundational, government-backed option for flood protection. It’s administered by FEMA and provides a standardized safety net for homeowners, renters, and businesses in communities that participate in the program—which includes most of Florida. While it’s a critical resource, it’s important to understand its specific structure and limitations.

Here are the key features you need to know:

- Standardized Coverage Limits: The NFIP offers up to $250,000 in coverage for a residential building and up to $100,000 for its contents. For many Florida properties, especially higher-value homes, this may not be enough to cover a total loss, which is why exploring private options is often necessary.

- Consistent Pricing: Under FEMA’s Risk Rating 2.0 system, the price for an NFIP policy is based on a property’s unique flood risk. This means the premium is consistent, regardless of which insurance company or agent sells you the policy.

- The 30-Day Waiting Period: This is a crucial detail. An NFIP policy typically doesn’t take effect until 30 days after you purchase it. You can’t wait until a storm is approaching to get covered, so planning ahead is non-negotiable.

- Broad Availability: As a federal program, the NFIP is available in nearly every Florida community. This widespread access makes it the go-to starting point for millions of residents seeking essential flood protection.

When to Consider a Private Flood Policy

Private flood insurance now represents approximately 35% of Florida’s flood market, with over 600,000 privately insured properties statewide. Key advantages include:

- Higher coverage limits: Up to $10 million for dwelling coverage

- Replacement cost coverage: Contents paid at replacement cost rather than actual cash value

- Loss of use benefits: Covers temporary living expenses while your home is being repaired (NFIP does not offer this)

- Shorter waiting periods: Some carriers offer 10 to 15-day waiting periods versus NFIP’s 30 days

- Competitive pricing: Private carriers often cost 10% to 30% less than NFIP for properties with favorable risk characteristics

Exploring Private Market Options

The private flood insurance market in Florida offers a variety of specialized products designed to fill the gaps left by the NFIP. These policies often provide more comprehensive protection and greater flexibility, which is especially important for properties with unique features or high replacement values. An independent broker can help you compare these options to find a policy that aligns with your specific risk management strategy. Instead of a one-size-fits-all approach, private carriers allow you to build a coverage plan that truly reflects your property’s value and your financial goals. Here are a few leading private carriers and what sets them apart.

Kin: Integrated Homeowners Coverage

For homeowners looking for simplicity, Kin offers flood coverage that can be added directly to your homeowners policy. This integrated approach streamlines your insurance management into a single policy and payment, which can be a huge time-saver. A major advantage in Florida is that Kin’s flood endorsement has no waiting period, offering immediate protection once the policy is active. It also includes coverage for additional living expenses if a flood forces you from your home, a benefit not offered by the NFIP. This makes it a practical choice for primary residences and seasonal homes alike, providing robust protection without the complexity of managing separate policies.

Neptune: Expanded Coverage for Outdoor Structures

Neptune is a strong choice for property owners with significant outdoor assets that the NFIP typically excludes. Their policies can cover up to $10,000 for pool repair and refilling and up to $50,000 for other detached structures like garages, sheds, or fences, which are often essential parts of a property’s value. Neptune also provides coverage for personal property stored in basements, another critical area where NFIP policies fall short. This makes it an excellent option for properties with extensive landscaping, guest houses, or finished basements, ensuring that more of your total investment is protected from flood damage.

Chubb: Protection for High-Value Homes

For owners of luxury and high-value properties, Chubb provides the high coverage limits necessary to fully protect a significant investment. Specializing in expensive homes, Chubb offers up to $15 million in combined coverage for your home and its contents, far exceeding the NFIP’s caps. Their policies go beyond simple repairs, covering valuable items and even providing up to $5,000 to help you move valuables or install protective measures if a flood warning is issued. This proactive approach to risk mitigation is ideal for clients who need a higher level of service and financial protection for their most valuable assets.

