Condo Insurance 101: A Guide for Smart Owners

Think your HOA fees have your insurance needs completely covered? That’s a common—and potentially costly—misconception for Florida condo owners. Your association’s master policy protects the building and common areas, but what about everything inside your unit? From your personal belongings to liability for an accident, you could be on your own. This is where personal condo insurance, or an HO-6 policy, becomes so important. It’s designed to fill those critical gaps. If you own a condo in Miami, South Florida, or anywhere in the Sunshine State, call Insurance Underwriters at 305-900-2823 or request a home insurance quote to get the right HO-6 coverage for your unit today.

Whether you just purchased your first condo in Brickell, own a unit in South Beach, or are considering a place in Sunny Isles, understanding condo insurance is not optional. Your HOA’s master policy only covers part of the picture, and without the right individual coverage, you could face devastating financial losses from a single water leak, hurricane, or liability claim.

This guide explains exactly what condo insurance covers, how it works alongside your HOA’s master policy, what it costs in Florida, and how to make sure you are properly protected as a condo owner.

What Is Condo Insurance (HO-6)?

Condo insurance, formally known as an HO-6 policy, is a specialized type of homeowners insurance designed specifically for condominium and co-op owners. Unlike a standard homeowners insurance policy (HO-3), which covers an entire house and its surrounding structures, an HO-6 policy is built to cover what your condo association’s master insurance policy does not.

Your condo association carries a master policy that generally covers the building’s exterior, common areas like hallways, lobbies, elevators, and pools, and the structural components of the building. However, the master policy typically stops at the walls of your individual unit. Everything inside your unit, from your kitchen cabinets to your furniture to your personal liability exposure, is your responsibility to insure.

That is exactly the gap an HO-6 condo insurance policy fills. It picks up where the master policy leaves off, providing coverage for your unit’s interior, your personal belongings, and your financial protection if someone gets injured in your home.

For Florida condo owners, this coverage is especially critical. The state’s exposure to hurricanes, tropical storms, flooding, and water damage makes adequate homeowners insurance and condo insurance a financial necessity.

Key Condo Insurance Terms Explained

When you’re reviewing your condo insurance policy, you’ll come across a few key terms that define how your coverage works and what it costs. Getting a handle on these concepts—premium, deductible, and limits—is the first step to making sure your policy is structured to protect you properly. Let’s break down what each one means for you.

Premium

Your premium is simply the price you pay for your insurance policy. Think of it as your subscription fee for financial protection, which you can typically pay monthly or once a year. This cost isn’t random; it’s calculated based on several factors, including the value of your condo, the amount of coverage you select, and your personal claims history. For condo owners focused on managing their expenses, understanding what drives your premium is key. It allows you to work with your advisor to find the right balance between comprehensive coverage and a cost that fits your financial strategy, ensuring you’re not overpaying for protection you don’t need.

Deductible

The deductible is the portion of a claim that you agree to pay yourself before your insurance company steps in to cover the rest. For example, if you have a $1,000 deductible and suffer $10,000 in covered damages, you would pay the first $1,000, and your insurer would handle the remaining $9,000. Choosing your deductible is a strategic decision. Opting for a higher deductible will usually lower your annual premium, which can be great for your budget. However, you need to be comfortable with paying that higher amount out-of-pocket if you ever need to file a claim. It’s all about finding a balance that aligns with your personal financial situation and risk tolerance.

Limits

Policy limits are the maximum dollar amount your insurance provider will pay out for a covered loss. Your HO-6 policy will have separate limits for different types of coverage, such as personal property, liability, and loss of use. It’s incredibly important to review these numbers carefully. If a fire destroyed your belongings and the cost to replace them was $75,000, but your personal property limit was only $50,000, you would be responsible for the $25,000 difference. Ensuring your coverage limits are high enough to protect your assets is one of the most critical parts of building a solid personal insurance plan, especially if you own valuable items like art, jewelry, or high-end electronics.

