Group Health Insurance Guide

Learn more about how PEO insurance can help businesses access better coverage.

Group health insurance is one of the most important benefits a business can offer. Whether you employ five people or five hundred, a well-structured group health plan helps you attract top talent, retain key employees, and build a healthier, more productive workforce. This guide covers everything employers need to know about group health insurance, from plan types and legal requirements to cost-saving strategies and Florida-specific considerations.

What Is Group Health Insurance?

Group health insurance is a single health insurance policy that an employer purchases to cover a group of employees and, in most cases, their eligible dependents. Instead of each worker buying coverage individually on the open market, the employer selects one or more plans from an insurance carrier, and employees enroll through the company. Learn more about workers’ compensation insurance.

Because the insurer spreads risk across all members of the group, premiums are typically lower than individual market rates. Group plans also come with guaranteed issue, meaning employees cannot be denied coverage or charged more based on pre-existing medical conditions.

Group health insurance remains the most common way Americans obtain medical coverage. According to the Kaiser Family Foundation, roughly 153 million people receive health benefits through an employer-sponsored plan. For businesses, offering group coverage signals stability, competitiveness, and a genuine investment in employee well-being.

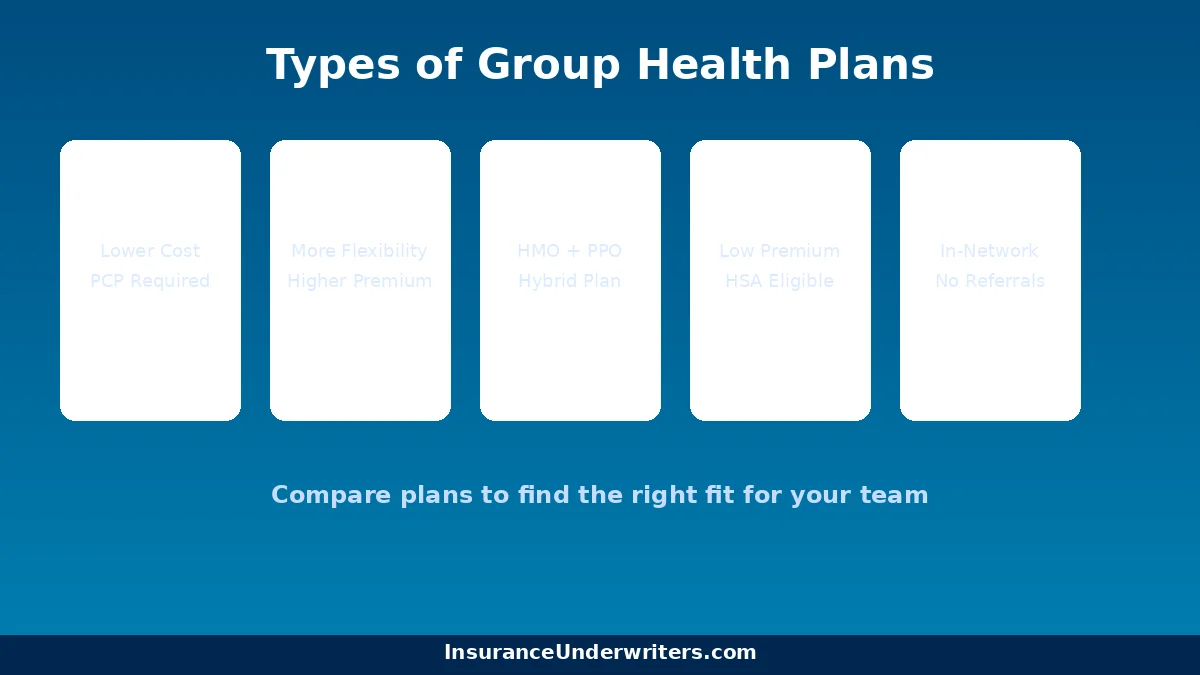

Types of Group Health Insurance Plans

Not all group health plans work the same way. Each plan type balances cost, network access, and flexibility differently. Understanding these distinctions is critical when choosing coverage for your team.

Health Maintenance Organization (HMO)

HMO plans require employees to choose a primary care physician (PCP) from within the plan’s network. The PCP acts as a gatekeeper, meaning employees typically need a referral before seeing a specialist. Out-of-network care is usually not covered except in emergencies.

Pros: Lower premiums and predictable out-of-pocket costs make HMOs attractive for budget-conscious employers and employees.

Cons: Limited provider choice and the referral requirement can feel restrictive for employees who want more flexibility.

Preferred Provider Organization (PPO)

PPO plans offer a broader network of doctors and specialists. Employees can see any provider without a referral, though they pay less when using in-network providers. Out-of-network care is covered at a higher cost-sharing level.

Pros: Greater flexibility in choosing providers and no referral requirements.