Aon Edge: Competitive Rate Options

Aon Edge often provides a more cost-effective alternative to the NFIP, with rates that can be up to 40% lower for comparable coverage. This doesn’t mean sacrificing protection; their EZ Flood plan offers dwelling limits up to $1.25 million and contents coverage up to $875,000. For properties requiring even higher limits, their Excess Flood plan can provide up to $5 million in combined coverage. This makes Aon Edge a compelling option for property owners focused on optimizing costs without compromising on comprehensive protection, aligning financial efficiency with a strong risk management plan.

Key Differences to Help You Decide

| Factor | NFIP | Private Flood Insurance |

|---|---|---|

| Max dwelling coverage | $250,000 | Up to $10 million |

| Max contents coverage | $100,000 | Varies by carrier (often $500,000+) |

| Contents valuation | Actual cash value | Replacement cost available |

| Loss of use coverage | Not included | Often included |

| Waiting period | 30 days | 10-15 days typical |

| Best for | High-risk zones, properties under $250K value | Properties valued over $250K, favorable-risk homes |

| Renewability | Guaranteed | Subject to carrier underwriting |

Choose NFIP when: Your property is in a high-risk zone (VE, AE), you want guaranteed renewability regardless of claims history, or your home’s replacement cost is under $250,000.

Choose private when: Your home’s replacement cost exceeds $250,000 and NFIP coverage would leave you underinsured, you want loss of use benefits, or your property has favorable risk characteristics that earn lower private rates.

Consider both (NFIP + excess private): For high-value coastal properties, layering NFIP as base coverage with a private excess policy fills the coverage gap above NFIP limits while maintaining federal backing.

Compare your flood insurance options with an independent broker. Get a quote from Insurance Underwriters to review both NFIP and private flood coverage for your property.

How Much Does Flood Insurance Cost in Florida?

Florida flood insurance premiums vary widely based on your property’s flood zone, elevation, construction characteristics, and the coverage option you select.

Average Florida Flood Insurance Costs by Zone

| Flood Zone | NFIP Average Annual Premium | Private Insurance Range |

|---|---|---|

| Zone X (low/moderate risk) | $400 – $1,200 | $350 – $800 |

| Zone AE (high risk) | $1,500 – $5,000 | $1,200 – $5,000 |

| Zone VE (coastal high hazard) | $4,000 – $12,000+ | $3,500 – $15,000+ |

| Zone AO/AH (shallow flooding) | $900 – $2,000 | $700 – $2,200 |

The average Florida homeowner pays between $700 and $1,363 per year for NFIP coverage, which is above the national average of approximately $1,290. However, premiums in Miami-Dade and Broward counties tend to be higher due to extensive coastal exposure.

Understanding NFIP Rate Changes

If you’ve had an NFIP policy for a while, you’ve likely seen your premium shift. This isn’t arbitrary; it’s the result of FEMA’s updated pricing approach, known as Risk Rating 2.0. In the past, your rate was determined almost exclusively by your property’s location on a flood map. The new system moves away from these broad zones to price each property individually, creating a more precise and equitable premium. This change aims to align your insurance costs more closely with your specific, real-world flood risk.

Instead of relying solely on a map, FEMA now incorporates a wider range of data points. This includes your home’s specific elevation, its distance from potential flooding sources like the ocean or a river, the frequency of different flood types in your area, and the estimated cost to rebuild. The goal is to ensure rates accurately reflect a property’s unique risk profile. For some Florida homeowners, this has led to an increase in cost, while others have seen their premiums go down. Understanding these variables is the first step toward managing your flood insurance costs effectively.

Key Factors That Affect Your Flood Insurance Premium

Under FEMA’s Risk Rating 2.0, premiums are now calculated individually for each property rather than using simple zone-based pricing. The key factors include:

- Flood frequency at your specific location: How often your property is expected to experience flooding

- Flood type: River overflow, rainfall, coastal surge, or storm surge

- Distance to the nearest water source: Properties closer to the coast, rivers, or canals pay more

- Property elevation: Homes above the Base Flood Elevation (BFE) receive lower rates

- Cost to rebuild: Higher replacement cost means higher premiums

- Building characteristics: Foundation type, number of floors, year built, and flood-resistant features