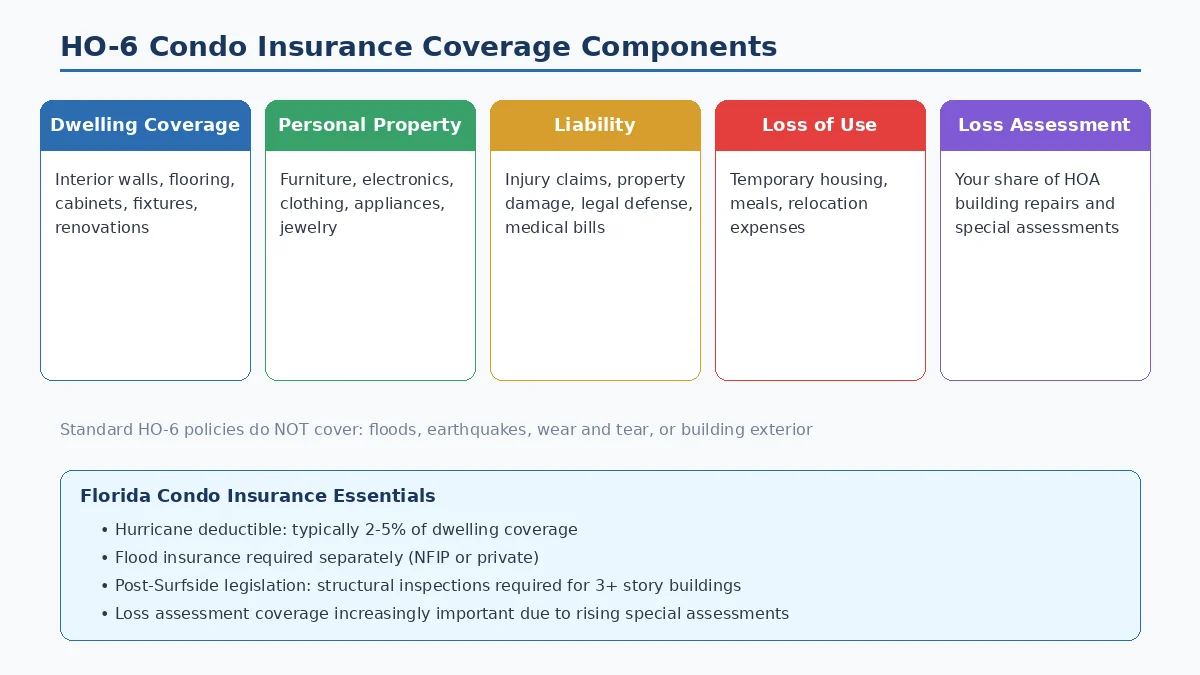

What Your Condo Insurance Policy Actually Covers

A standard HO-6 condo insurance policy includes several types of coverage that work together to protect you financially. Understanding each component helps you choose the right coverage limits for your situation.

Protecting Your Unit’s Interior (Dwelling Coverage)

Dwelling coverage protects the interior structure of your condo unit. This includes walls, flooring, ceilings, countertops, cabinets, bathroom fixtures, built-in appliances, and any improvements or renovations you have made to the unit.

If a covered event like a fire, burst pipe, or windstorm damages the interior of your condo, dwelling coverage pays for the repairs. The amount of dwelling coverage you need depends on your HOA’s master policy type:

- Bare-walls coverage: If your HOA has a bare-walls master policy, it only covers the building from the drywall outward. You are responsible for insuring everything inside, including original fixtures, flooring, cabinets, and appliances. You will need higher dwelling coverage limits.

- All-in (single entity) coverage: If your HOA has an all-in master policy, it covers the building structure plus original fixtures and finishes within units. You still need dwelling coverage for any upgrades, renovations, or improvements you have made beyond the original build-out.

Understanding Replacement Cost vs. Market Value

When you are setting your dwelling coverage limits, it is essential to understand the difference between replacement cost and market value. Market value is what your condo could sell for on the real estate market, a figure that includes factors like location, school districts, and current housing trends. Replacement cost, on the other hand, is the actual price of materials and labor required to repair or rebuild your unit’s interior to the condition it was in before the damage occurred. Your HO-6 policy is designed to cover the replacement cost, not the market value, which is a critical distinction for every condo owner to grasp.

Think about it this way: if a kitchen fire destroys your custom cabinetry and high-end appliances, your insurance pays to replace them with new items of similar quality at today’s prices. The policy does not care if the real estate market is up or down. A general guideline for estimating your dwelling coverage needs is to insure for about $40 to $60 per square foot. However, this is just a starting point. If you have made significant upgrades or have luxury finishes, your actual replacement cost will be higher, so a detailed inventory is the best way to determine the right amount of coverage.

Keeping Your Belongings Safe

Personal property coverage protects your belongings inside the condo. This includes furniture, electronics, clothing, kitchenware, sporting equipment, and other personal items. If your belongings are damaged, destroyed, or stolen due to a covered peril, this coverage reimburses you.

Most HO-6 policies cover personal property against named perils including fire, lightning, windstorm, hail, theft, vandalism, and water damage from burst pipes. Keep a detailed home inventory of your possessions with photos and receipts to streamline the claims process if you ever need to file.

Special Coverage for High-Value Items

While your personal property coverage protects your furniture and clothes, it’s important to know that standard HO-6 policies have strict limits on high-value items. Things like jewelry, fine art, antiques, and high-end electronics often have a specific, and surprisingly low, cap on what the insurance company will pay out—for instance, a policy might cap jewelry theft at just $1,500. If you own an engagement ring, a luxury watch, or a piece of art worth more than that, you would face a significant financial loss. This is a critical detail many condo owners miss until it’s too late.

