A Business Owner’s Guide to Product Liability Insurance

Bringing a product to market is a huge accomplishment. But with every sale, you also take on risk. Product Liability Insurance protects your business from financial losses when a product you manufacture, distribute, or sell causes bodily injury or property damage. This isn’t just about defense; it’s about growth. Many retail partners won’t even work with you without it. For any company involved in bringing physical goods to market, this coverage is not just a good idea—it is essential for your success.

Product liability insurance is a core risk management tool for manufacturers, distributors, retailers, and importers. If your business touches a physical product at any point in the supply chain, you need this coverage. Contact Insurance Underwriters at (305) 900-2823 for a product liability insurance consultation tailored to your business.

Product liability insurance is a type of commercial insurance that covers claims arising when a product causes harm. This harm can result from a design flaw, a manufacturing defect, or inadequate warnings and instructions. The coverage pays for legal defense costs, settlements, court-ordered judgments, and medical expenses related to the claim.

Unlike general liability insurance, which covers a broad range of third-party injury and property damage claims, product liability insurance focuses specifically on harm caused by products your business makes, sells, distributes, or repairs. While general liability policies often include some product liability protection under “products and completed operations” coverage, businesses with significant product exposure typically need higher limits or a standalone policy.

In the United States, product liability law operates under a strict liability standard in most states. This means a consumer does not need to prove negligence; they only need to show that the product was defective and caused their injury. That legal framework makes adequate insurance coverage critical for every business in the product supply chain.

Is Product Liability Insurance Right for Your Business?

Product liability insurance is essential for any business involved in the lifecycle of a physical product, including companies that design, manufacture, assemble, distribute, wholesale, import, retail, install, or modify products.

Any business involved in the lifecycle of a physical product should carry product liability insurance. This includes companies that design, manufacture, assemble, distribute, wholesale, import, retail, install, or modify products.

The businesses most at risk include:

- Manufacturers that produce finished goods or component parts

- Distributors and wholesalers that move products through the supply chain

- Retailers that sell products directly to consumers, including e-commerce sellers

- Importers that bring foreign-made products into the U.S. market

- Private label brands that contract manufacturing but sell under their own name

- Food and beverage producers that create consumable products

- Technology companies that produce hardware, electronics, or IoT devices

- Amazon and marketplace sellers that list products on third-party platforms

Even if your business did not manufacture the product, you can still be named in a product liability lawsuit. Under U.S. law, every entity in the distribution chain, from the raw material supplier to the retailer, can share liability. This is why small business insurance should always account for product liability exposure.

If you sell products online, through marketplaces like Amazon, or through retail channels, product liability insurance is a practical necessity. Many retailers and platforms now require proof of coverage before they will carry your products. Get a business liability insurance quote to find the right coverage for your operation.

