Commercial Auto Insurance: Coverage, Cost & Savings

What’s one of the biggest threats to your business? It might not be what you think. A single car accident involving a work vehicle can spark lawsuits that put your company’s assets on the line. Here’s the critical part: your personal auto policy offers zero protection in these situations. This is where a solid commercial auto insurance policy becomes your financial firewall. It’s not just another line item on your budget; it’s a strategic move to protect everything you’ve built from catastrophic liability.

Get a commercial auto insurance quote from Insurance Underwriters or call 305-900-2823 to speak with a specialist today.

This guide breaks down what commercial auto insurance covers, which businesses need it, how much it costs in 2026, and how to structure a policy that protects your operations without overpaying.

Key Takeaways

- Commercial auto insurance covers vehicles used for business purposes, including company-owned vehicles, leased trucks, employee-driven cars, and hired or rented vehicles.

- Personal auto policies exclude business use, meaning any claim arising from work-related driving can be denied entirely.

- Small businesses typically pay $1,200 to $3,500 per vehicle per year, though costs vary by industry, vehicle type, driving records, and coverage limits.

- Commercial auto liability insurance is legally required in nearly every state, with minimum limits varying from $15,000 to $50,000 per person for bodily injury.

- Businesses without company vehicles still need hired and non-owned auto (HNOA) coverage if employees ever drive for work purposes.

What Is Commercial Auto Insurance?

Commercial auto insurance is a business insurance policy that provides financial protection for vehicles used in company operations. It covers liability for bodily injury and property damage caused to third parties, physical damage to your own vehicles, medical expenses for drivers and passengers, and additional risks specific to business vehicle use.

The critical distinction between personal and commercial auto insurance comes down to how the vehicle is used, not what type of vehicle it is. A pickup truck that hauls materials to a job site is a commercial vehicle. A sedan that carries an employee to client meetings is being used commercially. The moment a vehicle is used for business operations, personal auto insurance no longer applies.

Commercial auto insurance fills this gap with higher liability limits, coverage for multiple drivers, and protections tailored to the risks businesses face on the road every day.

What Does Commercial Auto Insurance Cover?

A commercial auto policy combines several coverage types into one package. Understanding each component helps you build the right level of protection for your specific operations.

Covering Liability and Legal Costs

Commercial auto liability insurance is the foundation of every policy and the coverage required by law in nearly every state. It includes two components:

- Bodily injury liability pays for medical expenses, lost wages, pain and suffering, and legal defense costs when your driver causes injury to another person.

- Property damage liability covers the cost to repair or replace other people’s property damaged in an accident, including vehicles, buildings, fences, and equipment.

Most states require minimum liability limits, but those minimums are often insufficient for real-world claims. Common commercial liability limits are $1 million combined single limit (CSL) or split limits such as $250,000/$500,000/$100,000. Many contracts, particularly in construction and transportation, require $1 million CSL or higher before you can start work.

How Much Liability Coverage Do You Really Need?

While state-mandated minimums might keep you legally compliant, they offer a false sense of security. A single serious accident can easily result in medical and legal costs that soar past a $50,000 or $100,000 limit, leaving your business assets exposed to cover the difference. For this reason, a $1 million Combined Single Limit (CSL) is the standard recommendation for most businesses and a non-negotiable requirement for many client contracts. The right amount of liability coverage isn’t just about meeting a legal minimum; it’s about creating a financial firewall that protects your company from a catastrophic lawsuit. A thorough risk assessment with an experienced broker can help you determine if a $1 million limit is sufficient or if your operations warrant a higher limit through a commercial umbrella policy.

Repairing or Replacing Your Business Vehicles

Physical damage coverage protects your own vehicles and comes in two forms:

- Collision coverage pays for damage to your vehicle from a collision with another vehicle or object, regardless of who is at fault.

- Comprehensive coverage handles damage from non-collision events, including theft, vandalism, fire, hail, flooding, falling objects, and animal strikes.

Physical damage coverage is optional from a legal standpoint, but lenders and leasing companies require it on financed or leased vehicles. For businesses that depend on their vehicles to generate revenue, this coverage is essential for avoiding costly out-of-pocket repairs or replacement.