The solution is to add a “rider” or schedule your valuable items separately. This is called a scheduled personal property endorsement, and it insures each specific item for its fully appraised value. This not only closes the coverage gap but often provides broader protection against more types of loss, like misplacing an item. Properly insuring your valuables requires a strategic approach, from getting professional appraisals to structuring the right endorsements. As advisors for high-net-worth individuals, we can help you build a policy that provides comprehensive protection for everything you own.

Protection When Accidents Happen

Liability coverage protects you financially if someone is injured while visiting your condo or if you accidentally cause damage to someone else’s property. If a guest slips on your wet floor and breaks their arm, or if a water leak from your unit damages the unit below yours, liability coverage pays for medical bills, legal defense costs, and settlement amounts.

Most insurance experts recommend carrying at least $300,000 in liability coverage for a condo. If you have significant assets to protect, consider pairing your HO-6 policy with an umbrella insurance policy for an additional layer of protection.

When Your Condo is Unlivable: Loss of Use Coverage

If a covered event makes your condo uninhabitable, loss of use coverage pays for temporary living expenses while your unit is being repaired. This includes hotel costs, restaurant meals, and other necessary expenses above your normal cost of living.

For Florida condo owners, this coverage is particularly important during hurricane season. If a major storm damages your unit and you need to relocate for weeks or months, loss of use coverage keeps you financially stable during the displacement.

Covering Unexpected HOA Assessments

Loss assessment coverage is unique to condo insurance and often overlooked. If your condo association’s master policy does not fully cover a major loss to common areas or the building structure, the association can levy a special assessment against all unit owners to cover the shortfall.

For example, if a hurricane causes $2 million in damage to the building but the master policy only covers $1.5 million, the remaining $500,000 could be divided among all unit owners. Loss assessment coverage on your HO-6 policy helps pay your share of that assessment.

After the Surfside condo collapse in 2021, many Florida condo associations significantly increased their insurance requirements and reserve funding. This has made loss assessment coverage even more important for Florida condo owners, as special assessments have become more common.

Considering your condo insurance options? Contact Insurance Underwriters at 305-900-2823 for a personalized coverage review from experienced advisors who understand the South Florida condo market.

What Isn’t Covered: Common Exclusions

While an HO-6 policy provides essential protection, it’s just as important to understand what it doesn’t cover. A common mistake is assuming your policy or the HOA’s master policy will handle every type of damage. Standard condo policies typically exclude damage from natural wear and tear, intentional acts, and owner negligence. More importantly, certain major perils often require separate coverage. For instance, damage from flooding is almost never included in a standard HO-6 policy; you’ll need a distinct flood insurance policy for that. Similarly, issues like mold or damage from pests may have limited or no coverage, leaving you responsible for costly remediation. Understanding these exclusions is the first step to building a truly comprehensive protection plan and avoiding unexpected claim denials.

Condo vs. Homeowners Insurance: What’s the Difference?

Many first-time condo buyers assume their coverage works the same as traditional homeowners insurance. While there are similarities, several critical differences affect how you are protected.

| Feature | Condo Insurance (HO-6) | Homeowners Insurance (HO-3) |

|---|---|---|

| Structure coverage | Interior of unit only | Entire home structure + other structures |

| Exterior coverage | Covered by HOA master policy | Included in your policy |

| Common areas | Covered by HOA master policy | Not applicable |

| Loss assessment | Included | Not applicable |

| Dwelling coverage basis | Interior improvements and fixtures | Full replacement cost of home |

| Average annual cost | $500-$2,000 (Florida) | $2,000-$5,000+ (Florida) |

| Required by | Mortgage lender + HOA bylaws | Mortgage lender |

The most important distinction is scope: your condo policy works in tandem with the HOA master policy to create complete coverage. A homeowners policy stands alone. This shared-responsibility model is why reviewing your HOA’s master policy is the essential first step before purchasing condo insurance.

Your Policy vs. the HOA’s: Who Covers What?

Understanding the boundary between your personal HO-6 policy and your condo association’s master policy is essential. Gaps in this coverage boundary are where most condo owners get caught off guard.

| Coverage Area | Your HO-6 Policy | HOA Master Policy |

|---|---|---|

| Building exterior (roof, siding, structure) | No | Yes |

| Common areas (lobby, hallways, pool, gym) | No | Yes |

| Interior walls, flooring, cabinets | Yes (varies by master policy type) | Bare-walls: No / All-in: Original only |

| Your personal belongings | Yes | No |

| Upgrades and renovations you made | Yes | No |

| Your personal liability | Yes | No |

| Common area liability (slip and fall in lobby) | No | Yes |

| Loss assessment (your share of building repairs) | Yes | Covers the building claim itself |

| Additional living expenses | Yes | No |

Pro tip: Request a copy of your HOA’s master policy from your property manager or board. Identify whether it is a bare-walls or all-in policy, then make sure your HO-6 dwelling coverage fills the remaining gap.