Cons: Higher premiums and out-of-pocket costs compared to HMOs.

Point of Service (POS)

POS plans blend features of HMOs and PPOs. Employees select a primary care physician and need referrals for specialists, similar to an HMO. However, they also have the option to see out-of-network providers at a higher cost, similar to a PPO.

Pros: Combines lower in-network costs with out-of-network flexibility.

Cons: Referral requirements and higher out-of-network costs can be confusing for employees.

High-Deductible Health Plan (HDHP) with HSA

HDHPs feature lower monthly premiums paired with higher deductibles. Employees must pay more out of pocket before coverage kicks in, but these plans can be paired with a Health Savings Account (HSA). HSA contributions are tax-deductible, grow tax-free, and can be withdrawn tax-free for qualified medical expenses.

For 2026, the IRS defines an HDHP as a plan with a minimum deductible of $1,650 for individual coverage and $3,300 for family coverage.

Pros: Lowest premiums of any plan type, and HSA tax advantages benefit both employers and employees.

Cons: High deductibles can discourage employees from seeking care, and low-wage workers may struggle with upfront costs.

Exclusive Provider Organization (EPO)

EPO plans operate similarly to HMOs in that coverage is limited to in-network providers. However, EPOs typically do not require referrals to see specialists.

Pros: No referral requirements and lower premiums than PPOs.

Cons: No out-of-network coverage except for emergencies.

Plan Comparison at a Glance

| Feature | HMO | PPO | POS | HDHP/HSA | EPO |

|---|---|---|---|---|---|

| PCP Required | Yes | No | Yes | No | No |

| Referrals Needed | Yes | No | Yes | No | No |

| Out-of-Network Coverage | No | Yes | Yes (higher cost) | Varies | No |

| Relative Premiums | Lowest | Highest | Moderate | Low | Moderate |

| HSA Eligible | No | No | No | Yes | No |

Who Qualifies for Group Health Insurance?

Group health insurance eligibility depends on the size and structure of your business. To offer a group plan, you generally need:

- At least one full-time W-2 employee who is not the business owner or their spouse

- Registered business entity (LLC, corporation, partnership, or sole proprietorship with employees)

- Employees working 30 or more hours per week are typically considered full-time and eligible for coverage

Most insurers require a minimum participation rate, usually around 70% of eligible employees, to approve a group plan. Employers must also contribute a minimum percentage of the premium, typically 50% or more of the employee-only premium.

Eligible dependents usually include spouses and children up to age 26, consistent with Affordable Care Act requirements.

Employer Requirements: ACA Mandates and Compliance

The Affordable Care Act (ACA) created specific requirements for employers based on workforce size. Understanding these rules is essential to avoid penalties and maintain compliance.

Applicable Large Employers (ALEs)

Businesses with 50 or more full-time equivalent employees (FTEs) are classified as Applicable Large Employers. ALEs must offer affordable, minimum-value health coverage to at least 95% of their full-time employees and their dependents. Failure to comply triggers the employer shared responsibility payment, commonly called the “pay or play” penalty.

For 2026, coverage is considered affordable if the employee’s share of the self-only premium does not exceed 9.02% of their household income. The IRS uses safe harbors (W-2, rate of pay, and federal poverty line) to help employers determine affordability.

Small Employers (Fewer Than 50 FTEs)

Small businesses are not legally required to offer health insurance under the ACA. However, employers with fewer than 25 full-time equivalent employees may qualify for the Small Business Health Care Tax Credit, which can cover up to 50% of the employer’s premium contributions.

Reporting Requirements

All employers offering group health coverage must file annual reports with the IRS. ALEs must file Forms 1094-C and 1095-C, while smaller employers providing self-insured coverage file Forms 1094-B and 1095-B.

How Group Health Insurance Costs Work

Group health insurance costs are shared between the employer and employees. Understanding the cost structure helps you budget effectively and design a plan that balances affordability with comprehensive coverage.

Employer Contributions

Most employers pay a significant portion of the premium. According to the Kaiser Family Foundation’s 2024 Employer Health Benefits Survey, employers contribute an average of 83% of the premium for single coverage and 73% for family coverage. For small firms, these averages can vary, but competitive contribution levels are key to attracting and retaining employees.

Employee Contributions

Employees pay their share of the premium through pre-tax payroll deductions, which reduces their taxable income. Beyond premiums, employees also share costs through:

- Deductibles: The amount paid before the plan starts covering expenses

- Copayments: Fixed amounts paid for specific services (for example, $30 for a doctor visit)

- Coinsurance: A percentage of costs shared after meeting the deductible

- Out-of-pocket maximums: The most an employee pays in a plan year before the insurer covers 100%

Average Costs

In 2024, the average annual premium for employer-sponsored health insurance was $8,951 for single coverage and $25,572 for family coverage. Premiums have increased an average of 5-7% annually over the past five years, making cost management a top priority for employers of all sizes.