Covering Medical Bills After an Accident

Medical payments coverage pays for medical expenses incurred by your driver and passengers after an accident, regardless of who was at fault. In no-fault states, personal injury protection (PIP) replaces medical payments coverage and provides broader benefits, including coverage for lost wages and rehabilitation.

This coverage is particularly important for businesses whose employees regularly ride in company vehicles or transport clients.

Protection from Uninsured Drivers

This coverage protects your business when the at-fault driver either has no insurance (uninsured) or does not carry enough insurance (underinsured) to cover the damages. Many states require this coverage for commercial vehicles, including trucking insurance for long-haul operations,.

Considering that roughly one in eight drivers on U.S. roads is uninsured, this protection closes a significant gap in your risk management strategy.

Insuring Rented or Employee-Owned Vehicles

Hired and non-owned auto (HNOA) coverage is one of the most overlooked and most important components of a commercial auto program. It provides liability protection in two scenarios:

- Hired auto covers vehicles your business rents or leases on a short-term basis.

- Non-owned auto covers employees driving their personal vehicles for business purposes, such as running errands, visiting clients, or making deliveries.

Even businesses that do not own a single vehicle need HNOA coverage if employees ever drive for work. The liability exposure from an employee-caused accident while performing work duties falls on the employer, and a personal auto policy may not cover the claim.

What Isn’t Covered? (Common Exclusions)

Knowing what your commercial auto policy doesn’t cover is just as important as knowing what it does. Every policy contains exclusions, which are specific situations or types of damage that the insurance company will not pay for. These aren’t hidden traps; they are standard contract terms that define the boundaries of your coverage. Understanding these limitations ahead of time allows you to close potential gaps with operational policies or additional coverage, ensuring your business isn’t left exposed after an incident.

Vehicle and Equipment Nuances

Some of the most common claim denials come from how vehicles are used and who is driving them. For instance, if an employee uses a company van for personal errands over the weekend and gets into an accident, the claim could be denied because personal use is typically excluded. Similarly, if a driver who isn’t officially listed on your policy causes a crash, your insurer may refuse to cover the damages. It’s also critical to remember that insurance is designed for accidents, not intentional acts. Damage resulting from a road rage incident or any other deliberate action won’t be covered.

Specialized Services and Endorsements

Standard commercial auto policies are built for common risks, but they don’t cover every business scenario. If your work requires you to sign contracts where you assume liability for others, you’ll likely need a specific endorsement for contractual liability. Policies also typically exclude catastrophic events like floods, earthquakes, and acts of war, which require separate coverage. Finally, any claim related to illegal activities will be denied. If a vehicle is damaged while being used for street racing or any other criminal purpose, your insurance will not pay for the repairs or liability.

Who Needs Commercial Auto Insurance?

The short answer: any business whose operations involve driving. The longer answer covers more scenarios than most business owners realize.

When Is Commercial Auto Insurance a Must?

- Companies that own or lease vehicles used for deliveries, service calls, transportation, or daily operations

- Contractors and construction firms that transport tools, materials, and crews to job sites

- Delivery and courier services operating vans, trucks, or cars for package and food delivery

- Sales organizations with representatives who drive to client meetings and appointments

- Healthcare and home service providers including mobile veterinarians, home health aides, HVAC technicians, plumbers, and electricians

- Transportation companies including taxi services, limousines, medical transport, and shuttle services

- Real estate professionals who drive clients to property showings

- Landscaping, cleaning, and maintenance companies that transport equipment between job sites

Why You Might Need Coverage (Even Without Company Cars)

If your employees ever use personal vehicles for any business purpose beyond commuting, your business is exposed to liability. Examples include:

- An employee drives their own car to a client meeting and causes an accident on the way

- A manager uses their personal vehicle to pick up office supplies

- A salesperson drives between appointments throughout the day

In all of these situations, the business can be held liable. A hired and non-owned auto policy addresses this exposure.

Not sure if you need commercial auto insurance? Our team at Insurance Underwriters can evaluate your specific operations and recommend the right coverage. Request a free coverage review or call 305-900-2823.

How Much Does Commercial Auto Insurance Cost?