Common Product Defects That Can Lead to a Lawsuit

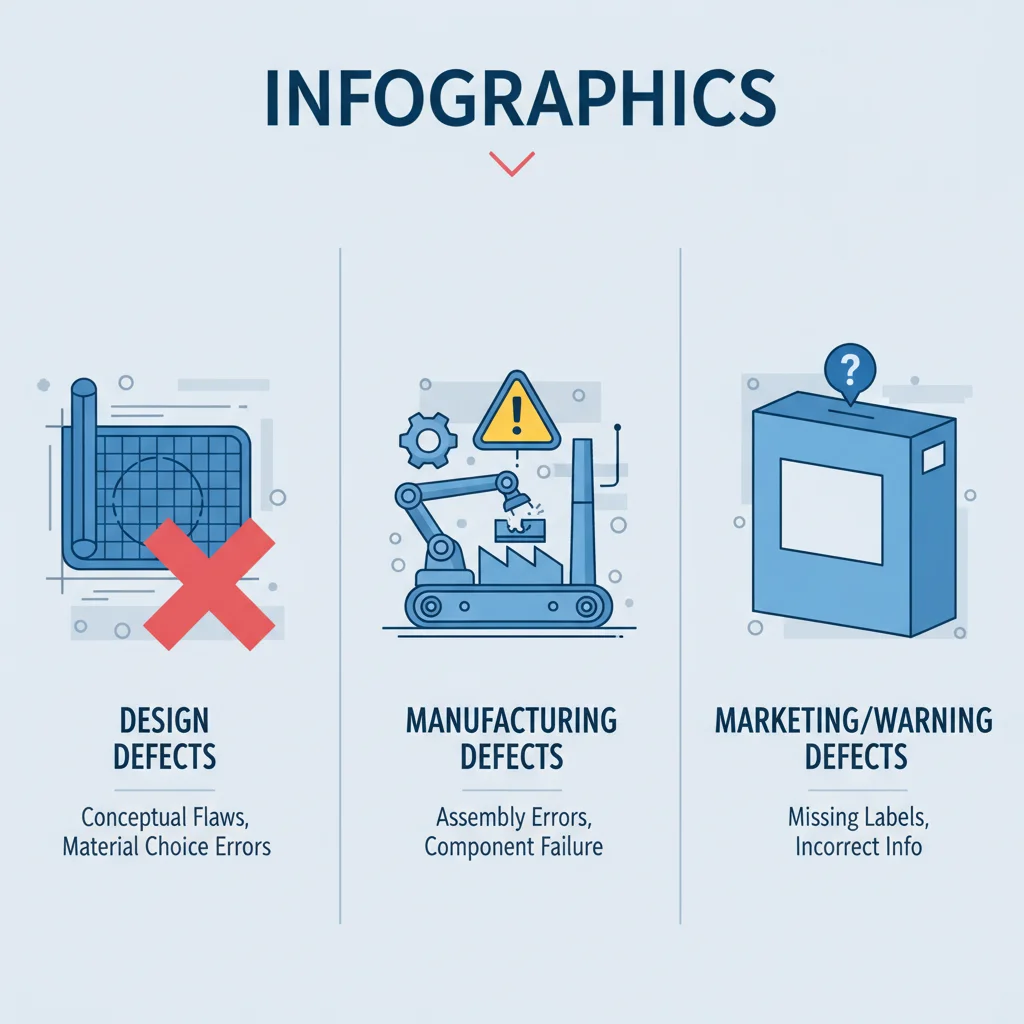

Product liability claims in the U.S. are categorized into three types of defects: design defects, manufacturing defects, and marketing defects (failure to warn). Each type creates distinct legal exposure for businesses in the product supply chain.

Product liability claims fall into three categories recognized by U.S. courts. Understanding these categories helps businesses identify risk areas and implement quality controls that reduce exposure.

When the Product’s Design Is Flawed

A design defect exists when the product’s blueprint or design is inherently unsafe, making every unit produced dangerous regardless of how well it was manufactured. The defect is in the concept, not the execution.

Examples of design defects include:

- A space heater designed without an automatic shut-off when tipped over

- A children’s toy with small detachable parts that pose a choking hazard

- A power tool with an exposed blade guard that allows contact during normal use

- A vehicle with a high center of gravity that makes it prone to rollover

Courts typically evaluate design defects using either the “consumer expectations test” (was the product more dangerous than a reasonable consumer would expect?) or the “risk-utility test” (did the risks of the design outweigh its benefits when a safer alternative existed?).

Mistakes Made During the Manufacturing Process

A manufacturing defect occurs when a product departs from its intended design during the production process. Unlike design defects, manufacturing defects affect only a subset of products, not the entire product line.

Examples include:

- A batch of pharmaceutical tablets contaminated during production

- A structural bolt made with substandard metal alloy

- A food product contaminated with bacteria due to equipment failure

- An electronic device with a soldering error that causes overheating

Manufacturing defects are often the most straightforward to prove because the plaintiff can compare the defective unit to the product’s design specifications or to other units that function correctly.

Inadequate Warnings and Marketing Defects

Marketing defects, also called failure-to-warn defects, occur when a product lacks adequate instructions, safety warnings, or labeling. The product itself may be well-designed and properly manufactured, but the absence of proper warnings makes it unreasonably dangerous.

