Watercraft Insurance: A Complete Guide

Watercraft insurance protects your investment in boats, jet skis, personal watercraft (PWC), sailboats, and yachts from accidents, theft, storms, and liability claims. Whether you cruise Biscayne Bay every weekend or dock a yacht at a Miami Beach marina, the right policy keeps you financially protected on the water.

Get a free watercraft insurance quote from Insurance Underwriters today and protect your vessel before your next trip on the water.

This guide covers everything you need to know about watercraft insurance: the types of watercraft that need coverage, what each policy covers, how much it costs, and what South Florida boat owners should watch for when shopping for the right policy.

What Is Watercraft Insurance?

Watercraft insurance is a specialized policy that provides financial protection for vessels used on the water. It covers physical damage to your boat or personal watercraft, liability for injuries or property damage you cause to others, and additional protections like towing, salvage, and medical payments.

Many boat owners assume their homeowners insurance covers their watercraft. In most cases, that is not true. Standard homeowners policies only cover small boats with engines under 25 horsepower and values under a few thousand dollars. Anything beyond that, including jet skis, sailboats, fishing boats, and yachts, requires a dedicated watercraft insurance policy.

Unlike auto insurance, watercraft insurance is not legally required in most states. Florida does not mandate boat insurance. However, marina operators, lenders, and common sense all point toward carrying coverage. A single accident on the water can result in six-figure liability claims, and operating without a policy puts your personal assets at risk.

Types of Watercraft That Need Insurance

Watercraft insurance applies to a broad range of vessels. The type of watercraft you own directly affects your coverage options, premiums, and policy structure. Here is a breakdown of the most common types and their insurance considerations.

Motorboats and Fishing Boats

Center consoles, bass boats, pontoon boats, and other motorized vessels are the most commonly insured watercraft. If your boat has an engine, you need hull coverage for physical damage and liability coverage for third-party claims. Fishing boats may also need equipment coverage for rods, electronics, and tackle.

Personal Watercraft (Jet Skis and PWCs)

Jet skis and personal watercraft are among the most accident-prone vessels on the water. The U.S. Coast Guard reports that PWCs consistently rank in the top vessel categories for on-water accidents, with operator error accounting for approximately 90% of incidents. PWCs typically need their own standalone policy separate from boat insurance.

Sailboats

Sailboat insurance covers vessels from small day-sailers to offshore racing boats. Policies for sailboats often include provisions for rigging and sail damage, which motorboat policies do not. Larger sailboats used for cruising may need additional navigation territory endorsements.

Yachts

Yacht insurance is a specialized segment of watercraft coverage for vessels typically over 27 feet. Yacht policies often include crew liability, extended navigation territories, personal effects coverage, and higher liability limits. Owners of yachts docked at South Florida marinas should carry $500,000 or more in liability coverage.

Comparison: Watercraft Types and Coverage Needs

| Watercraft Type | Typical Value Range | Avg. Annual Premium | Key Coverage Needs |

|---|---|---|---|

| Jet Ski / PWC | $5,000 – $20,000 | $200 – $600 | Liability, collision, theft, towing |

| Fishing Boat (under 20 ft) | $10,000 – $40,000 | $300 – $600 | Hull, liability, equipment, towing |

| Pontoon Boat | $20,000 – $60,000 | $400 – $750 | Hull, liability, passenger medical |

| Center Console (20-30 ft) | $30,000 – $150,000 | $600 – $1,500 | Hull, liability, uninsured boater, salvage |

| Sailboat (under 30 ft) | $15,000 – $80,000 | $500 – $1,200 | Hull, rigging, liability, navigation territory |

| Yacht (40+ ft) | $200,000 – $2M+ | $2,000 – $8,000+ | Agreed value hull, high liability, crew, personal effects |