Commercial auto insurance costs vary significantly based on your industry, vehicle types, driver records, location, and coverage limits. Here are realistic 2026 cost ranges:

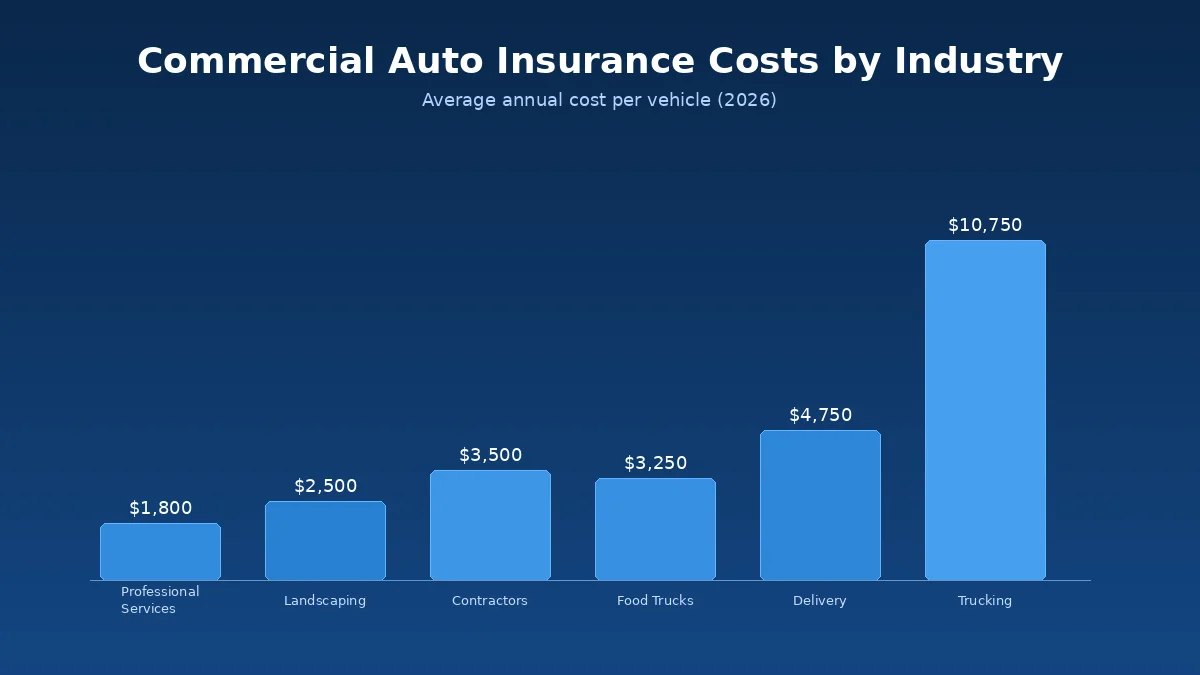

A Look at Average Premiums by Industry

| Business Type | Estimated Annual Cost Per Vehicle |

|---|---|

| Professional services (sedans, light use) | $1,200 – $2,400 |

| General contractors | $2,800 – $4,200 |

| Delivery and courier services | $3,500 – $6,000 |

| Food trucks and catering | $2,500 – $4,000 |

| Landscaping and lawn care | $1,800 – $3,200 |

| For-hire trucking (per truck) | $9,000 – $12,500 |

Most small businesses with light commercial vehicles pay between $1,200 and $3,500 per vehicle per year, which translates to roughly $100 to $290 per month per vehicle.

Examples of Monthly Costs

To give you a clearer picture of how these annual premiums translate into a monthly budget item, let’s look at some industry-specific examples. A professional services firm using sedans for client visits might budget around $100 to $200 per vehicle per month. In contrast, a general contractor with trucks hauling tools and materials often sees costs between $233 and $350 per month. Businesses with vehicles constantly on the road, like delivery and courier services, can expect to pay anywhere from $292 to $500 per month.

Other common examples include landscaping companies, whose work trucks typically range from $150 to $267 per month, and for-hire trucking operations, where the high mileage and risk can push the monthly cost for a single truck to between $750 and $1,042. These figures highlight how much your specific operations influence your rate. The only way to determine your exact cost is by requesting a tailored quote that accounts for your unique business details.

What Factors Influence Your Insurance Rate?

Vehicle type and use. A sedan used for occasional client visits costs far less to insure than a heavy-duty truck making daily deliveries. Heavier vehicles, specialized equipment, and high-mileage use all increase premiums.