Types of HOA Master Policies

Before you can determine how much dwelling coverage you need, you have to know what your HOA’s master policy already covers. These policies generally fall into one of a few categories, and the type your association holds directly impacts the amount of coverage you’ll need to purchase for your own HO-6 policy. You can find this information in your HOA documents or by asking your property manager. Getting this detail right is the foundation of building a solid condo insurance plan that doesn’t leave you with unexpected and costly gaps.

Bare Walls Coverage

This is the most basic type of master policy, sometimes called “studs-out” coverage. A bare-walls policy covers the physical structure of the building—the exterior, roofing, and framing—along with common areas. However, its protection stops at the drywall of your individual unit. This means you are responsible for insuring everything inside your condo, from the flooring and lighting fixtures to the kitchen cabinets and built-in appliances. If your HOA has a bare-walls policy, you will need to secure a higher amount of dwelling coverage on your HO-6 policy to ensure the entire interior of your home can be rebuilt after a major loss.

Single Entity Coverage

A step up from bare-walls, a “single entity” policy covers the building structure and common areas, plus the standard fixtures inside each unit as they were originally built. This typically includes the original cabinets, plumbing, wiring, and standard flooring that came with the unit. With this type of master policy, your personal HO-6 dwelling coverage only needs to account for your personal belongings and any upgrades or renovations you’ve made. For example, if you replaced the original laminate countertops with granite or installed custom hardwood floors, you would need to insure the value of those specific upgrades on your own policy.

All-In Coverage

Often considered the most comprehensive type of master policy, “all-in” coverage typically includes the building, common areas, and all fixtures within a unit, including improvements and upgrades made by you or previous owners. While this sounds like it covers everything, the specifics can vary greatly between associations. It’s crucial to confirm exactly what is considered an “improvement” under your HOA’s specific policy. Even with this extensive coverage, you still absolutely need an HO-6 policy to protect your personal belongings, cover your personal liability, and pay for additional living expenses if a covered event forces you from your home.

Covering the Master Policy Deductible Gap

One of the most critical and frequently overlooked parts of condo insurance is loss assessment coverage. Imagine a hurricane causes major damage to your building’s roof and common areas. If the total repair cost exceeds the master policy’s coverage limit, or if the policy has a massive deductible, the HOA can levy a “special assessment” to make up the difference. This means every unit owner has to pay their share of the shortfall, which can easily run into thousands of dollars. This is precisely where loss assessment coverage steps in to protect you, paying for your portion of that shared expense so you aren’t hit with a sudden, massive bill. Given the rising costs of construction and insurance in Florida, ensuring you have adequate loss assessment coverage is a non-negotiable part of a sound financial plan. When you request a home insurance quote, our advisors can help you determine the right amount for your specific building.

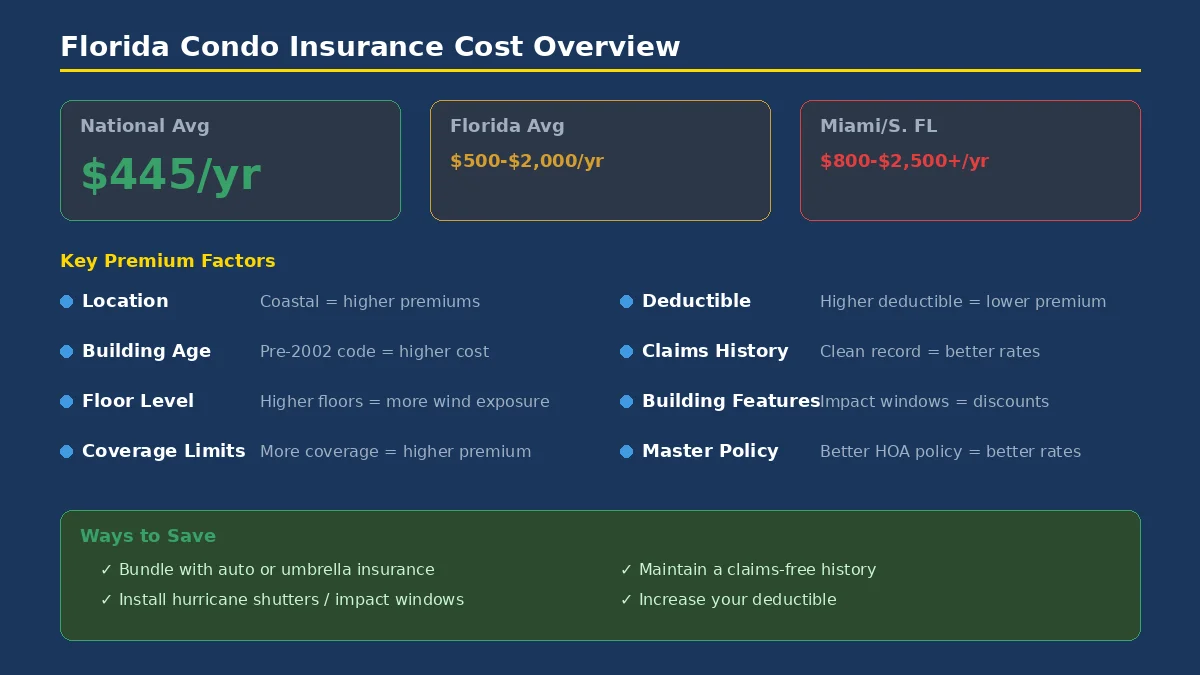

How Much Does Condo Insurance Cost in Florida?

