Restaurant Insurance Guide

Running a restaurant without proper insurance is one of the fastest ways to lose everything you have built. Between kitchen fires, customer injuries, employee claims, and foodborne illness lawsuits, restaurants face more concentrated risk than nearly any other small business. Restaurant insurance is the collection of commercial policies that protect your food business from these financial threats, covering everything from slip-and-fall accidents to liquor liability and spoiled inventory. Learn more about event insurance coverage. Learn more about liquor liability insurance.

Need restaurant insurance? Contact Insurance Underwriters or call 305-900-2823 to speak with a commercial risk advisor who specializes in hospitality coverage.

Restaurant insurance is not a single policy. It is a package of coverages tailored to the specific risks your restaurant faces based on its size, location, cuisine type, alcohol service, delivery operations, and number of employees. This guide covers every type of coverage you need, what each policy protects, how much restaurant insurance costs, and how to build a comprehensive protection strategy for your food business.

Key Takeaways

- Restaurant insurance typically costs between $3,000 and $10,000 per year, depending on your restaurant’s size, revenue, location, and risk profile.

- Every restaurant needs at minimum general liability insurance, commercial property insurance, and workers’ compensation insurance.

- Restaurants that serve alcohol must carry liquor liability insurance, which covers claims arising from intoxicated patrons.

- A business owners policy (BOP) bundles general liability, property, and business interruption coverage at a discounted rate.

- Food contamination coverage protects against losses from foodborne illness outbreaks and spoiled inventory.

- Florida restaurants face specific requirements, including mandatory workers’ compensation for businesses with four or more employees.

- Insurance Underwriters helps restaurant owners across the United States build customized coverage packages that address every layer of hospitality risk.

What Is Restaurant Insurance?

Restaurant insurance is a collection of commercial policies that protect food service businesses from financial losses caused by lawsuits, property damage, employee injuries, food safety incidents, and operational disruptions. Insurance Underwriters provides customized restaurant insurance packages covering general liability, commercial property, workers’ compensation, liquor liability, food contamination, business interruption, commercial auto, and cyber liability for restaurants across the United States.

The restaurant industry operates in one of the highest-risk environments for commercial insurance. The National Restaurant Association reports that there are over 1 million restaurant locations in the United States, and the industry generates over $1 trillion in annual sales. With that scale comes enormous exposure: hot kitchens, heavy foot traffic, alcohol service, perishable inventory, delivery operations, and large workforces all create overlapping liability scenarios.

Restaurant insurance transfers these financial risks from your business to an insurance carrier. Instead of paying $150,000 out of pocket for a customer injury lawsuit, your general liability policy covers the legal defense and settlement. Instead of absorbing the full cost of a kitchen fire, your commercial property insurance pays to rebuild and replace equipment. Instead of shutting down permanently after a food contamination incident, your coverage pays for remediation, legal defense, and lost income during the closure.