Driver records. Insurers evaluate the motor vehicle records (MVRs) of every driver on the policy. Accidents, traffic violations, DUIs, and license suspensions all increase costs. Clean driving records across your team can significantly reduce premiums.

Coverage limits and deductibles. Higher liability limits and lower deductibles increase premiums. However, carrying adequate limits ($1 million CSL is standard for most commercial operations) prevents catastrophic out-of-pocket exposure.

Number of vehicles. Multi-vehicle policies often qualify for fleet discounts, typically ranging from 5% to 25% for businesses with five or more vehicles.

Location. Urban areas with heavy traffic, higher accident rates, and more expensive medical care produce higher premiums than rural locations. Your garaging ZIP code is a major pricing factor.

Claims history. A clean loss history over the past three to five years earns better rates. Conversely, frequent claims signal higher risk and drive premiums up.

Industry classification. Certain industries carry higher inherent risk. Contractors, delivery services, and transportation companies pay more than professional services firms or real estate agencies.

Annual mileage and radius. The more miles driven and the wider the operating territory, the higher the exposure and the higher the premium.

Commercial vs. Personal Auto Insurance: What’s the Difference?

Understanding the differences between commercial and personal auto insurance helps business owners recognize why a personal policy is never adequate for business use.

| Feature | Personal Auto Insurance | Commercial Auto Insurance |

|---|---|---|

| Who is covered | Named individual and household members | Business entity and authorized employees |

| Liability limits | Typically $100,000 – $300,000 | $500,000 – $2,000,000+ |

| Vehicle ownership | Individual | Individual, business, or leased to business |

| Multiple drivers | Household members only | Any authorized employee |

| Business use | Excluded or severely limited | Covered by design |

| Hired/rented vehicles | Typically excluded | Covered with HNOA endorsement |

| Cost | Lower | Higher (reflects increased risk) |

The most dangerous assumption a business owner can make is that their personal auto policy will cover a work-related accident. Personal insurers routinely deny claims involving business use, leaving the business fully exposed to lawsuits, medical bills, and property damage.

Does Commercial Auto Insurance Cover Personal Use?

In most cases, yes. Commercial auto policies generally cover personal use of a company-owned vehicle by an authorized driver. However, the specifics depend on your policy terms. Some policies restrict personal use coverage or apply different deductibles. Always confirm with your insurance advisor how personal use is handled on your commercial policy.

Beyond Your Vehicle: Related Insurance Policies to Consider

Commercial auto insurance is a critical piece of your risk management puzzle, but it doesn’t cover everything. A vehicle accident can trigger other liabilities, and your business assets extend far beyond your fleet. To create a truly resilient operation, you need to look at how your auto policy fits within a broader insurance strategy. Several other coverages work alongside commercial auto to protect your business from different angles, ensuring one incident doesn’t jeopardize your financial stability. Thinking about these policies now helps you build a comprehensive shield against the unexpected.

Coverage for Tools and Equipment

Your commercial auto policy is designed to cover the vehicle itself, but what about the valuable cargo inside? If you’re a contractor, landscaper, or any professional who transports gear, your tools and equipment are your livelihood. A standard auto policy won’t pay to replace them if they are stolen from a truck or damaged in a collision. That’s where inland marine insurance, often called tools and equipment coverage, comes in. This specialized policy protects your essential machinery and equipment from theft, damage, and other unforeseen risks, whether they are on a job site, in transit, or in storage. It’s a must-have for any business that relies on portable equipment to get the job done.

Commercial Umbrella Insurance

What happens when a catastrophic accident results in a lawsuit that exceeds the limits of your commercial auto policy? A single major claim can easily surpass a standard $1 million limit, leaving your business responsible for the rest. A commercial umbrella insurance policy provides an essential extra layer of liability protection. It sits on top of your primary policies—like general liability and commercial auto—and kicks in when those limits are exhausted. For businesses facing significant public interaction or high-risk operations, umbrella insurance isn’t a luxury; it’s a strategic defense against a worst-case scenario that could otherwise be financially devastating.