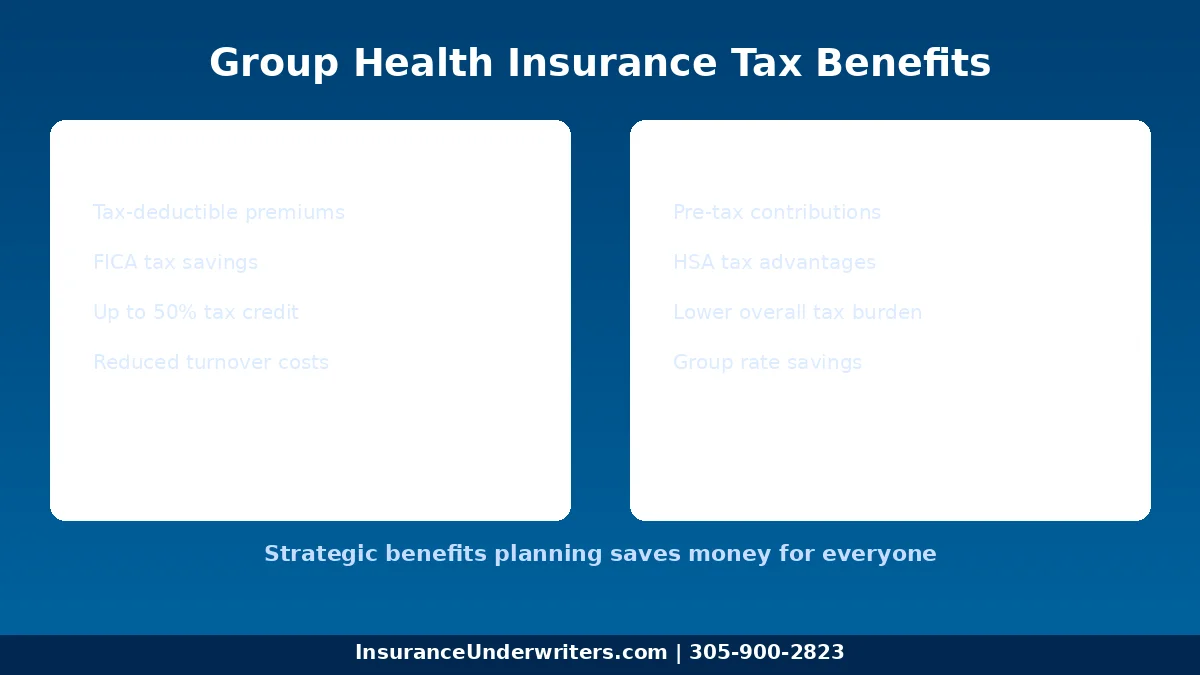

Tax Benefits of Group Health Insurance

Offering group health insurance provides significant tax advantages for both employers and employees.

For Employers

- Premium contributions are tax-deductible as a business expense, reducing your overall tax liability

- FICA tax savings: Employer contributions to group health plans are exempt from Social Security and Medicare taxes

- Small Business Health Care Tax Credit: Employers with fewer than 25 FTEs and average annual wages below $56,000 may qualify for a credit worth up to 50% of premium contributions

For Employees

- Pre-tax premium payments reduce taxable income through Section 125 cafeteria plans

- HSA contributions are tax-deductible, and withdrawals for qualified medical expenses are tax-free

- Lower overall tax burden compared to purchasing individual coverage with after-tax dollars

Self-Funded vs. Fully Insured vs. Level-Funded Plans

Beyond choosing a plan type (HMO, PPO, etc.), employers must also decide on a funding arrangement. Each approach carries different levels of financial risk and administrative responsibility.

Fully Insured Plans

The insurance carrier assumes all financial risk. The employer pays a fixed monthly premium, and the carrier pays all claims. This is the most common arrangement for small businesses because it offers predictable costs and minimal administrative burden.

Self-Funded (Self-Insured) Plans

The employer pays claims directly out of company funds instead of purchasing a traditional insurance policy. Self-funded plans often include stop-loss insurance to cap the employer’s exposure for catastrophic claims. Larger companies with 100 or more employees typically favor self-funding because it offers greater flexibility in plan design and can reduce costs when claims are lower than expected.

Level-Funded Plans

Level-funded plans offer a middle ground. The employer pays a fixed monthly amount that covers expected claims, administrative fees, and stop-loss insurance. If actual claims are lower than projected, the employer may receive a refund. If claims exceed projections, the stop-loss coverage kicks in. Level-funded plans have become increasingly popular among small and mid-sized businesses seeking cost predictability with the potential for savings.

