Cyber Liability Insurance for Business in 2026

Cyber Liability Insurance for Business: Why Digital Protection Matters in 2026

Cyber liability insurance for business is no longer a nice-to-have policy for technology companies. In 2026, almost every business stores customer information, accepts digital payments, uses cloud software, or depends on email to operate. That means a single ransomware attack, fraudulent wire transfer, or data breach can interrupt revenue, damage client trust, and create legal costs long after systems come back online.

Need protection beyond a standard business policy? Get a commercial insurance quote from InsuranceUnderwriters.com and compare coverage options from top carriers.

The challenge is that many business owners still assume general liability or property insurance will cover a cyber event. In most cases, they will not. Cyber liability coverage is designed for the financial fallout that follows a digital incident, from breach notification and forensic investigation to ransomware response, business interruption, and third-party claims.

What Is Cyber Liability Insurance for Business?

Cyber liability insurance is a business insurance policy that helps cover the costs of cyber incidents involving data, networks, digital systems, and online operations. It can respond when sensitive information is exposed, software is locked by ransomware, a company network is compromised, or a client alleges that your security failure caused them financial harm.

For many companies, cyber coverage fills a major gap between traditional commercial policies and the realities of modern operations. A fire can damage a building. A slip and fall can create a bodily injury claim. But a phishing email that exposes client records or shuts down invoicing software creates a very different type of loss.

InsuranceUnderwriters.com works with businesses across industries to compare commercial coverage options, including specialty policies that address digital risk. Because the company represents more than 200 carriers and has a team of professional agents, business owners can review options without relying on one-size-fits-all coverage.

Why Cyber Risk Is a Business Risk in 2026

Cyber attacks are not limited to large corporations. Small and midsize companies are often attractive targets because they may hold valuable customer information without the same security budget as enterprise organizations.

The financial impact is also significant. IBM’s 2025 Cost of a Data Breach Report placed the global average cost of a data breach at $4.44 million, with costs varying by industry, geography, incident type, and response speed. The FBI’s Internet Crime Complaint Center reported more than $16 billion in cybercrime losses in 2024, showing how widespread digital fraud, business email compromise, and extortion have become.

Those numbers matter because the real cost of a cyber event is rarely just an IT invoice. A business may need legal counsel, customer notification, credit monitoring, public relations support, forensic specialists, lost income reimbursement, and help restoring operations. Without a dedicated policy, those costs may fall directly on the company.

What Does Cyber Liability Insurance Cover?

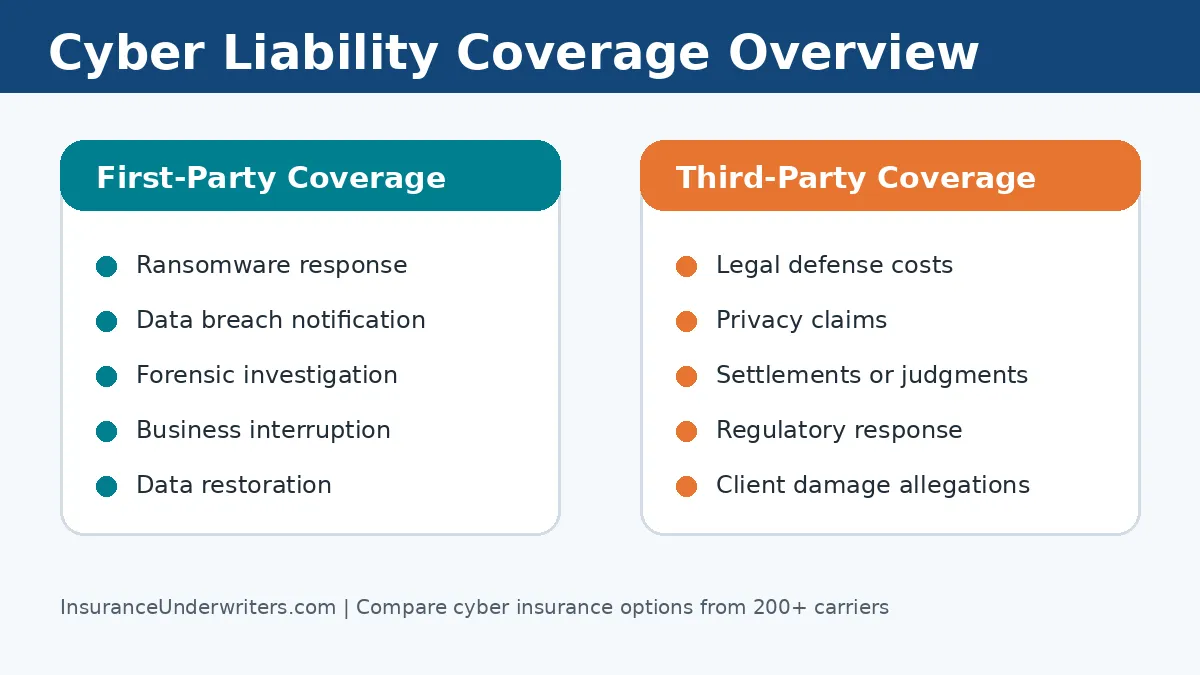

Cyber liability insurance can vary by carrier and policy form, but most business policies are built around two major categories: first-party coverage and third-party coverage.