Business Owner’s Policy (BOP)

For many small and mid-sized businesses, a Business Owner’s Policy (BOP) is an efficient and cost-effective way to secure foundational coverage. A BOP bundles two essential policies—general liability and commercial property insurance—into a single package, often at a lower price than buying them separately. General liability protects against third-party claims of injury or property damage, while property insurance covers your physical assets like your office or warehouse. While a BOP doesn’t include commercial auto insurance, it serves as the core of a business’s risk management program, which can then be supplemented with auto, workers’ comp, and other necessary policies.

Garage Keepers Insurance

If your business operates an auto repair shop, body shop, dealership service department, or any facility that takes custody of customer vehicles, you need a separate policy to protect those vehicles while they are in your care. Commercial auto insurance covers your own fleet, but it does not cover damage to a customer’s car sitting in your bay or parked in your lot. Garage keepers insurance fills that gap by covering customer vehicles against fire, theft, vandalism, and collision while they are in your possession.

Workers’ Compensation

If an employee is injured in a work-related auto accident, your commercial auto policy will cover vehicle damage and third-party liability, but it won’t cover your employee’s medical bills or lost wages. That’s the job of workers’ compensation insurance. This coverage is legally required in almost every state and is crucial for protecting both your employees and your business. It provides medical benefits and wage replacement for employees injured on the job, while also shielding your business from potentially crippling lawsuits related to the injury. For any company with employees on the road, workers’ comp is a non-negotiable part of your insurance portfolio.

Smart Ways to Save on Commercial Auto Insurance

Premiums are not fixed. Businesses that take a proactive approach to risk management can meaningfully reduce their commercial auto insurance costs.

1. Create a Driver Safety Program

Establishing formal driver training, regular MVR checks, and clear vehicle use policies demonstrates to insurers that you actively manage your risk. Some carriers offer premium discounts of 5% to 15% for documented safety programs.

Leverage Insurer-Provided Safety Resources

You don’t have to create a safety program from scratch. Many insurance carriers offer a library of resources to help their clients manage risk, including online driver training courses, vehicle maintenance checklists, and templates for building official safety policies. Using these tools does more than just make your job easier; it shows your insurer that you’re a proactive partner in preventing accidents. This kind of partnership is exactly what underwriters look for. A strong safety record, built with the help of your insurer’s own risk management tools, often leads to better coverage options and more favorable premiums down the road.

2. Use Safety and Tracking Technology

GPS tracking, dash cameras, electronic logging devices (ELDs), and collision avoidance systems give underwriters quantifiable proof that your fleet operates safely. Telematics data showing safe driving habits can unlock meaningful premium reductions.

3. Choose a Higher Deductible

Raising your physical damage deductible from $500 to $1,000 or $2,500 reduces premiums. This strategy works best for businesses with strong cash reserves that can absorb smaller losses without filing a claim.

4. Bundle Your Insurance Policies

Working with a single brokerage that handles your commercial auto, general liability, workers’ compensation, and property insurance often qualifies your business for package discounts. Bundling also simplifies administration and ensures consistent coverage.

5. Prioritize Clean Driving Records

Enforce strict hiring standards for drivers. Run MVR checks during hiring and at least annually thereafter. Remove high-risk drivers from the policy when possible. Every preventable accident that stays off your record improves renewal pricing.

6. Review Your Coverage Annually

Business operations change. Vehicles are added or retired. Routes change. An annual policy review with your insurance advisor ensures your coverage matches your current operations and that you are not paying for coverage you no longer need.

7. Pay Your Premium in Full

While monthly payments can be helpful for cash flow, they often come with small installment fees that add up over the year. One of the simplest ways to reduce your total insurance cost is to pay your annual premium in a single lump sum. Many insurance carriers offer a discount, often between 5% and 10%, for customers who pay in full. This strategy eliminates administrative fees and provides a direct, measurable return on your insurance spending. If you can comfortably manage your cash flow to accommodate the one-time payment, it’s a straightforward tactic for trimming operational expenses without sacrificing an ounce of protection.

8. Maintain Continuous Coverage

Letting your commercial auto insurance lapse, even for a single day, creates a significant financial vulnerability for your business. Any accident that occurs during a coverage gap becomes your full responsibility, exposing your company to potentially devastating out-of-pocket costs. Furthermore, insurers view lapses as a major red flag, signaling instability and higher risk. When you go to reinstate your policy or find a new one, you’ll likely face much higher premiums. Maintaining continuous coverage is not just about legal compliance to avoid having to face fines; it’s a critical part of maintaining a favorable risk profile and ensuring long-term cost control.