How to Choose the Right Group Health Plan

Selecting the right plan requires balancing your budget, employee needs, and long-term business goals. Here is a step-by-step approach:

1. Assess Your Workforce

Review your employee demographics, including age, family status, and health needs. A younger workforce may prefer HDHPs with HSAs, while employees with families may prioritize comprehensive PPO coverage.

2. Set Your Budget

Determine how much you can contribute toward premiums each month. Consider the total cost of ownership, including premiums, employer contributions, and administrative fees.

3. Compare Plan Types

Request quotes from multiple carriers and compare HMO, PPO, POS, HDHP, and EPO options. Evaluate network size, prescription drug coverage, mental health services, and wellness programs.

4. Review Compliance Requirements

Confirm that your chosen plan meets ACA affordability and minimum value standards if you are an ALE. Ensure proper documentation and reporting procedures are in place.

5. Work With an Experienced Broker

An independent insurance broker can help you navigate the marketplace, negotiate rates, and find plans tailored to your industry and workforce. Insurance Underwriters works with employers across Florida and nationwide to design group health programs that balance cost and coverage.

Benefits Administration: Streamlining the Process

Managing group health insurance involves more than selecting a plan. Enrollment, compliance, claims support, and employee communication all require time and expertise.

Insurance Underwriters offers an AI-powered Benefits Administration platform that eliminates up to 99% of repetitive HR and benefits questions. The platform provides: For more details, see our guide on AI benefits administration tools.

- Real-time concierge support for employees navigating their benefits

- Cost transparency tools that help employees understand their coverage options

- AI-driven navigation that reduces administrative burden on HR teams

- Measurable ROI through improved employee engagement and reduced HR overhead

For businesses looking to consolidate payroll, benefits, compliance, and HR into a single platform, a Professional Employer Organization (PEO) may be the right fit. PEOs handle day-to-day HR administration while giving your employees access to large-group benefits pricing.

Florida-Specific Considerations

Florida employers face unique considerations when offering group health insurance.

State Insurance Regulations

Florida defines small group health plans as those covering 1 to 50 employees. The state requires insurers to offer coverage on a guaranteed-issue basis to all small employers, meaning carriers cannot deny coverage based on health status or claims history.

No State Income Tax Advantage

Florida has no state income tax, which makes pre-tax premium deductions particularly valuable. Employees benefit from federal tax savings on premium contributions without any state tax offset.

Hurricane and Climate Risk

Florida’s exposure to hurricanes and tropical storms can affect employee health and workplace continuity. Comprehensive group health coverage ensures employees have access to medical care during and after natural disasters, supporting faster recovery and return to work.

Provider Networks in South Florida

Employers in the Miami metropolitan area benefit from access to large provider networks, including major hospital systems like Baptist Health, Jackson Health System, and Nicklaus Children’s Hospital. When selecting a group plan, verify that your employees’ preferred providers are in-network.

Frequently Asked Questions

What is the minimum number of employees needed for group health insurance?

Most insurers require at least two full-time employees (including the business owner in some states) to qualify for a small group plan. In Florida, small group plans cover employers with 1 to 50 employees.

How much does group health insurance cost per employee?

Costs vary based on plan type, geographic location, employee demographics, and contribution levels. On average, employers pay approximately $7,400 per employee annually for single coverage. Your actual costs depend on the plan you select and your contribution strategy.

Can part-time employees get group health insurance?

The ACA defines full-time employees as those working 30 or more hours per week. Employers are not required to offer coverage to part-time workers, but many plans allow employers to extend eligibility to part-time employees at their discretion.

What is the difference between group and individual health insurance?

Group health insurance is purchased by an employer and covers multiple employees under a single policy. Individual health insurance is purchased directly by a person through the marketplace or directly from an insurer. Group plans typically offer lower premiums and guaranteed coverage regardless of health status.

Are employer contributions to group health insurance tax-deductible?

Yes. Employer contributions to group health insurance premiums are fully tax-deductible as a business expense. They are also exempt from FICA taxes, providing additional savings.

How does the Small Business Health Care Tax Credit work?

Employers with fewer than 25 full-time equivalent employees and average annual wages below $56,000 may qualify for a tax credit worth up to 50% of their premium contributions. The credit is available for two consecutive years and is claimed on IRS Form 8941.

Next Steps

Choosing the right group health insurance plan is one of the most impactful decisions you can make for your business and your employees. The right coverage attracts talent, reduces turnover, and provides financial protection for your entire team.

Insurance Underwriters specializes in helping businesses of all sizes find group health insurance solutions tailored to their needs and budget. Our experienced team evaluates your workforce, compares carriers, and designs a benefits package that delivers real value.

Get a group health insurance quote today or call us at 305-900-2823 to speak with a benefits specialist.

Comments

Comments are closed.