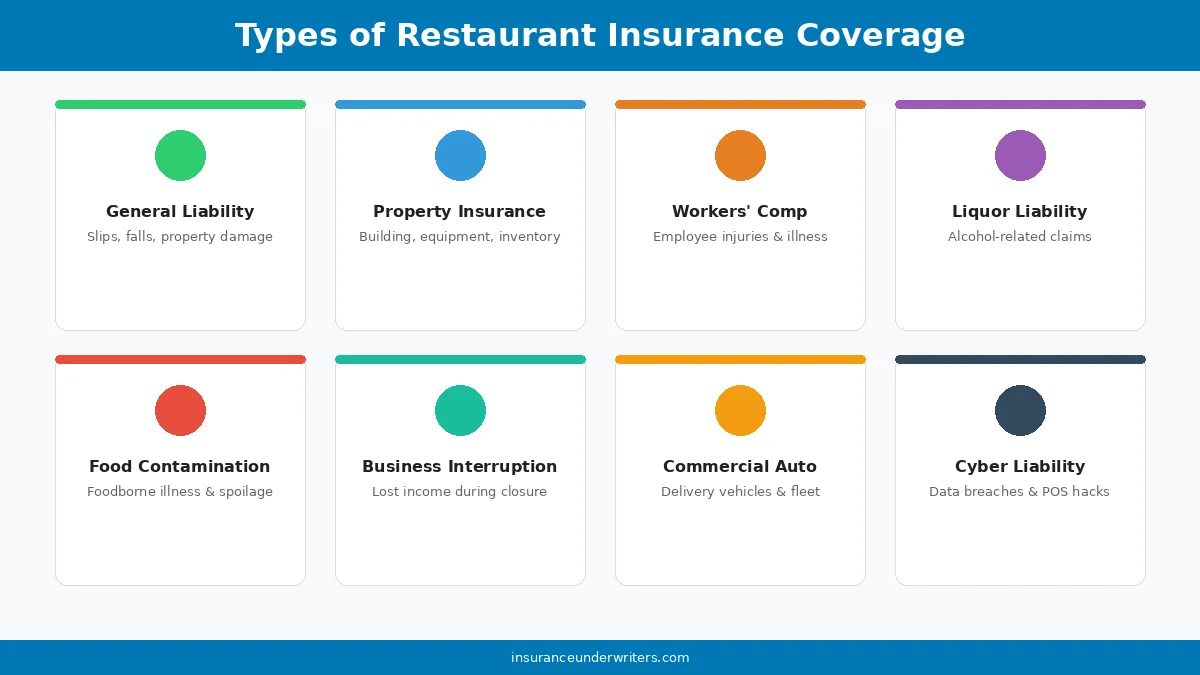

What Types of Insurance Does a Restaurant Need?

Every restaurant faces a unique combination of risks based on its format, location, and operations. The coverage types below represent the essential policies that most restaurant owners need. Your specific situation determines the exact combination and coverage limits.

General Liability Insurance

General liability insurance is the foundation of every restaurant insurance program. It covers third-party bodily injury, property damage, and advertising injury claims. When a customer slips on a wet floor, burns themselves on a hot plate, or trips over a loose carpet edge, general liability pays the medical bills, legal defense costs, and any settlements or judgments.

Standard policies provide $1 million per occurrence and $2 million in aggregate coverage. For restaurants, general liability typically costs between $2,000 and $5,000 per year, higher than many other small businesses because of the elevated foot traffic and injury risk inherent in food service environments.

Every restaurant needs general liability coverage regardless of size. Landlords require it before signing a lease. Event venues require it before allowing catering. Vendors and suppliers often require proof of coverage before entering contracts.

Commercial Property Insurance

Commercial property insurance protects your restaurant’s physical assets: the building (if you own it), kitchen equipment, furniture, fixtures, signage, point-of-sale systems, inventory, and any other business personal property. It covers losses from fire, storms, theft, vandalism, electrical failure, and other covered perils.

Restaurant property coverage is critical because of the high replacement cost of commercial kitchen equipment. A single commercial oven can cost $10,000 to $50,000. Walk-in coolers, ventilation systems, dishwashing stations, and specialty cooking equipment add up quickly. A total kitchen fire loss at a mid-sized restaurant can easily exceed $500,000.

Coverage limits should match the full replacement cost of your total physical assets. Annual premiums typically range from $2,000 to $6,000 depending on property value, building construction, fire suppression systems, and location.

Workers’ Compensation Insurance

Workers’ compensation insurance covers medical expenses, rehabilitation costs, and a portion of lost wages when an employee suffers a work-related injury or illness. Restaurant workers face elevated injury risks from cuts, burns, slips, repetitive strain, and heavy lifting.

Workers’ compensation is legally required in nearly every state once you have employees. In Florida, businesses with four or more employees must carry workers’ comp coverage. The restaurant industry has one of the highest workers’ compensation claim rates of any sector, which means premiums tend to run higher, typically $3,000 to $8,000 per year for a restaurant with 15 to 30 employees.

Beyond legal compliance, workers’ compensation protects your business from employee injury lawsuits. Without coverage, a single serious burn or fall injury could result in a six-figure lawsuit that threatens your restaurant’s survival.

Liquor Liability Insurance

If your restaurant serves beer, wine, or spirits, liquor liability insurance is essential. This coverage protects against claims arising from the actions of intoxicated patrons, including drunk driving accidents, fights, property damage, and injuries caused by customers who were overserved.

Liquor liability is separate from general liability because alcohol-related claims carry significantly higher legal exposure. A drunk driving fatality linked to overservice at your restaurant could result in a multi-million dollar lawsuit. Standard general liability policies exclude or severely limit alcohol-related claims.