9. Report Claims Promptly

When an accident happens, time is of the essence. Reporting a claim immediately allows your insurance carrier to begin its investigation while the details are fresh and evidence is available. A delay can compromise the ability to gather accurate witness statements and assess the situation, which can complicate the process and potentially lead to a more expensive outcome. Prompt reporting demonstrates that you are a proactive partner in managing risk. It enables your insurer to control costs, defend your business effectively, and resolve the claim more efficiently, which helps protect your claims history and keep your future premiums stable. When in doubt, it’s always best to work with your advisor to report any incident that could lead to a claim.

How to Get Your Commercial Auto Insurance Policy

Securing the right commercial auto coverage follows a straightforward process:

- Assess your vehicle inventory. List every vehicle used for business, including employee-owned vehicles used for work purposes.

- Identify your coverage needs. Determine required liability limits based on state law, contract requirements, and your risk tolerance.

- Gather driver information. Compile driver names, license numbers, and driving history for everyone who will operate business vehicles.

- Document your operations. Be prepared to describe your business type, vehicle use, annual mileage, operating radius, and cargo insurance details.

- Work with a commercial insurance advisor. An experienced brokerage like Insurance Underwriters can compare quotes across multiple carriers, identify coverage gaps, and structure a policy that balances protection with cost efficiency.

- Review policy details before binding. Confirm liability limits, deductibles, covered vehicles, named drivers, and any exclusions.

Working With an Insurance Professional

While you can get a quote directly from a carrier, partnering with an experienced insurance advisor transforms the process from a simple transaction into a strategic business decision. A true professional does more than just find a policy; they analyze your specific operational risks, from your vehicle fleet and driver profiles to your contractual obligations. They act as your risk architect, ensuring your coverage is not only compliant but also cost-effective and aligned with your long-term goals. An independent brokerage provides access to multiple insurance carriers, allowing them to find the optimal balance of price and protection that a single insurer cannot offer. This partnership ensures you have an advocate who understands your business and can provide guidance on everything from claims handling to annual policy reviews, securing comprehensive business protection that supports your growth.

Does Your State Require Commercial Auto Insurance?

Almost every state requires businesses to carry minimum liability insurance for commercial vehicles. Requirements vary, but common minimum limits include:

- Bodily injury: $25,000 per person / $50,000 per accident (many states)

- Property damage: $15,000 to $25,000 per accident

- Combined single limit (CSL): Some states allow a single limit covering both bodily injury and property damage

Federal requirements through the Federal Motor Carrier Safety Administration (FMCSA) apply to interstate carriers:

- General freight carriers: $750,000 minimum

- Household goods carriers: $750,000 minimum

- Passenger carriers (16+ passengers): $5,000,000 minimum

- Hazardous materials haulers: $1,000,000 to $5,000,000 depending on cargo

State minimums are just that: minimums. They rarely provide adequate protection for a real-world claim. A serious accident with injuries can easily exceed $100,000 in medical costs alone. Working with an experienced commercial insurance advisor helps ensure your limits reflect your actual exposure.

Penalties for Driving Uninsured

Failing to carry state-mandated commercial auto insurance leads to consequences that go far beyond a simple ticket. The financial penalties alone can be severe, with fines ranging from a few hundred dollars to over $5,000, depending on the state and whether it’s a repeat offense. Authorities can also suspend your driver’s license and vehicle registration and even impound your vehicle, immediately halting business operations. In some states, driving uninsured can even result in jail time. Because these penalties vary so widely, it’s critical to understand that a lapse in coverage creates a significant legal and financial liability for your company.

Beyond the immediate fines, getting caught without insurance often triggers a long-term administrative headache. Most states will require you to file an SR-22, which is a certificate of financial responsibility that your insurance company submits to the DMV. This document proves you are carrying at least the state-minimum liability coverage. An SR-22 requirement flags you as a high-risk driver to insurers, which almost always leads to significantly higher premiums for several years. This single compliance issue can inflate your insurance costs and impact your business’s bottom line long after the initial fine is paid.