How to Lower Your Flood Insurance Costs

- Get an elevation certificate: If your property sits above the BFE, an elevation certificate can document this and reduce your premium

- Install flood vents: Properly designed openings in foundation walls allow floodwater to flow through rather than push against the structure

- Elevate mechanical systems: Raising HVAC, water heaters, and electrical panels above BFE reduces risk and premiums

- Choose a higher deductible: Increasing your deductible from $1,000 to $5,000 or $10,000 lowers annual premiums

- Take advantage of Community Rating System (CRS) discounts: If your community participates in FEMA’s CRS program, residents may receive a 5% to 45% premium discount

- Compare NFIP and private options: Private carriers may offer 10% to 30% savings for properties with favorable risk profiles

What Does Flood Insurance Cover in Florida?

Understanding exactly what flood insurance covers (and does not cover) helps you avoid surprises when filing a claim.

What Building Coverage Includes

Flood insurance covers physical damage to the insured building, including:

- Foundation walls, staircases, and structural elements

- Electrical and plumbing systems

- HVAC equipment, water heaters, and furnaces

- Permanently installed flooring (carpet, tile, hardwood)

- Built-in cabinets, countertops, and bookcases

- Built-in appliances (dishwashers, ranges, refrigerators)

- Detached garage (up to 10% of building coverage under NFIP)

- Debris removal costs

What Contents Coverage Includes

Contents coverage protects your belongings inside the insured building:

- Furniture and electronics

- Clothing and personal items

- Portable appliances (washers, dryers, microwaves)

- Curtains, area rugs, and window treatments

- Food freezers and their contents

What’s Not Covered by a Standard Flood Policy?

Standard flood insurance policies (both NFIP and most private) exclude:

- Vehicles: Cars, boats, and other vehicles require separate coverage. Consider watercraft insurance or auto insurance with comprehensive coverage.

- Finished basement improvements: NFIP provides limited basement coverage (primarily for essential equipment)

- Landscaping, pools, and fences: Outdoor structures and landscaping are generally excluded

- Temporary living expenses: NFIP does not cover loss of use (private policies may include this)

- Currency, precious metals, and valuable papers: Specialized jewelry and fine art coverage may be needed

- Business interruption losses: Businesses should explore commercial property insurance options

When Is Flood Insurance Required in Florida?

When Your Mortgage Lender Requires Flood Insurance

If you have a federally backed mortgage (FHA, VA, USDA, or conventional loans purchased by Fannie Mae or Freddie Mac) and your property is in a Special Flood Hazard Area (zones A or V), your lender is required by federal law to mandate flood insurance. You must maintain coverage for the life of the loan.

What Happens if Your Required Policy Lapses?

If your lender requires you to carry flood insurance, letting the policy lapse can lead to a costly problem. Your mortgage servicer will likely purchase “force-placed insurance” on your behalf to protect their financial interest in the property. This type of policy is significantly more expensive—often two to three times the cost of a standard policy—and offers much less protection. Force-placed coverage is designed to protect the lender’s investment, not your personal belongings or your equity in the home. To avoid this expensive and inadequate coverage, it’s critical to maintain continuous flood insurance throughout the life of your loan.

Flood Insurance After Your Mortgage is Paid Off

Once you’ve paid off your mortgage, federal law no longer requires you to maintain a flood insurance policy, even if you live in a high-risk zone. However, your property’s flood risk doesn’t disappear with your final mortgage payment. Florida’s weather patterns and low elevation mean that flooding remains a constant threat. Dropping your coverage to save on premiums exposes your most valuable asset to catastrophic financial loss. Continuing to maintain a flood policy is a strategic decision to protect your home’s equity and ensure you can rebuild without draining your savings or taking on new debt after a disaster.

Florida’s Flood Disclosure Law for Home Sellers

If you’re planning to sell your property, you need to be aware of Florida’s flood disclosure requirements. State law mandates that home sellers must inform potential buyers about the property’s flood history. This includes disclosing whether you have ever filed a flood insurance claim on the property or if the property has ever received federal disaster assistance for flood damage. This transparency is designed to help buyers make an informed decision about their potential risk and insurance needs. Failing to disclose this information can lead to legal complications after the sale is complete.