Examples include:

- A prescription drug that fails to disclose known side effects

- A cleaning product without proper chemical hazard warnings

- A power tool sold without safety instructions for proper use

- A food product that does not clearly label allergens like nuts, gluten, or dairy

Marketing defect claims are particularly common in industries like pharmaceuticals, chemicals, food production, and consumer electronics. Businesses can reduce this exposure through comprehensive labeling, clear user manuals, and visible safety warnings.

What’s Actually Covered by Product Liability Insurance?

Product liability insurance covers legal defense costs, settlements, court-ordered judgments, and medical expenses when a product manufactured, distributed, or sold by your business causes bodily injury or property damage to a third party.

Product liability insurance provides financial protection across several categories of loss. Here is what a typical policy covers:

Costs Your Policy Typically Covers

- Legal defense fees: Attorney fees, court costs, expert witness fees, and other litigation expenses, whether you win or lose the case

- Settlements: Negotiated payments to resolve claims out of court

- Court-ordered judgments: Damages awarded by a jury or judge if you lose the case

- Medical expenses: Costs to treat injuries caused by your product

- Property damage repairs: Costs to repair or replace property damaged by your product

Coverage for Completed Services

Your liability doesn’t always end when the job is finished. This is where products-completed operations coverage becomes essential, as it specifically addresses claims for bodily injury or property damage caused by your work *after* you’ve completed the project. For example, if an HVAC contractor installs a new system that later leaks and causes significant water damage, this coverage would respond to the claim. This protection is a standard feature of most commercial general liability policies, but reviewing your specific limits is critical. It covers both the products you use and the services you perform, providing a crucial safety net for contractors, repair services, and any business whose work has a lasting impact.

Common Exclusions: What Isn’t Covered

It is equally important to understand the exclusions:

- Product recalls: The cost of recalling defective products from the market is not covered under standard product liability insurance. Separate product recall insurance is available for this risk.

- Your own product damage: If your product damages itself, that is not covered. Product liability applies to harm done to third parties or their property.

- Employee injuries: Workers injured by your products during manufacturing are covered under workers’ compensation insurance, not product liability.

- Intentional acts: Deliberate harm or fraud is excluded.

- Professional services errors: Mistakes in professional advice or services fall under professional liability insurance (errors and omissions).

- Contractual liability: Obligations you assumed in a contract are typically excluded unless specifically endorsed.

Understanding these boundaries helps you build a comprehensive insurance portfolio. Most businesses need product liability coverage alongside general liability, commercial property, and possibly cyber liability insurance depending on the nature of their products.

Issues You Already Know About

While your policy is broad, it’s designed for specific risks. It’s helpful to know which common business challenges fall outside its scope, as this clarity is key to building a complete risk management strategy.

Injuries from Improper Product Use

This is the heart of what product liability insurance is for. The policy is your financial shield when someone claims your product caused them bodily injury or damaged their property. The core of any lawsuit will be debating whether the product was defective or if the consumer’s “improper use” was the true cause of the harm. Even if a claim seems baseless, defending your business in court is expensive. Your policy is designed to cover those legal costs, protecting your company from the financial drain of litigation while the facts are sorted out.

Performance Guarantees and Warranties

It’s important to distinguish between a product causing harm and a product simply not working. Product liability insurance does not cover your obligation to repair or replace a faulty item under its warranty. For example, if a commercial freezer you manufacture stops cooling and a client loses their inventory, the warranty might cover the freezer repair, but product liability insurance would not cover the cost of the spoiled goods. The policy is triggered by third-party injury or property damage, not by the failure of your product to perform as promised.

Financial Losses Without Injury or Damage

Product liability insurance is triggered by physical harm. It won’t cover situations where your product causes a customer to lose money without any related bodily injury or property damage. This is often called “pure financial loss.” For instance, if a component you supply fails and forces your client to shut down their production line for a day, their lost revenue isn’t covered by your product liability policy. For those risks, you would need to explore coverage like errors and omissions insurance, which is built for financial losses stemming from professional mistakes or product failures.

Claims of False Advertising

This coverage is about what your product *does*, not what you *say* it does. If a customer sues you because your marketing claims were misleading, that falls under advertising injury—a separate coverage area. This protection is often included in a general liability insurance policy. For example, if your all-natural cleaning product doesn’t disinfect as advertised, that’s a potential false advertising claim. However, if that same product causes a chemical burn due to an undisclosed ingredient, that is a product liability claim.