Condo insurance costs in Florida vary based on several factors, but you can expect to pay more than the national average due to the state’s hurricane risk profile and ongoing insurance market challenges.

Average Condo Insurance Costs in Florida

- National average: Approximately $445 per year for a standard HO-6 policy

- Florida average: $500 to $2,000+ per year depending on location, coverage limits, and building characteristics

- Miami/South Florida: $800 to $2,500+ per year for units in high-rise buildings near the coast

Florida Costs vs. the National Average

When you look at condo insurance costs, Florida stands in a league of its own compared to the rest of the country. While the national average for a standard HO-6 policy hovers around $445 per year, Florida residents often see premiums ranging from $500 to over $2,000 annually. In high-risk coastal areas like Miami and South Florida, those costs can climb even higher, from $800 to $2,500 or more, especially for units in high-rise buildings. This significant price difference is driven by the state’s unique exposure to hurricanes and tropical storms, which creates a much higher-risk environment for insurers. Understanding this context is the first step in budgeting for the right level of condo insurance to protect your investment in the Sunshine State.

What Determines Your Insurance Rate?

Several factors influence your condo insurance premium:

- Location: Coastal units in Miami Beach, Brickell, Sunny Isles, and Fort Lauderdale face higher premiums due to hurricane and flood exposure.

- Floor level: Higher floors may have lower water damage risk but higher wind damage exposure.

- Building age and construction: Older buildings, especially those built before Florida’s updated building codes in 2002, often cost more to insure.

- Coverage limits: Higher dwelling, personal property, and liability limits increase your premium.

- Deductible amount: Choosing a higher deductible lowers your annual premium but increases your out-of-pocket cost during a claim.

- Claims history: Both your personal claims history and the building’s claims history affect pricing.

- HOA master policy quality: Buildings with comprehensive master policies and adequate reserves may qualify for better rates.

- Building safety features: Fire sprinklers, impact-resistant windows, modern electrical systems, and 24/7 security can reduce premiums.

How Condo Value and Location Affect Your Premium

In Florida, your condo’s location is one of the biggest drivers of your insurance premium. A unit in a high-risk coastal area like Miami Beach, Brickell, or Sunny Isles will naturally have a higher premium due to the increased exposure to hurricanes and flooding. It’s why policies for units in South Florida high-rises can range from $800 to over $2,500 annually. Beyond the zip code, the building’s age and construction play a huge role; a structure built before the state’s 2002 building code updates will almost always cost more to insure. The value of your condo’s interior—from custom cabinetry to your personal belongings—also directly impacts your premium. The more it would cost to rebuild and replace everything, the higher the coverage limits you’ll need, which is reflected in your final condo insurance cost.

Smart Ways to Save on Condo Insurance

- Bundle your condo insurance with auto or umbrella insurance for a multi-policy discount

- Install impact-resistant windows and hurricane shutters

- Maintain a claims-free history

- Increase your deductible if you can absorb a higher out-of-pocket cost

- Ask about discounts for new construction or recently renovated buildings

- Work with an independent insurance advisor who can compare rates across multiple carriers

Discounts for Safety and Security Features

Insurance carriers reward homeowners who actively reduce their risk. By installing certain protective devices in your condo, you can often qualify for significant discounts on your premium. Insurers see features like monitored fire and burglary alarms, deadbolt locks, and smoke detectors as signs of a responsible owner, which can translate directly into savings. In Florida, this is especially true for hurricane mitigation features. If your unit has impact-resistant windows or storm shutters, make sure your insurance provider knows about it, as these can be some of the most valuable credits available. You can often save money by installing safety features, so be sure to document every upgrade and discuss it with your advisor to ensure you are receiving every possible discount.

Savings for Paying Your Premium in Full

One of the simplest ways to lower your annual condo insurance cost is to pay your entire premium upfront. While paying in monthly installments can be convenient for budgeting, it often comes with small administrative or service fees that add up over the course of the year. Insurance companies save on billing and processing costs when you pay in a single lump sum, and they typically pass a portion of those savings on to you in the form of a discount. If your financial situation allows for it, opting for a pay-in-full plan is a straightforward strategy to reduce your overall expense without changing your coverage or deductible. When you review your policy options, ask your advisor to show you the cost difference between a monthly payment plan and a single annual payment.

Is Condo Insurance Required in Florida?