How Citizens Property Insurance Affects You

Florida’s Citizens Property Insurance Corporation, the state’s insurer of last resort, began requiring separate flood insurance for all policyholders through a phased implementation:

- Properties with replacement cost over $600,000 were required first

- The mandate is expanding to cover all Citizens policyholders regardless of flood zone by 2027

- If you carry Citizens insurance, you may already be required to have flood coverage even if you are not in a high-risk zone

Why You Still Need Coverage in Low-Risk Zones

Florida homeowners outside high-risk flood zones should still strongly consider flood insurance. Just one inch of floodwater can cause more than $25,000 in damage to a home. With Preferred Risk Policies available through NFIP for as little as $400 to $600 per year in lower-risk zones, the cost of coverage is modest compared to potential losses.

How to File a Flood Insurance Claim in Florida

If your property sustains flood damage, acting quickly and documenting everything improves your chances of a successful claim.

What to Do Immediately After a Flood

- Contact your insurance carrier immediately. Report the flood damage to your NFIP carrier or private insurer as soon as it is safe to do so. Most policies require prompt notification.

- Document all damage thoroughly. Take photos and videos of every affected room, item, and structural element before cleaning up or making repairs. This evidence is critical for your claim.

- Separate damaged from undamaged property. Do not discard damaged items until the adjuster has inspected them. Place damaged belongings in a separate area.

- Make temporary repairs to prevent further damage. Cover broken windows, tarp damaged roofs, and remove standing water. Keep receipts for all emergency repair expenses.

- Meet with the adjuster. NFIP sends an adjuster to inspect your property, usually within 30 days. For private policies, timing varies by carrier. Be present during the inspection to point out all damage.

- Review and negotiate the settlement. Compare the adjuster’s estimate against your documentation. If you disagree with the assessment, request a re-inspection or file an appeal.

Key Deadlines to Remember

- NFIP proof of loss deadline: 60 days from the date of the adjuster’s report

- Florida statute of limitations: Claims must generally be filed within 3 years, but earlier is always better

- Document everything: Keep copies of all correspondence, receipts, and claim-related documents

Protecting Your Florida Business from Floods

Businesses in Florida face the same flood risks as homeowners, and standard commercial property insurance typically excludes flood damage. Commercial flood insurance is available through both NFIP and private carriers.

NFIP Options for Business Owners

- Building coverage up to $500,000

- Contents coverage up to $500,000

- Same 30-day waiting period applies

When to Choose Private Commercial Coverage

Private carriers often provide better options for Florida businesses:

- Higher coverage limits for valuable commercial properties

- Business interruption coverage (not available through NFIP)

- Faster claims processing and more flexible policy terms

- Coverage for loss of income during restoration

Construction companies should also consider builders risk insurance to protect projects during the building phase, and all businesses should review their general liability coverage to ensure comprehensive protection.

Need flood coverage for your business? Insurance Underwriters works with both NFIP and private carriers to find the right commercial flood solution. Get a business property insurance quote or call 305-900-2823.

Special Considerations for Miami and South Florida

As a Miami-based brokerage, Insurance Underwriters understands the unique flood challenges South Florida property owners face.

What Makes Miami-Dade Unique?

- Miami-Dade has the highest concentration of NFIP policies in the country

- The county’s low elevation (averaging just 6 feet above sea level) puts most properties at some level of flood risk

- King tides and sea-level rise are increasing the frequency of nuisance flooding even in moderate-risk zones

- Many Miami neighborhoods in Zone AE face annual premiums of $1,500 to $5,000 under Risk Rating 2.0

Do I Need Flood Insurance for My Condo?

Flood insurance for condominiums works differently. Your condo association should carry a building flood policy (Residential Condominium Building Association Policy under NFIP), while individual unit owners need a separate contents policy to cover personal belongings and interior improvements. Review your association’s master policy to understand what is and is not covered at the building level.