Understanding Your Rights: Policy Cancellation and Non-Renewal

The consequences of driving uninsured extend directly to your relationship with your insurance carrier. If you are cited for a coverage lapse, your insurer may cancel your policy mid-term or choose not to renew it at the end of the term. This action leaves your business without protection and creates a critical gap in your risk management. A history of driving without insurance makes it much more difficult and expensive to secure new coverage, as future insurers will view your business as a higher risk. This negative mark on your record can follow you for years, limiting your options and increasing your operational costs.

While an insurer has the right to terminate a policy for valid reasons like non-payment or a coverage lapse, they cannot do so without following proper procedures. State regulations dictate how and when an insurer can cancel or non-renew a policy, including providing adequate written notice. It’s helpful to understand your rights as a policyholder in these situations. However, the most effective strategy is always prevention. Maintaining continuous, adequate coverage is the only way to ensure your business is protected from liability and to preserve your long-term insurability and access to competitive rates.

Finding the Right Commercial Auto Coverage for Your Business

Commercial auto insurance is not a luxury for businesses with large fleets. It is a foundational risk management tool for any business whose employees ever get behind the wheel for work. From a single sedan making sales calls to a fleet of delivery trucks operating across state lines, the right coverage prevents a single accident from becoming a financial catastrophe.

The key is working with an advisor who understands your operations, evaluates your specific risk profile, and builds a policy that protects your business without unnecessary costs.

Insurance Underwriters specializes in commercial auto insurance for businesses of all sizes. Whether you need coverage for a single vehicle or a full fleet program, our team evaluates your operations, compares options across top-rated carriers, and structures a policy that fits your risk profile and budget.

Get a commercial auto insurance quote or call us at 305-900-2823 to speak with a commercial auto specialist.

Frequently Asked Questions

How much is commercial auto insurance?

Most small businesses pay between $1,200 and $3,500 per vehicle per year for commercial auto insurance. Monthly costs range from approximately $100 to $290 per vehicle. The exact cost depends on your industry, vehicle type, driving records, coverage limits, location, and claims history. Contractors and delivery services typically pay more than professional services firms due to higher inherent risk.

What is commercial auto insurance?

Commercial auto insurance is a business insurance policy that covers vehicles used for work purposes. It provides liability protection for bodily injury and property damage caused to others, physical damage coverage for your own vehicles, medical payments for drivers and passengers, and additional protections like uninsured motorist and hired/non-owned auto coverage. Personal auto policies exclude business use, making commercial coverage essential for any business that uses vehicles.

Do I need commercial auto insurance?

You need commercial auto insurance if your business owns or leases vehicles, if employees drive for work purposes (even in their personal cars), if you transport goods or equipment, or if you provide any kind of transportation service. Even businesses without company-owned vehicles should carry hired and non-owned auto coverage to protect against liability when employees drive for business. Nearly every state requires minimum commercial auto liability coverage for business vehicles.

What does commercial auto insurance cover?

Commercial auto insurance covers liability for bodily injury and property damage you cause to others, collision damage to your own vehicles, comprehensive damage from theft, fire, weather, and vandalism, medical payments for your driver and passengers, and uninsured/underinsured motorist protection. Additional coverage options include hired and non-owned auto, cargo coverage, and roadside assistance. Specific coverage depends on the endorsements and limits you select.

How much is commercial auto insurance per month?

Monthly commercial auto insurance costs typically range from $100 to $290 per vehicle for small businesses with standard commercial vehicles. Higher-risk operations such as delivery services may pay $290 to $500 per vehicle per month, while for-hire trucking operations can pay $750 to $2,500 or more per truck per month. Your actual cost depends on vehicle type, usage, driving records, and coverage limits.

Does commercial auto insurance cover personal use?

Most commercial auto policies do cover personal use of company-owned vehicles by authorized employees. However, coverage terms and deductibles may differ for personal use compared to business use. Some policies include restrictions on personal use. Review your policy language with your insurance advisor to understand exactly how personal driving is handled under your commercial auto coverage.

Is commercial auto insurance more expensive than personal auto insurance?

Yes, commercial auto insurance typically costs more than personal auto insurance because it covers higher liability limits, multiple drivers, heavier or specialized vehicles, and higher-risk business activities. The premium difference reflects the increased exposure that comes with business vehicle use, including more miles driven, more drivers on the policy, and higher potential claim values. However, the cost is a fraction of what an uninsured business accident can produce in liability.

Comments

Comments are closed.