How Much Does Product Liability Insurance Cost?

Product liability insurance premiums for small businesses typically range from $500 to $3,000 per year for low-risk products, while companies in manufacturing, food production, or medical devices may pay $5,000 to $15,000 or more based on revenue, claims history, and coverage limits.

The cost of product liability insurance varies significantly based on several factors. For small businesses, annual premiums typically range from $500 to $3,000, but companies with higher risk profiles can pay $10,000 or more per year.

Typical Premiums and Potential Discounts

The price you pay for product liability insurance is tailored to your business’s unique risk profile. Insurers evaluate several key factors to determine your premium. These include the type of product you sell (a children’s toy carries more risk than office supplies), your annual revenue, your role in the supply chain, your claims history, and the coverage limits you select. For instance, a manufacturer of high-risk electronics will naturally have a different cost structure than a small retailer selling handmade clothing. The key is understanding that your premium directly reflects your specific level of exposure in the marketplace.

You have more control over your premiums than you might think. Insurers often reward businesses that demonstrate strong risk management. This includes having documented quality control procedures, providing clear warning labels, and maintaining a clean claims history. Working with an experienced broker can also uncover savings, such as bundling your product liability policy with other commercial coverage. A strategic approach to your insurance portfolio can lead to better protection at a more efficient cost. We can help you structure your coverage to align with your risk management goals and secure the most favorable terms.

Factors That Determine Your Insurance Premium

| Factor | Impact on Premium |

|---|---|

| Product type | High-risk products (medical devices, chemicals, food) cost more |

| Annual revenue | Higher revenue generally means higher premiums |

| Claims history | Previous claims increase your premium |

| Coverage limits | Higher limits ($1M vs. $2M per occurrence) raise the cost |

| Deductible amount | Higher deductibles lower the premium |

| Industry | Manufacturing and food production face higher rates |

| Distribution channels | Products sold to consumers directly carry more risk than B2B |

| Quality control measures | Strong QC documentation can reduce premiums |

| Geographic market | Selling in the U.S. is more expensive due to the litigious environment |

Most product liability insurance comes as part of a general liability policy or a business owner’s policy (BOP). Standalone product liability policies are available for businesses that need higher limits or have specialized risk profiles.

Product liability insurance costs depend on your industry, revenue, and risk profile. An experienced broker can help you find the right balance of coverage and cost. Contact Insurance Underwriters to request a customized product liability insurance quote.

Your Company’s Operating History

Insurers review your company’s past to gauge future risk. Your operating history is more than just how long you’ve been in business; it’s the story of your performance and reliability. A history of product liability claims will likely increase your premiums, as it suggests a higher risk of future lawsuits. Conversely, a long, clean record demonstrates stability and strong quality control, which can work in your favor. Underwriters also consider how your business has evolved. For instance, if you’ve moved from distributing products to manufacturing them, your risk profile has changed significantly. An experienced broker can help you present your company’s history clearly and show your commitment to proactive risk management, helping you secure the most favorable terms.

What Happens When a Product Liability Claim Is Filed?

Understanding how a product liability claim works helps you respond quickly and protect your business. Here is the typical claims process:

Step 1: Notifying Your Insurer of the Incident

When you learn that a product has caused injury or damage, notify your insurance carrier immediately. Prompt notification is critical because most policies require timely reporting. Delayed notification can jeopardize your coverage.

Step 2: Investigating the Claim

Your insurer will assign a claims adjuster to investigate. They will gather evidence, interview witnesses, review product documentation, and assess the validity of the claim. During this phase, preserve all relevant records: production logs, quality control reports, safety test results, product designs, and customer communications.

Step 3: Preparing Your Legal Defense

If the claim proceeds, your insurer provides legal defense. This includes hiring attorneys, engaging expert witnesses, and managing the litigation process. Under most policies, the insurer has the “duty to defend,” meaning they cover defense costs even if the claim is ultimately found to be groundless.