Florida has specific requirements and regulations that affect condo insurance for both unit owners and associations.

What Your Mortgage Lender Will Require

If you have a mortgage on your condo, your lender will require you to carry an HO-6 policy. This is standard across virtually all mortgage products. The lender needs assurance that their financial interest in the property is protected.

Understanding Your HOA’s Insurance Rules

Many Florida condo associations now require unit owners to maintain a minimum level of HO-6 coverage, including specific liability limits. Check your HOA’s bylaws and covenants for these requirements before purchasing your policy.

How New Florida Laws Affect Your Insurance

Following the tragic Surfside condo collapse in June 2021, Florida enacted significant legislation affecting condo associations:

- Structural inspections: Condos three stories or taller must undergo milestone structural inspections at 30 years of age (25 years if within three miles of the coast), then every 10 years after.

- Reserve funding: Associations can no longer waive or reduce funding for structural reserves. Full funding is required for roof, structure, waterproofing, electrical, plumbing, and other critical systems.

- Structural integrity reserve studies (SIRS): Required every 10 years to determine the funding needed for major structural components.

These requirements have led to increased HOA fees and special assessments across Florida. For condo owners, this makes loss assessment coverage on your HO-6 policy more valuable than ever, because special assessments to fund building repairs and reserves have become increasingly common.

Do You Need Separate Flood Insurance?

Standard condo insurance does not cover flood damage. In Florida, especially in coastal areas of Miami-Dade, Broward, and Palm Beach counties, flood insurance is often required by mortgage lenders if your building is in a designated flood zone.

The National Flood Insurance Program (NFIP) offers flood policies for condo unit owners starting at relatively affordable rates, though private flood insurance options are also available and sometimes offer better coverage or pricing.

Calculating Your Dwelling Coverage Needs

This is where your personal policy does the heavy lifting. Dwelling coverage protects the interior of your condo—think walls, flooring, cabinets, built-in appliances, and any renovations you’ve made. The right amount isn’t a guess; it’s a calculation based on your HOA’s master policy. If your association has a “bare-walls” policy, you’re responsible for everything from the drywall in, meaning you’ll need higher limits. If they have an “all-in” policy that covers original fixtures, you still need to insure all your upgrades and improvements. The key is to review your HOA documents to understand exactly where their coverage stops so you can build a policy that provides seamless, strategic protection with no expensive gaps.

Determining Your Personal Property Limits

Your personal property coverage protects everything you own inside your unit, from your sofa and TV to your clothes and kitchenware. The best way to determine your limit is to create a home inventory. This doesn’t have to be a complicated spreadsheet. Simply walk through your condo with your smartphone and record a video, narrating the items in each room and estimating their value. This simple exercise gives you a realistic total and creates a digital record that will be invaluable if you ever need to file a claim. Remember that standard policies have limits on high-value items like jewelry, art, and collectibles, so you may need separate coverage for those pieces.

Understanding Loss of Use Limits

Loss of use coverage is your financial safety net if a covered disaster, like a fire or hurricane, makes your condo uninhabitable. It pays for the additional living expenses you incur while you’re displaced, such as hotel bills, restaurant meals, and laundry services. For anyone living in Florida, this coverage is non-negotiable. A major storm could force you out of your home for weeks or even months during repairs. Loss of use ensures that a catastrophic event doesn’t also create a financial crisis, allowing you to maintain your normal standard of living while your home is being restored. It’s a critical component for weathering Florida’s unpredictable hurricane season.

Common Mistakes to Avoid with Condo Insurance

Navigating condo insurance can feel tricky, but avoiding a few common pitfalls can save you from major financial headaches down the road. Many condo owners make incorrect assumptions about their coverage, leaving them exposed when a disaster strikes. Understanding these mistakes is the first step toward building a solid financial safety net for your home and belongings. From misinterpreting the HOA’s role to neglecting policy updates, these errors are easy to make but also easy to prevent with a bit of foresight and the right guidance.

Assuming Your HOA Master Policy Covers Everything

The single biggest mistake condo owners make is believing their HOA’s master policy provides complete protection. Your condo association carries a master policy that generally covers the building’s exterior, common areas like hallways, lobbies, elevators, and pools, and the structural components of the building. However, the master policy typically stops at the walls of your individual unit. Everything inside your unit—from the drywall and flooring to your kitchen cabinets and personal belongings—is your responsibility to insure. Relying solely on the HOA policy leaves your personal assets and the interior of your home completely unprotected against risks like fire, theft, or water damage.

Underinsuring Your Personal Property

It is incredibly easy to underestimate the total value of your personal belongings. Think about everything you own: furniture, electronics, clothing, kitchenware, art, and jewelry. If you had to replace it all at once after a fire or major theft, the cost would likely be much higher than you think. Most HO-6 policies cover personal property against named perils including fire, lightning, windstorm, hail, theft, vandalism, and water damage from burst pipes. To avoid being underinsured, you should create a home inventory to accurately calculate the coverage you need. Without an adequate limit, you could be left paying out-of-pocket to replace essential items.