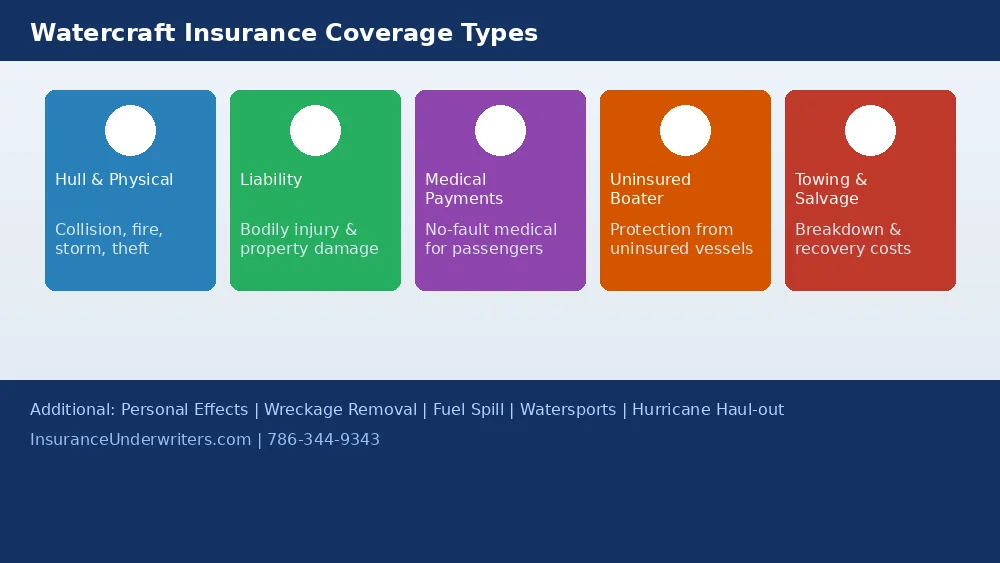

What Does Watercraft Insurance Cover?

A comprehensive watercraft insurance policy includes several layers of protection. Each coverage type addresses a different risk you face on the water.

Hull and Physical Damage Coverage

Hull coverage pays for repairs or replacement if your watercraft is damaged in a collision, fire, storm, theft, or vandalism. This is the equivalent of comprehensive and collision coverage in auto insurance. Two valuation methods exist:

- Agreed value: You and the insurer agree on a set value upfront. If your vessel is totaled, you receive the full agreed amount. This is the preferred option for most boat owners.

- Actual cash value: The payout is based on the depreciated market value at the time of loss. This results in lower premiums but smaller payouts.

For South Florida boaters, agreed value coverage is strongly recommended. Hurricane damage can total a vessel, and depreciated payouts rarely cover the cost of replacement.

Liability Coverage

Liability coverage protects you if you cause bodily injury or property damage to someone else while operating your watercraft. This includes legal defense costs, medical bills for the injured party, and repair costs for damaged property. Most marinas require a minimum of $100,000 in liability coverage, but carrying $300,000 to $500,000 is standard practice for responsible boat owners.

If you need liability protection beyond your watercraft policy limits, an umbrella insurance policy can add an extra $1 million or more in coverage.

Medical Payments Coverage

Medical payments coverage pays for medical bills for you and your passengers after a boating accident, regardless of who is at fault. This no-fault coverage is particularly important for families who take guests out on the water regularly. Typical limits range from $5,000 to $25,000 per person.

Uninsured/Underinsured Boater Coverage

This coverage protects you if you are involved in an accident with a boater who has no insurance or insufficient coverage to pay for your damages and injuries. Given that a significant percentage of boat owners nationwide operate without insurance, this coverage is essential for anyone on busy waterways like those in Miami-Dade and Broward counties.

Towing and Salvage Coverage

If your boat breaks down on the water, towing coverage pays for the cost of getting you back to shore or to the nearest marina. Salvage coverage handles the expense of recovering a sunken or stranded vessel, which can easily cost $10,000 or more. In South Florida, where boaters frequently travel to the Keys, the Bahamas, and offshore fishing grounds, towing coverage is not optional.

Additional Coverages to Consider

- Personal effects coverage: Protects items on board like electronics, fishing gear, and diving equipment.

- Wreckage removal: Covers the cost of removing your vessel if it sinks, which is often required by law.

- Fuel spill liability: Pays for cleanup costs if fuel or oil spills from your vessel.

- Watersports liability: Covers injuries to people being towed behind your boat (tubing, skiing, wakeboarding).

- Hurricane haul-out: Covers the cost of moving your boat to a safe location ahead of a storm.

Not sure which coverages you need? Request a personalized watercraft insurance quote from our team and we will help you build the right policy for your vessel.

How Much Does Watercraft Insurance Cost?

Watercraft insurance costs vary widely based on your vessel type, value, location, and coverage level. As a general rule, expect to pay between 1% and 3% of your boat’s value annually for comprehensive coverage.

For South Florida boat owners, premiums tend to run higher than the national average due to hurricane exposure, high boat traffic density, and saltwater corrosion risk. Here are the primary factors that affect your premium:

- Vessel value and age: Higher-value boats cost more to insure. Older vessels may have limited coverage options.

- Boat type and horsepower: High-performance boats and PWCs carry higher premiums due to accident risk.

- Navigation territory: Policies covering ocean navigation cost more than inland-only policies.

- Claims history: A clean record keeps premiums low. Prior claims increase your rate.

- Safety courses: Completing a boating safety course from the U.S. Coast Guard Auxiliary or a state-approved provider can reduce premiums by 5% to 15%.

- Storage method: Boats stored in covered facilities or on lifts cost less to insure than those left in the water year-round.