Step 4: Reaching a Resolution

Claims resolve through one of three outcomes:

- Dismissal: The claim is found to be without merit

- Settlement: The insurer negotiates a payment to resolve the claim

- Judgment: A court awards damages if the case goes to trial

Essential Documents to Keep on Hand

Strong documentation is your best defense in a product liability claim:

- Product design specifications and engineering drawings

- Manufacturing process records and quality control logs

- Testing and certification reports

- Warning labels and instruction manuals

- Customer complaint records

- Supply chain documentation (raw material sources, component suppliers)

- Insurance certificates and policy documents

Why Proactive Record Keeping Matters

In a product liability claim, your records are more than just paperwork—they are the foundation of your defense. When an adjuster begins their investigation, the first thing they will review is your documentation. Comprehensive records, from initial design specifications and quality control logs to customer communications, create a clear, factual timeline. This paper trail demonstrates a commitment to safety and due diligence, showing that you took responsible steps to create a safe product. Without this evidence, defending against a claim becomes significantly more challenging. Maintaining these files proactively is one of the most effective risk management strategies you can implement, as strong documentation is your best defense when facing litigation.

Product Liability Considerations for Your Industry

Product liability risks vary dramatically by industry. Here is targeted guidance for the sectors that face the highest exposure.

For Manufacturers

Manufacturers face the most direct product liability exposure because they create the product. Key considerations:

- Implement ISO 9001 or similar quality management systems

- Maintain detailed batch and lot tracking records

- Conduct regular product safety testing

- Keep engineering change records that document design modifications

- Carry higher coverage limits, typically $2M to $5M or more per occurrence

- Consider umbrella insurance for catastrophic claims that exceed primary policy limits

The manufacturing sector accounts for a significant portion of product liability claims in the U.S. A single defective component that enters mass production can generate thousands of individual claims, making adequate business interruption insurance equally important for manufacturers.

For Retail & E-Commerce

Retailers can be held liable for products they sell, even if they did not manufacture them. This applies equally to brick-and-mortar stores and online sellers.

- Amazon now requires sellers with more than $10,000 in monthly revenue to carry product liability insurance

- Verify that your suppliers carry their own product liability coverage

- Include hold-harmless and indemnification clauses in supplier contracts

- Private label products carry the same liability as if you manufactured them

- Drop shippers are not immune; you can still be named as the seller of record

For Food & Beverage Businesses

Food producers face unique risks because contamination, allergens, and spoilage can cause immediate and severe harm.

- Follow FDA and state food safety regulations closely

- Implement HACCP (Hazard Analysis Critical Control Points) protocols

- Maintain cold chain documentation for perishable goods

- Label all allergens clearly and completely

- Carry product recall insurance in addition to product liability coverage

- Consider coverage for advertising injury related to mislabeled health claims

For Tech & Electronics Companies

Tech hardware manufacturers face evolving product liability risks, particularly with battery-powered devices, IoT products, and medical technology.

- Battery failures (lithium-ion fires) are a growing source of claims

- IoT devices introduce software-driven defects that may be classified as product defects

- Medical devices face heightened regulatory and liability exposure

- Cybersecurity vulnerabilities in connected products may trigger liability claims

- Software updates that change product behavior can create new liability exposure

- Cyber liability insurance should complement product liability for connected devices

Product Liability vs. General Liability: What’s the Difference?

One of the most common questions business owners ask is whether their general liability policy already covers product liability. The short answer: partially.

General liability insurance typically includes a “products and completed operations” component that provides some product liability protection. However, this coverage is limited in scope and often insufficient for businesses with significant product risk.

| Feature | General Liability | Standalone Product Liability |

|---|---|---|

| Third-party injury | Covered | Covered |

| Product-related claims | Limited coverage included | Primary focus |

| Coverage limits | Shared with other claims | Dedicated limits |

| Legal defense | Included | Included |

| Recall coverage | Not included | Available as endorsement |

| Best for | Service businesses with low product risk | Manufacturers, distributors, retailers |

If your business generates more than 25% of its revenue from product sales, or if you manufacture, import, or private-label products, consider increasing your product liability limits beyond what general liability provides.

How to Choose the Right Product Liability Insurance Policy

Selecting the right policy requires evaluating your specific risk profile. Here are the key considerations:

First, Evaluate Your Business’s Risk Exposure

- What products do you make, sell, or distribute?