Forgetting to Update Your Policy After Renovations

If you have recently renovated your kitchen, updated your bathrooms, or installed new flooring, your condo’s value has increased. Your insurance coverage needs to reflect that. The amount of HO-6 coverage you need depends on your condo unit, your lifestyle, and what your condo association’s master policy already covers. Failing to inform your insurance provider about significant upgrades means your dwelling coverage limit may no longer be sufficient to cover a total loss. After any major renovation, you should contact your insurance advisor to adjust your policy and ensure your investment is fully protected.

Best Practices for Managing Your Condo Policy

Securing the right condo insurance policy is just the beginning. Proactive management is key to ensuring your coverage remains adequate and effective over time. Your life, your belongings, and even your building’s policies can change, creating potential gaps if your policy stays static. By adopting a few simple best practices, you can maintain robust protection, streamline any future claims, and make sure you are never paying for more coverage than you need or carrying less than you require. These habits empower you to treat your insurance as the strategic asset it is.

Create a Detailed Home Inventory

One of the most effective things you can do to prepare for a potential claim is to create a thorough inventory of your possessions. Keep a detailed home inventory of your possessions with photos and receipts to streamline the claims process if you ever need to file. You can use a simple spreadsheet, a dedicated app, or even just a video walkthrough of your home where you describe your items and their approximate value. Store this inventory in a secure cloud-based location so it is accessible even if your computer or phone is destroyed. This simple step can turn a stressful claims process into a straightforward one.

Review Your Coverage Annually

Insurance is not a “set it and forget it” product. It is crucial to review your HO-6 policy and your condo association’s master policy every year. This helps make sure you do not have gaps in your coverage. Your HOA could change its master policy, or you may have acquired new, valuable items that require additional coverage. An annual review with your insurance advisor ensures your policy limits for dwelling, personal property, and liability are still appropriate for your current situation. This proactive check-up is essential for maintaining your financial security and peace of mind.

Work With an Independent Insurance Advisor

The Florida insurance market is complex, with unique challenges related to weather and regulations. Instead of going it alone, work with an independent insurance advisor who can compare rates across multiple carriers. An expert advisor at a firm like Insurance Underwriters does more than just find a competitive price; we act as your risk management partner. We can help you decipher your HOA’s master policy, identify potential gaps, and structure a comprehensive HO-6 policy that aligns with your specific needs and risk tolerance, ensuring you have strategic protection in place.

How to File a Condo Insurance Claim

Filing a condo insurance claim requires understanding which policy covers the damage. Here is a step-by-step process:

- Assess the damage and ensure safety. Do not re-enter your unit until it is safe. Document all damage with photos and videos before making any repairs.

- Determine which policy covers the loss. If the damage is to your unit’s interior or belongings, it falls under your HO-6 policy. If it involves the building structure, exterior, or common areas, contact your HOA to file under the master policy.

- Notify your insurance company promptly. Most policies require timely notification. Call your agent or the insurer’s claims line as soon as possible.

- Document everything. Keep receipts for temporary repairs, additional living expenses, and damaged items. Your home inventory list is essential here.

- Meet with the adjuster. Your insurer will send an adjuster to assess the damage. Be present during the inspection and point out all damage.

- Review the settlement offer. Compare the offer to your actual losses. If the offer seems low, you have the right to negotiate or hire a public adjuster.

- Keep records of all communication. Document every phone call, email, and letter related to your claim.

For water damage claims, which are among the most common in Florida condos, determining responsibility can be complex. If a pipe bursts in the unit above you and water damages your ceiling and belongings, your HO-6 policy covers your losses. The unit owner upstairs may be liable for the source of the damage through their own liability coverage.

Tips for Miami and South Florida Condo Owners

South Florida’s unique real estate market and weather patterns create specific insurance considerations for condo owners in the region.

Getting Your Condo Ready for Hurricane Season

- Know your hurricane deductible. Florida condo policies often have a separate, higher deductible for hurricane damage, typically 2-5% of your dwelling coverage amount.

- Document your belongings before hurricane season each year. Update your inventory with photos and current values.

- Understand the difference between wind damage (covered by your condo policy) and flood damage (requires separate flood insurance).

What to Know if You Live in a High-Rise

Miami’s skyline is filled with high-rise condominiums in neighborhoods like Brickell, Downtown, Edgewater, and Sunny Isles Beach. High-rise condo owners should pay attention to:

- Wind mitigation: Buildings with impact-resistant glass and structural wind mitigation features often qualify for significant premium discounts.

- Water damage risks: High-rise buildings have extensive plumbing systems. Water damage from broken pipes is one of the most frequent condo insurance claims.

- Building-wide coverage quality: Research the building’s master policy, insurance reserves, and recent inspection results before purchasing a unit.