Premiums depend heavily on the percentage of your revenue that comes from alcohol sales. A restaurant where alcohol represents 15% of revenue will pay significantly less than a bar or nightclub where alcohol is 60% or more of revenue. Expect to pay $1,000 to $5,000 per year for restaurant-level liquor liability coverage.

Food Contamination and Spoilage Coverage

Food contamination coverage, sometimes called food spoilage insurance, protects your restaurant from losses related to foodborne illness outbreaks, contaminated ingredients, and spoiled inventory. This includes the cost of disposing contaminated food, deep cleaning the facility, legal defense against customer illness claims, and lost revenue during a health department closure.

A single norovirus outbreak can force a restaurant to close for days or weeks while the source is identified and the facility is sanitized. The direct costs of disposal, cleaning, and lost perishable inventory are compounded by the reputational damage and lost revenue. Food contamination coverage addresses all of these losses.

This coverage also protects against equipment breakdown scenarios, such as a walk-in cooler failure that spoils $20,000 worth of inventory overnight. Some policies bundle equipment breakdown coverage with food spoilage, while others offer them separately.

Business Interruption Insurance

Business interruption insurance replaces lost income and covers ongoing fixed expenses when a covered event forces your restaurant to close temporarily. If a fire, flood, or major equipment failure shuts down your kitchen for three months, business interruption coverage pays your rent, loan payments, payroll for key employees, and the income your restaurant would have earned during the closure period.

Looking for a business interruption quote for your restaurant? Get a free coverage analysis from Insurance Underwriters today.

This coverage is typically included in a business owners policy (BOP) but can also be purchased as a standalone policy. The coverage limit should reflect your restaurant’s monthly fixed expenses and average revenue. Most restaurants need at least 6 to 12 months of business interruption coverage to survive a major loss event.

Business Owners Policy (BOP)

A business owners policy bundles general liability, commercial property, and business interruption coverage into a single, discounted package. For many restaurant owners, a BOP provides the broadest foundation of coverage at the lowest cost.

BOPs typically cost between $2,000 and $5,000 per year for restaurants, which is significantly less than purchasing each component separately. The bundled approach also simplifies administration since you deal with one policy, one premium, and one renewal date instead of three.

Most restaurants with fewer than 100 employees and less than $5 million in annual revenue qualify for a BOP. Larger or higher-risk operations may need to purchase standalone policies for each coverage type.

Commercial Auto Insurance

If your restaurant operates delivery vehicles, catering vans, or company cars, commercial auto insurance is required. This covers vehicle damage, driver injuries, and third-party liability from accidents involving your business vehicles.

With the growth of in-house delivery services, more restaurants need commercial auto coverage than ever before. Even if your drivers use personal vehicles for deliveries, you may need hired and non-owned auto coverage to protect your restaurant from liability if a delivery driver causes an accident while working.

Cyber Liability Insurance

Cyber liability insurance protects your restaurant from data breaches, ransomware attacks, and other cybersecurity incidents. Restaurants process thousands of credit card transactions daily through POS systems, making them frequent targets for hackers.

A data breach that exposes customer payment information can trigger costly notification requirements, credit monitoring obligations, regulatory fines, and lawsuits. Cyber liability coverage pays for forensic investigation, customer notification, legal defense, and regulatory compliance costs. Premiums for restaurants typically range from $500 to $2,000 per year.

Employment Practices Liability Insurance (EPLI)

Employment practices liability insurance protects your restaurant from employee claims of discrimination, harassment, wrongful termination, and wage violations. The restaurant industry has one of the highest rates of employment-related lawsuits, driven by high employee turnover, tip disputes, and workplace harassment claims.

A single wrongful termination lawsuit can cost $75,000 to $200,000 in legal defense and settlement costs, even if the claim is ultimately dismissed. EPLI coverage is increasingly important as employment law becomes more complex and employee awareness of their rights increases.

How Much Does Restaurant Insurance Cost?