- Deductible level: Higher deductibles lower your premium but increase your out-of-pocket cost in a claim.

Watercraft Insurance in South Florida: What Local Boat Owners Should Know

South Florida is one of the largest recreational boating markets in the country. Miami-Dade, Broward, and Palm Beach counties have more registered vessels per capita than nearly any other metro area in the United States. Operating a boat here comes with unique insurance considerations.

Hurricane Coverage Is Non-Negotiable

Florida’s hurricane season runs from June 1 through November 30. Many standard watercraft policies include named storm deductibles that are separate from (and higher than) your standard deductible. A typical hurricane deductible is 2% to 5% of the insured value. On a $100,000 boat, that means $2,000 to $5,000 out of pocket before coverage kicks in.

Some insurers require a hurricane haul-out plan as a condition of coverage. Make sure your policy clearly defines what happens during named storm events, and verify whether your marina offers storm preparation services. For broader information on storm-related coverage in Florida, see our guide to flood insurance in Florida.

Saltwater and Corrosion Considerations

South Florida’s saltwater environment accelerates wear on engines, electronics, and hull materials. Insurers factor this into premiums and may require proof of regular maintenance. Keeping maintenance records can help with claims and may qualify you for premium discounts.

High-Traffic Waterways Increase Liability Risk

Biscayne Bay, the Intracoastal Waterway, and the channels around Miami Beach and Fort Lauderdale are among the busiest recreational waterways in the country. More boat traffic means more collision risk, which is why higher liability limits are recommended for South Florida boaters.

Liveaboard and Charter Considerations

If you live aboard your vessel or use it for charter purposes, standard watercraft insurance will not suffice. Liveaboard policies and charter boat insurance are specialized products that address the unique risks of commercial or residential use. Our team can help you find the right policy for these situations.

Watercraft Insurance vs. Homeowners Insurance

One of the most common misconceptions is that your homeowners insurance covers your boat. Here is the reality:

- Most homeowners policies cover boats with engines under 25 HP and values under $1,500 to $2,500.

- Liability coverage under homeowners policies is typically limited to $500 to $1,000 for watercraft-related incidents.

- Personal watercraft (jet skis, PWCs) are almost always excluded from homeowners policies.

- Any boat with a motor, trailer, or value above the sublimit requires a standalone watercraft policy.

If you own a home in Florida and a boat, you need separate policies for each. Your homeowners insurance in Florida protects your house. Your watercraft insurance protects your vessel. They are distinct products with distinct coverages. The same applies to condo owners who keep a boat at a nearby marina.

How to Choose the Right Watercraft Insurance Policy

Selecting the right watercraft insurance policy requires more than picking the cheapest quote. Here is what to evaluate:

- Choose agreed value over actual cash value. Agreed value policies pay the full insured amount in a total loss, giving you certainty when you need it most.

- Carry adequate liability limits. A minimum of $300,000 in liability coverage is recommended. High-net-worth individuals should consider $500,000 or more, supplemented by an umbrella policy.

- Understand your deductibles. Know your standard deductible and your named storm deductible separately. They are almost always different amounts.

- Verify navigation territory. If you plan to take your boat to the Bahamas, the Keys, or offshore, confirm your policy covers those waters.

- Add towing and salvage. This coverage is inexpensive relative to the potential cost of a tow or vessel recovery.

- Review personal effects limits. If you carry expensive electronics, fishing equipment, or diving gear, make sure your policy covers them.

- Work with an independent broker. An independent brokerage like Insurance Underwriters can shop multiple carriers to find the best combination of coverage and price for your specific vessel and situation.

Protecting valuable personal assets, including your watercraft, is part of a broader strategy. High-net-worth individuals who insure boats, yachts, and PWCs should also review their jewelry insurance and personal liability coverage to make sure all assets are properly protected.

Florida Boating Laws and Registration Requirements

While Florida does not require boat insurance, the state does have registration and safety requirements that every boat owner should know:

- Registration: All motorized vessels must be registered with the Florida Fish and Wildlife Conservation Commission (FWC). Registration fees are based on vessel length.

- Boater education: Anyone born on or after January 1, 1988, must complete an approved boating safety course to operate a vessel with 10 HP or more.

- Age restrictions: Operators under 14 cannot operate a PWC. Operators under 18 need to complete the boater safety course.

- Required safety equipment: All vessels must carry life jackets, fire extinguishers (where applicable), visual distress signals, and a sound-producing device.

Completing a boating safety course not only meets Florida’s legal requirement but also qualifies you for insurance discounts. Most insurers offer a 5% to 15% premium reduction for certified boaters.