Get Your Flood Policy Ready for Hurricane Season

Florida’s hurricane season runs from June 1 through November 30. Remember:

- NFIP policies have a 30-day waiting period, so purchase coverage before storm threats develop

- You cannot purchase or modify flood insurance once a tropical storm or hurricane is named

- Review your policy annually before hurricane season to confirm adequate limits

Looking for coverage beyond your home? Learn about travel insurance to protect your vacation investments and health while traveling.

Renters in Florida also need flood coverage, but the policy structure is different from homeowners. See our renters insurance Florida guide for details on how tenants can protect their belongings from flood damage.

Frequently Asked Questions

How much is flood insurance in Florida?

The average annual cost ranges from $700 to $1,363 through NFIP, depending on your flood zone, property elevation, and building characteristics. Low-risk zone properties may pay as little as $400 per year, while coastal high-hazard properties in Zone VE can exceed $12,000 annually. Private flood insurance may offer 10% to 30% savings for properties with favorable risk profiles.

Is flood insurance required in Florida?

Flood insurance is required for properties in Special Flood Hazard Areas (zones A and V) with federally backed mortgages. Citizens Property Insurance policyholders face expanding flood insurance mandates regardless of zone. Even when not legally required, flood insurance is strongly recommended for all Florida properties given the state’s flood risk.

Which Florida flood zones require insurance?

Federal law requires flood insurance for mortgaged properties in high-risk zones: A, AE, AH, AO, V, and VE. Lenders for properties in moderate-risk Zone X (shaded) may also require coverage at their discretion. All flood zones are eligible for voluntary coverage.

Does homeowners insurance cover flooding in Florida?

No. Standard homeowners insurance policies in Florida explicitly exclude flood damage. A separate flood insurance policy through NFIP or a private carrier is required for flood protection. This applies regardless of whether the flooding is caused by hurricanes, heavy rain, storm surge, or rising water.

What is the difference between NFIP and private flood insurance?

NFIP is a federal program with standardized terms, $250,000 dwelling limits, and guaranteed renewability. Private flood insurance offers higher coverage limits (up to $10 million), replacement cost contents valuation, loss of use coverage, potentially shorter waiting periods, and often lower premiums for favorable-risk properties. NFIP is backed by the federal government, while private policies are backed by the issuing insurance company.

Can I get flood insurance if I am not in a high-risk zone?

Yes. NFIP flood insurance is available to any property owner in a participating community, regardless of flood zone. In fact, NFIP Preferred Risk Policies for low-to-moderate risk zones are among the most affordable flood coverage options available, often costing $400 to $600 per year.

Tools and Resources for Florida Property Owners

Online Tools to Assess Your Risk

Before you can secure the right coverage, you need a clear picture of your property’s specific flood risk. The best place to start is with the federal government’s own data. FEMA provides a free, user-friendly resource called the Flood Map Service Center. By simply entering your address, you can see your property’s official flood zone designation, which is the primary factor insurers use to determine your premium. This information empowers you to understand whether you’re in a high-risk coastal zone like VE or a more moderate-risk area like Zone X. If you find the maps confusing, don’t worry. Your mortgage lender or a knowledgeable insurance agent can also pull this information for you and explain exactly what it means for your personal insurance needs.

How to Get a Flood Insurance Quote

Once you know your flood zone, the next step is to explore your coverage options. A great starting point is the NFIP’s official website, floodsmart.gov, which has a tool to generate a preliminary quote. However, this only shows you one piece of the puzzle. To get a complete view, it’s essential to compare prices from both the federal program and private insurance companies, as private carriers can often provide higher limits and more competitive rates. Remember, since nearly a quarter of all flood claims occur in low-to-moderate risk zones, it’s wise to consider coverage no matter your designation. Working with an independent broker like Insurance Underwriters allows you to review quotes from the NFIP and multiple private insurers side-by-side, ensuring you find the best fit for your property and budget.

Comments

Comments are closed.