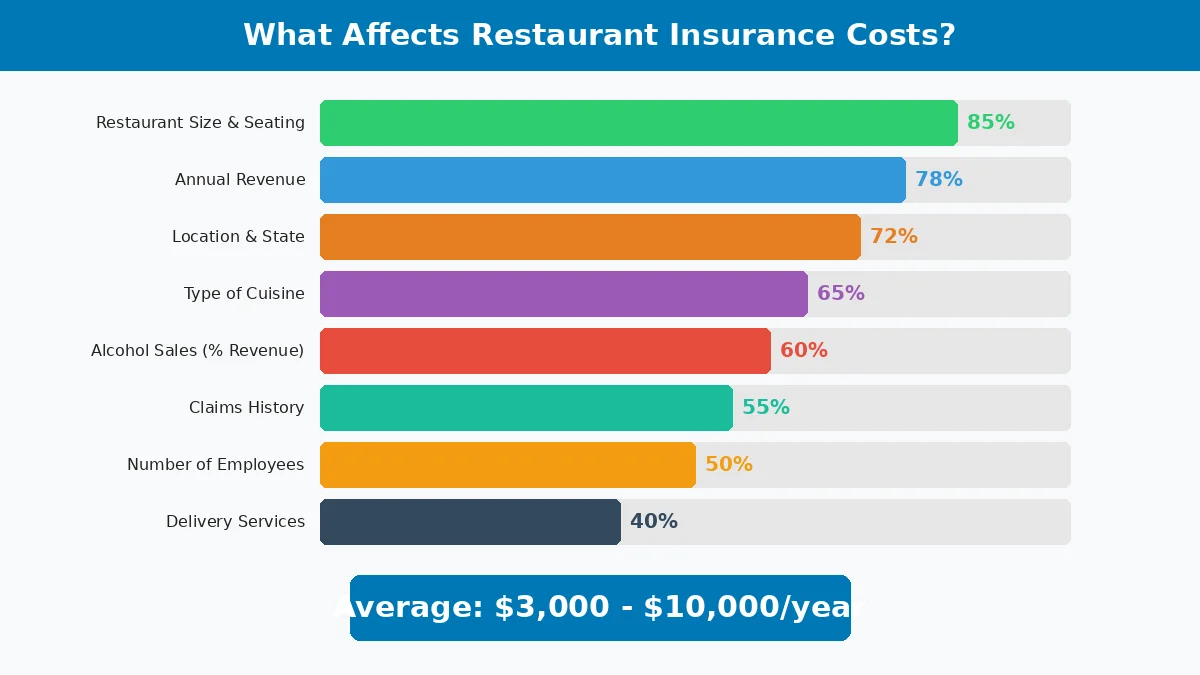

Restaurant insurance typically costs between $3,000 and $10,000 per year for a comprehensive coverage package. Insurance Underwriters helps restaurant owners determine the right coverage levels based on their restaurant’s size, revenue, location, cuisine type, alcohol sales volume, claims history, number of employees, and delivery operations to build a cost-effective protection strategy.

Here is a breakdown of typical annual costs by coverage type:

| Coverage Type | Average Annual Cost |

|---|---|

| General Liability | $2,000 – $5,000 |

| Commercial Property | $2,000 – $6,000 |

| Workers’ Compensation | $3,000 – $8,000 |

| Liquor Liability | $1,000 – $5,000 |

| Food Contamination | $500 – $2,000 |

| Business Interruption | $750 – $2,500 |

| Commercial Auto | $1,200 – $4,000 |

| Cyber Liability | $500 – $2,000 |

| EPLI | $800 – $3,000 |

| BOP (GL + Property + BI bundle) | $2,000 – $5,000 |

Factors That Affect Your Premium

Restaurant size and seating capacity. A 30-seat cafe pays less than a 200-seat banquet hall. More seats mean more foot traffic, higher revenue exposure, and greater injury risk.

Annual revenue. Insurance carriers use revenue as a proxy for overall risk exposure. Higher revenue generally means higher premiums, but it also means you have more to protect.

Location. Restaurants in high-crime areas, flood zones, or regions with high litigation rates pay more. Florida restaurants face hurricane and flood exposure that increases property premiums.

Type of cuisine. Restaurants with extensive frying, open-flame cooking, or wood-fired ovens carry higher fire risk and may pay more for property coverage.

Alcohol sales as a percentage of revenue. Higher alcohol revenue increases liquor liability premiums significantly.

Claims history. A clean claims record earns better rates. Restaurants with multiple prior claims face higher premiums or may struggle to find coverage.