Protecting Yourself from Special Assessments

With Florida’s new structural inspection and reserve funding requirements, many condo associations are issuing special assessments that can range from a few thousand dollars to over $100,000 per unit for major structural repairs.

- Purchase adequate loss assessment coverage on your HO-6 policy. Standard limits may be $1,000, but you can often increase this to $25,000 or $50,000 for a modest additional premium.

- Review your building’s most recent reserve study and structural inspection report.

- Factor potential special assessments into your overall budget when purchasing a condo in Florida.

How Much Condo Insurance Do You Need?

Determining the right amount of condo insurance requires evaluating several factors specific to your situation:

- Review your HOA master policy. Identify the coverage type (bare-walls vs. all-in) and note any deductible amounts that could be assessed to unit owners.

- Calculate your dwelling coverage needs. Estimate the cost to rebuild the interior of your unit, including all fixtures, flooring, cabinets, countertops, and any upgrades or renovations.

- Inventory your personal property. Add up the replacement cost of all your belongings. Most people underestimate this figure. A typical condo unit may contain $50,000 to $150,000 worth of personal property.

- Assess your liability exposure. At minimum, carry $300,000 in liability coverage. If you have a higher net worth, consider $500,000 or more plus an umbrella policy.

- Consider loss assessment limits. Given Florida’s current condo regulatory environment, increasing your loss assessment coverage above the default is strongly recommended.

- Add flood insurance if needed. If your building is in or near a flood zone, separate flood coverage is essential.

Not a condo owner? If you rent your unit, you need a different type of policy. Our renters insurance Florida guide explains the HO-4 coverage designed specifically for tenants.

Frequently Asked Questions About Condo Insurance

What is condo insurance (HO-6)?

Condo insurance, also called an HO-6 policy, is a specialized homeowners insurance policy designed for condominium and co-op owners. It covers the interior of your unit, your personal belongings, personal liability, additional living expenses, and loss assessments. It works alongside your HOA’s master policy to provide complete coverage for your condo.

What does condo insurance cover?

A standard HO-6 policy covers dwelling (interior structure), personal property (belongings), personal liability (injury or damage claims), loss of use (temporary living expenses), and loss assessment (your share of building-wide repair costs). It does not cover floods, earthquakes, or damage to the building exterior or common areas.

How much does condo insurance cost in Florida?

Florida condo insurance typically costs between $500 and $2,000+ per year, depending on your location, coverage limits, building characteristics, and claims history. Coastal units in Miami and South Florida generally fall on the higher end of this range due to hurricane and flood exposure.

Is condo insurance required in Florida?

Condo insurance is required by mortgage lenders and often required by HOA bylaws. Even if you own your condo outright and your HOA does not mandate it, carrying an HO-6 policy is strongly recommended to protect your personal assets and liability exposure.

What is the difference between condo insurance and homeowners insurance?

Condo insurance (HO-6) covers only the interior of your unit and works alongside your HOA’s master policy. Homeowners insurance (HO-3) covers your entire home structure, including the exterior and other structures on your property. Condo insurance also includes loss assessment coverage, which homeowners insurance does not.

Does condo insurance cover water damage?

Yes, most HO-6 policies cover sudden and accidental water damage from sources like burst pipes, appliance malfunctions, and accidental overflow. However, flood damage from external water sources (storm surge, heavy rainfall) requires a separate flood insurance policy.

Get the Right Protection for Your Florida Condo

The right condo insurance policy is your financial safety net as a condo owner. Between hurricane exposure, water damage risks, rising special assessments, and personal liability, going without adequate HO-6 coverage is a gamble no Florida condo owner should take.

Insurance Underwriters specializes in personal insurance for Florida condo owners, homeowners, and high-net-worth individuals. Our experienced advisors understand the unique challenges of insuring condos in Miami, South Florida, and throughout the state.

Request a home insurance quote or call us at 305-900-2823 to get a personalized condo insurance review. We will analyze your HOA’s master policy, identify coverage gaps, and build an HO-6 policy that fully protects your unit, your belongings, and your financial future.

If you own valuable artwork, our fine art insurance guide explains how to protect your collection with specialized coverage.

Key Takeaways

- Know where your HOA’s coverage ends and yours begins: Your association’s master policy protects the building’s structure and common areas, leaving you responsible for insuring your unit’s interior, your personal belongings, and your liability. An HO-6 policy is designed to fill these exact gaps.

- Structure your policy to cover your entire lifestyle: A comprehensive HO-6 policy protects more than just your walls. It should include enough dwelling coverage for renovations, personal property coverage for all your belongings, and liability protection in case of accidents.

- Address Florida-specific risks with targeted coverage: Standard condo insurance does not cover flooding, making a separate flood policy essential for many. It’s also wise to increase your loss assessment coverage to protect yourself from expensive, building-wide repair bills passed on by your HOA.

Comments

Comments are closed.