For information on insurance requirements for vehicles used to tow boats, see our guide to commercial auto insurance. For a deeper look at Florida-specific boat coverage, read our boat insurance in Florida guide.

Common Watercraft Insurance Claims in Florida

Understanding the most frequent watercraft insurance claims helps you evaluate whether your policy has the right coverage. Here are the claim types Florida boat owners file most often:

- Collision damage: Hitting another vessel, a dock, a submerged object, or a navigational marker. This is the most common claim type on busy South Florida waterways.

- Hurricane and storm damage: Wind, surge, and debris can total a vessel in hours. Claims spike every year between August and October during peak hurricane season.

- Theft: Outboard motors, electronics, and even entire vessels are stolen from marinas and trailers. Miami-Dade ranks among the highest counties in the state for marine theft.

- Sinking: Whether from a hull breach, a failed bilge pump, or a through-hull fitting failure, sinking claims are expensive because they include salvage, environmental cleanup, and total loss payouts.

- Fire: Engine compartment fires, electrical shorts, and fuel system failures can destroy a boat in minutes. Fire claims are among the most costly.

- Grounding: Running aground in shallow channels, sandbars, or reef areas is common in the Florida Keys and Biscayne Bay. Damage to hulls, propellers, and lower units adds up quickly.

- Liability claims from passenger injuries: Slip-and-fall injuries on deck, tubing accidents, and collision-related passenger injuries generate liability claims that can exceed $100,000.

Each of these scenarios reinforces why carrying comprehensive watercraft insurance with adequate liability limits is not a luxury. It is a financial necessity for South Florida boat owners.

How to Save Money on Watercraft Insurance

You do not have to overpay for watercraft insurance. Here are proven strategies to lower your premium without sacrificing coverage:

- Complete a boating safety course: Most insurers offer 5% to 15% discounts for certified boaters.

- Bundle policies: Combining your watercraft insurance with your home, auto, or umbrella insurance through the same carrier can reduce overall costs.

- Increase your deductible: A higher deductible lowers your premium. Choose an amount you can comfortably pay out of pocket in a claim.

- Install safety equipment: Fire suppression systems, GPS tracking, and automatic engine shutoffs may qualify you for additional discounts.

- Store your boat properly: Keeping your vessel in a covered facility, on a lift, or in dry storage reduces risk and lowers your rate.

- Maintain a clean claims history: Avoiding small claims and maintaining a multi-year claims-free record results in lower renewal premiums.

- Work with an independent broker: Independent brokerages like Insurance Underwriters compare rates from multiple carriers, giving you access to competitive pricing that a single-carrier agent cannot match.

Frequently Asked Questions About Watercraft Insurance

Watercraft insurance is a policy that protects boats, jet skis, sailboats, yachts, and other water vessels from physical damage, theft, liability claims, and on-water emergencies. It covers repair costs, legal expenses, medical payments, and towing or salvage operations.

How much does watercraft insurance cost?

Watercraft insurance typically costs between 1% and 3% of your vessel’s value per year. A jet ski policy may start around $200 annually, while a yacht over 40 feet can cost $2,000 to $8,000 or more. Factors like location, vessel type, claims history, and coverage level all affect the final premium.

Do I need watercraft insurance in Florida?

Florida does not legally require boat insurance. However, your marina and your lender almost certainly will. Beyond that, operating any watercraft without liability coverage exposes you to significant financial risk if you cause an accident.

Does homeowners insurance cover my boat?

In most cases, no. Standard homeowners policies only cover very small boats (under 25 HP, under $1,500 to $2,500 in value). Jet skis, sailboats, and any motorboat above those limits need a separate watercraft insurance policy.

What is the difference between agreed value and actual cash value?

Agreed value means you and the insurer set a fixed payout amount when the policy is written. Actual cash value pays the depreciated market value at the time of a loss. Agreed value provides more certainty and is recommended for most boat owners.

Is jet ski insurance the same as boat insurance?

Not exactly. While both fall under the watercraft insurance umbrella, jet skis and PWCs often require standalone policies. Coverage for PWCs focuses on liability, collision, theft, and towing, while boat insurance typically includes broader hull and navigation territory provisions.

Protect Your Watercraft with Insurance Underwriters

Insurance Underwriters is a full-service independent brokerage based in Miami, Florida. We specialize in personal insurance solutions for boat owners, jet ski enthusiasts, and yacht owners throughout South Florida.

As an independent brokerage, we shop multiple insurance carriers to find the coverage and pricing that fits your specific vessel and situation. Whether you need a basic liability policy for a jet ski or a comprehensive agreed value policy for a 60-foot yacht, our team can build the right coverage package.

Get your free watercraft insurance quote today or call us at 786-344-9343 to speak with a watercraft insurance specialist.

Comments

Comments are closed.