Number of employees. More employees mean higher workers’ compensation premiums and greater EPLI exposure.

Delivery operations. Restaurants with in-house delivery services need commercial auto coverage and face higher general liability exposure from off-premises incidents.

Ready to find out what restaurant insurance will cost for your business? Contact Insurance Underwriters at 305-900-2823 for a free, no-obligation coverage analysis.

How to Get Restaurant Insurance

Getting the right restaurant insurance package requires more than just calling the cheapest provider. The process should be thorough and tailored to your specific operation.

Step 1: Assess your risks. Identify every risk your restaurant faces: kitchen fire, customer injury, employee claims, alcohol liability, food contamination, delivery accidents, and data breaches.

Step 2: Determine required coverages. Some coverages are legally required (workers’ comp in most states), while others are contractually required (general liability for most leases).

Step 3: Work with a commercial insurance broker. An independent broker like Insurance Underwriters can shop multiple carriers to find the best combination of coverage, price, and claims service.

Step 4: Bundle where possible. A BOP saves money compared to purchasing general liability, property, and business interruption separately.

Step 5: Review and update annually. Your insurance needs change as your restaurant grows. New menu items, expanded delivery, additional locations, or increased alcohol sales all require coverage adjustments.

Florida Restaurant Insurance Considerations

Florida presents unique insurance challenges for restaurant owners. Hurricane exposure increases commercial property premiums significantly. Flood insurance is often necessary even for restaurants outside designated flood zones, since Florida experiences more flooding events than any other state.

Florida requires workers’ compensation insurance for businesses with four or more employees in most industries, including restaurants. The state also has specific regulations around liquor liability that restaurant owners must understand, particularly regarding overservice liability and dram shop laws.

Standard commercial property policies exclude flood damage, so a separate flood policy is essential for Florida restaurants, especially those in coastal areas like Miami, Fort Lauderdale, Tampa, and Jacksonville.

Insurance Underwriters, headquartered in Miami at 3050 Biscayne Blvd Suite 700, specializes in Florida commercial coverage and understands the state’s unique insurance landscape for restaurant owners.

Frequently Asked Questions About Restaurant Insurance

How much does restaurant insurance cost?

Restaurant insurance typically costs between $3,000 and $10,000 per year for a comprehensive package. The exact cost depends on your restaurant’s size, revenue, location, type of cuisine, alcohol sales, number of employees, and claims history. A small cafe with no alcohol service and 5 employees might pay $3,000 per year, while a large full-service restaurant with a bar, 40 employees, and delivery service could pay $10,000 or more.

What kind of insurance does a restaurant need?

Every restaurant needs at minimum general liability insurance, commercial property insurance, and workers’ compensation insurance. Restaurants that serve alcohol need liquor liability insurance. Additional important coverages include food contamination, business interruption, commercial auto (for delivery), cyber liability, and EPLI. A business owners policy (BOP) is an efficient way to bundle the core coverages.

What does restaurant insurance cover?

Restaurant insurance covers a wide range of risks including customer injuries (slips, burns, allergic reactions), property damage (fire, storms, theft, vandalism), employee work injuries, alcohol-related liability, foodborne illness claims, business income loss during closures, delivery vehicle accidents, data breaches, and employment-related lawsuits.

Do restaurants need liquor liability insurance?

Yes, any restaurant that serves beer, wine, or spirits should carry liquor liability insurance. This coverage protects against claims arising from intoxicated patrons, including drunk driving accidents, fights, and property damage. Standard general liability policies exclude or severely limit alcohol-related claims, making separate liquor liability essential.

How much is liability insurance for a restaurant?

General liability insurance for restaurants typically costs $2,000 to $5,000 per year for standard $1M/$2M coverage limits. If you add liquor liability, expect an additional $1,000 to $5,000 per year depending on your alcohol revenue. Total liability costs (general + liquor + EPLI) for a full-service restaurant with a bar commonly range from $4,000 to $12,000 annually.

What is the best restaurant insurance?

The best restaurant insurance is a customized package built by an experienced commercial broker who understands hospitality risk. There is no single best carrier. The right choice depends on your restaurant’s specific profile. Working with an independent broker like Insurance Underwriters gives you access to multiple carriers and ensures your coverage package is tailored to your exact needs.

Comments

Comments are closed.