- What is the potential severity of harm if a product fails?

- How many units are in the market?

- What quality control measures are in place?

- Have you faced previous claims or complaints?

Decoding Your Policy’s Structure

Once you have a clear picture of your risk exposure, the next step is to understand the mechanics of the insurance policy itself. The fine print matters, and a few key terms can dramatically change how your coverage functions in a real-world scenario. Product liability policies have a specific structure, and knowing how to read it is essential for making an informed decision. Pay close attention to whether your policy is claims-made or occurrence-based, the significance of the retroactive date, and how your deductible impacts both your premium and your financial responsibility when a claim is filed.

Claims-Made Policies

Most product liability policies are written on a “claims-made” basis. This is a critical detail that dictates when your coverage applies. A claims-made policy provides coverage only if the claim is reported to the insurer while your policy is active. This is different from an “occurrence” policy, which covers incidents that happen during the policy period, regardless of when the claim is filed. Because a product-related injury can lead to a lawsuit years after the sale, maintaining continuous coverage with a claims-made policy is crucial to avoid gaps that could leave you uninsured for past work.

The Retroactive Date

Within a claims-made policy, the retroactive date is one of the most important features. This date establishes the starting point for your coverage. Essentially, any wrongful act that gave rise to a claim must have taken place on or after this date to be covered. When you first purchase a claims-made policy, the retroactive date is typically the same as the policy’s start date. If you switch insurance carriers, it is vital to ensure your new policy maintains the original retroactive date. Failing to do so creates a gap in coverage, leaving you exposed to claims from your prior operations.

Deductibles and Excess

Your deductible is the amount of money you are responsible for paying out-of-pocket on a claim before your insurance policy begins to pay. This is a key lever for managing your insurance costs. As a general rule, a higher deductible will result in a lower annual premium. While this can save you money upfront, it also means you assume more financial risk in the event of a claim. Choosing the right deductible is a strategic decision that balances your budget with your risk tolerance. Understanding this trade-off is fundamental to structuring a cost-effective insurance program.

Choose the Right Coverage Limits for Your Needs

Coverage limits for product liability insurance typically range from $500,000 to $5,000,000 per occurrence, with aggregate limits of $1,000,000 to $10,000,000. Your required limits depend on:

- The severity of potential injuries your products could cause

- Your annual revenue and production volume

- Contractual requirements from retailers, distributors, or platforms

- Your overall risk tolerance

Per-Accident vs. Annual Limits (AOA/AOY)

When you review a policy, you will see two key numbers: the “Any One Accident” (AOA) limit and the “Any One Year” (AOY) limit. Think of the AOA limit as the maximum amount your insurer will pay for a single incident, like a batch of contaminated food that causes widespread illness. The AOY limit, on the other hand, is the total amount your policy will pay out for all claims combined within that policy year. It’s your total coverage cap for the year, no matter how many separate incidents occur. Understanding this difference is key to making sure you’re not left underinsured after a single large claim.

How to Choose Your “Any One Accident” Limit

Choosing your “Any One Accident” limit isn’t a guessing game; it’s a strategic risk assessment. The best approach is to consider a worst-case scenario. How much damage could your product cause in a single event? Think about the number of people or properties that could be affected. You’ll need to weigh several factors, including the potential severity of injuries your product could cause, your annual revenue, and how many units you produce. Many retailers and distributors also have contractual requirements that dictate minimum coverage levels. The right limit balances your specific risk profile with the cost of your policy.

Popular Policy Add-Ons (Endorsements)

A standard product liability policy provides a solid foundation, but it may not cover every risk unique to your business. That’s where endorsements, also known as riders, come in. Think of them as specific upgrades that you add to your policy to close potential coverage gaps and build a truly strategic risk management plan. For any business involved with physical products, especially manufacturers, distributors, or retailers, the right endorsements are not just helpful—they are often essential for protecting your business relationships and your bottom line. An experienced broker can help you identify which endorsements are critical for your specific operations, ensuring your coverage is as specialized as your business.