First-party cyber coverage

First-party coverage helps pay for costs your business incurs directly after a cyber event. Common examples include:

- Data breach response: Costs to investigate what happened, identify affected records, notify impacted individuals, and provide support such as credit monitoring when appropriate.

- Ransomware and cyber extortion: Support for negotiating, responding to, and recovering from extortion demands, subject to policy terms and legal requirements.

- Business interruption: Lost income and extra expenses when a covered cyber event disrupts normal operations.

- Data restoration: Costs to recover or replace damaged data, software, or systems after a covered attack.

- Forensic investigation: Technical experts who determine how the incident happened, what systems were affected, and what must be remediated.

- Crisis management and public relations: Help communicating with customers, vendors, employees, and the public after a serious breach.

Third-party cyber liability coverage

Third-party coverage helps respond when another party claims your business caused them financial harm through a cyber incident. This may include:

- Legal defense costs: Attorney fees and related expenses if customers, vendors, or partners bring a claim.

- Settlements or judgments: Covered amounts your business is legally responsible to pay, subject to policy terms.

- Regulatory proceedings: Defense costs or penalties where insurable by law after a privacy or security event.

- Media liability: Claims involving online content, copyright issues, or digital communications, when included.

Cyber policies are not identical, which is why it is important to compare exclusions, sublimits, waiting periods, ransomware conditions, and breach response resources before choosing a carrier.

First-Party vs. Third-Party Cyber Insurance: What Is the Difference?

| Coverage Type | What It Protects | Common Examples |

|---|---|---|

| First-party cyber coverage | Your own business losses after a covered cyber event | Ransomware response, data recovery, breach notification, lost income, forensic investigation |

| Third-party cyber liability coverage | Claims made against your business by clients, vendors, regulators, or other outside parties | Legal defense, settlements, privacy claims, regulatory response, client damage allegations |

Bottom line: First-party coverage helps your company recover. Third-party coverage helps protect your company when others say your cyber failure harmed them. Many businesses need both.

Which Industries Need Cyber Liability Insurance Most?

Any company that uses digital systems should consider cyber insurance, but some industries face higher exposure because they handle sensitive information, process payments, or depend heavily on uptime.

- Healthcare and wellness practices: Patient records, billing information, appointment systems, and privacy requirements create serious cyber exposure.

- Professional services: Accountants, consultants, attorneys, agencies, and other advisors often store confidential client information.

- Retail and ecommerce: Payment processing, customer accounts, inventory systems, and online ordering can all be targeted.

- Real estate and property management: Wire transfers, tenant information, owner records, and vendor payments create fraud risk.

- Construction and trade businesses: Bid documents, payroll systems, supplier portals, and project management software are increasingly digital.

- Technology companies: Software providers, IT consultants, and managed service providers may face both first-party losses and client claims. See our technology insurance guide for related coverage considerations.

- Startups and LLCs: Newer businesses may be especially vulnerable because they are building systems quickly. If you operate through an LLC, our LLC insurance guide explains why the entity alone does not replace proper coverage.

Cyber insurance should also be considered when contracts require proof of coverage. Vendors, landlords, enterprise clients, and government buyers may ask for cyber liability limits before work begins.

How Much Cyber Coverage Does a Business Need?

The right limit depends on the size of the business, the type of information handled, contractual requirements, annual revenue, and how much the company depends on digital systems. A small professional services firm may need a different limit than an ecommerce company processing thousands of transactions per month.

When reviewing coverage, consider these questions:

- How many customer, employee, or patient records do you store?

- Do you accept credit card payments or ACH transfers?

- Could your business operate if email, accounting software, or your website went down?

- Do client contracts require specific cyber liability limits?

- Do you use third-party vendors that connect to your systems?

- What would one week of downtime cost in lost revenue, payroll, and customer impact?

Cyber coverage should be reviewed alongside other commercial policies. If you are comparing broader protection, our guide to business insurance costs explains factors that affect pricing across multiple policy types.

Want help comparing limits and policy terms? Request a business liability insurance quote and ask about cyber liability options for your company.

How to Choose the Right Cyber Liability Policy

Choosing cyber insurance is not just about finding the lowest premium. The details determine whether the policy works when a real incident occurs.