Vendor’s Endorsements

If you sell your products through third-party retailers, distributors, or wholesalers, a vendor’s endorsement is a must-have. This add-on extends your product liability coverage to the vendors who sell your goods, listing them as an “additional insured” on your policy. This is a common requirement from retailers, as it protects them if they are named in a lawsuit related to your product. The coverage applies as long as the vendor sells your product as-is, without modifying it or its original warranties. For any business looking to scale through retail distribution channels, this endorsement is a key part of building strong, lasting partnerships.

Coverage for North American Exports

Selling products across borders is a fantastic way to grow, but it also introduces new risks. Your standard U.S. liability policy may not automatically cover you for claims arising from sales in other countries, including Canada. An endorsement for North American exports is designed to fill this gap. This is particularly important because the legal environments in the U.S. and Canada can be complex and litigious. This add-on helps protect your business when you export products, ensuring a lawsuit from a customer in Toronto is covered just as a claim from a customer in Texas would be.

Why You Should Work With a Specialized Broker

Product liability insurance is complex. An experienced commercial insurance broker understands how to structure coverage that addresses your specific risks. They can access multiple carriers, negotiate competitive premiums, and identify coverage gaps that a direct policy might miss.

Insurance Underwriters specializes in commercial insurance for manufacturing, retail, food production, technology, and other industries with significant product liability exposure. Our team evaluates your entire risk profile to build a comprehensive protection strategy.

Frequently Asked Questions About Product Liability Insurance

What is product liability insurance?

Product liability insurance is a type of commercial coverage that protects businesses from claims when a product they manufacture, distribute, or sell causes bodily injury or property damage. It covers legal defense costs, settlements, judgments, and medical expenses.

How much does product liability insurance cost?

Annual premiums for product liability insurance typically range from $500 to $3,000 for small businesses with low-risk products. Companies in high-risk industries like manufacturing, food production, or medical devices may pay $5,000 to $15,000 or more depending on revenue, claims history, and coverage limits.

Is product liability insurance required by law?

Product liability insurance is not legally mandated in most states. However, it may be required by contract; retailers, distributors, and online marketplaces like Amazon often require proof of product liability coverage before doing business with you.

Does general liability insurance cover product liability?

Yes, most general liability policies include a “products and completed operations” component that provides some product liability coverage. However, businesses with significant product risk should consider higher dedicated limits or a standalone product liability policy.

Who needs product liability insurance?

Any business that manufactures, distributes, imports, retails, or modifies physical products needs product liability insurance. This includes e-commerce sellers, private label brands, food producers, and technology hardware companies.

Product Liability vs. Professional Liability: What’s the Difference?

Product liability covers harm caused by physical products, while professional liability insurance (errors and omissions) covers financial losses caused by professional mistakes, negligent advice, or service failures. A consulting firm needs professional liability; a manufacturer needs product liability.

Find the Right Product Liability Coverage for Your Business

Product liability claims can devastate a business financially. A single defective product can trigger lawsuits that cost hundreds of thousands of dollars in legal fees and settlements, even if your company ultimately prevails in court.

The right product liability insurance policy gives you the financial protection and legal defense to withstand these claims while keeping your business operational. Whether you manufacture goods, sell products through retail or e-commerce channels, or import products into the U.S. market, adequate product liability coverage is a non-negotiable part of your risk management strategy.

Contact Insurance Underwriters at (305) 900-2823 to discuss your product liability insurance needs. Our commercial insurance team works with manufacturers, retailers, food producers, technology companies, and businesses across every industry to build coverage that fits your risk profile and budget.

Key Takeaways

- Liability extends beyond manufacturing: Any business that designs, distributes, imports, or sells a physical product can be held responsible for damages. This coverage is often a mandatory requirement for partnerships with major retailers and online marketplaces.

- Know the difference between liability and performance: Product liability insurance covers claims of bodily injury or property damage, not business risks like product recalls, warranty fulfillment, or purely financial losses. Understanding this distinction is key to building a complete risk management strategy.

- Structure your policy for your specific risks: The right coverage is not one-size-fits-all; it depends on your products, revenue, and sales channels. Key details like coverage limits, policy type, and endorsements must be carefully selected to prevent costly gaps.

Comments

Comments are closed.