- Review first-party and third-party coverage: Make sure the policy addresses both your direct recovery costs and claims from outside parties.

- Check ransomware and extortion terms: Look for sublimits, coinsurance, required security controls, and response procedures.

- Understand the business interruption waiting period: Some policies require a set number of hours before lost income coverage applies.

- Compare breach response resources: Strong policies may include access to forensic firms, legal teams, notification vendors, and crisis support.

- Look at exclusions: Common issues include prior known events, failure to maintain required controls, acts of war, or unsupported systems.

- Match coverage to contracts: If a client requires cyber liability, verify the limit, additional insured wording, and certificate requirements.

- Coordinate with other policies: Cyber insurance should work with your general liability, professional liability, crime, and property coverage instead of leaving gaps.

A licensed insurance agent can help interpret policy language and compare carrier options based on your actual risk profile. InsuranceUnderwriters.com offers access to more than 200 carriers, giving business owners a broader view of available solutions than a single-carrier quote.

What Cyber Insurance Usually Does Not Replace

Cyber liability coverage is important, but it is not a substitute for good security practices. Carriers may ask about controls such as multi-factor authentication, endpoint protection, employee training, backups, encryption, patch management, and vendor access.

Better security can also support better insurance outcomes. Businesses that document controls, train employees, and maintain recovery plans may have more options when applying for coverage. Cyber insurance and cybersecurity should work together: one reduces the chance and severity of an event, while the other helps fund recovery if an event still happens.

How InsuranceUnderwriters.com Helps Businesses Compare Cyber Coverage

InsuranceUnderwriters.com is a licensed insurance brokerage operated by 4 Quotes, L.L.C. The team serves personal and commercial clients nationwide with a broad range of insurance products, including commercial property, business liability, workers compensation, professional liability, business owners policies, and cyber and crime coverage.

For business owners, the value is not just access to a policy. It is guidance through the questions that matter: what coverage applies, which limits are reasonable, how exclusions work, and how cyber insurance fits with the rest of the company’s commercial insurance program.

With 8 professional agents, 43 combined years of experience, more than 1,028 partnership customers, and relationships with over 200 insurance carriers, InsuranceUnderwriters.com can help business owners evaluate options without guessing which policy form is appropriate.

Is Cyber Liability Insurance Worth It for Small Businesses?

Cyber liability insurance is often worth considering for small businesses because one incident can create costs that are difficult to absorb from cash flow. Even a company with a small team can face breach notification expenses, lost income, legal questions, and vendor pressure after a cyber event.

The policy is especially important if your business stores personal information, accepts digital payments, depends on cloud software, uses contractors with system access, or signs contracts with larger clients. In those cases, cyber insurance can protect both balance sheet stability and customer confidence.

Ready to review your commercial insurance program? Contact InsuranceUnderwriters.com for a commercial insurance quote and ask how cyber liability coverage can fit your business in 2026.

Cyber Liability Insurance FAQs

Does general liability insurance cover cyber attacks?

General liability insurance usually does not cover cyber attacks, data breaches, ransomware, or digital fraud. Cyber liability insurance is designed to address many of those technology-related losses.

What is the difference between cyber liability and data breach insurance?

Data breach insurance often focuses on notification, credit monitoring, and response costs after personal information is exposed. Cyber liability insurance may be broader and can include ransomware, business interruption, legal defense, regulatory response, and third-party claims.

How much does cyber liability insurance cost for a small business?

Cyber liability insurance cost depends on revenue, industry, data volume, security controls, claims history, and selected limits. A small professional services firm may pay less than an ecommerce, healthcare, or technology business with higher exposure.

Do small businesses really need cyber insurance?

Many small businesses should consider cyber insurance if they store customer data, accept electronic payments, use cloud software, depend on email, or sign client contracts that require cyber liability limits.

What information do insurers ask for when quoting cyber coverage?

Insurers may ask about annual revenue, number of records stored, security controls, multi-factor authentication, backups, employee training, prior incidents, payment processing, and vendor access.

Key Takeaways

- Cyber liability insurance helps cover digital risks that standard commercial policies may not address.

- First-party coverage pays for your own recovery costs, while third-party coverage responds to claims from others.

- Ransomware, data breaches, business interruption, forensic investigation, and legal defense are common cyber policy concerns.

- Businesses in healthcare, professional services, retail, real estate, construction, technology, and startups often face elevated cyber exposure.

- The right policy depends on your data, revenue, contracts, security controls, and tolerance for downtime.

Digital risk is now part of doing business. The right cyber liability insurance policy can help your company respond faster, recover with less financial strain, and show clients that you take data protection seriously.

Comments

Not found any comments yet.