Business Owners Policy: What It Is & What It Covers

As a business owner, you know every dollar is an investment. So, let’s talk about one of the smartest investments you can make: a Business Owners Policy (BOP). Think of it as your essential, all-in-one protection package, designed for small and mid-sized businesses. It bundles critical coverage like general liability, commercial property, and business interruption insurance into a single, affordable plan. If you interact with clients or have a physical location, a BOP is the foundation of a solid risk management strategy. Learn more about event insurance. Learn more about liquor liability insurance.

Ready to protect your business with a BOP? Get a free business owners policy quote or call us at 305-900-2823 to speak with an advisor today.

Key Takeaways

- A business owners policy bundles general liability, commercial property, and business interruption coverage into one policy at a lower cost than buying each separately.

- BOPs are designed for small to mid-sized businesses with fewer than 100 employees and under $5 million in annual revenue.

- Typical BOP costs range from $500 to $3,500 per year depending on your industry, location, and coverage limits.

- A BOP does not include workers’ compensation, commercial auto, or professional liability — those require separate policies.

- Insurance Underwriters helps businesses across the United States build comprehensive commercial insurance strategies that start with a BOP and scale as you grow.

For a complete overview of all coverage types available to protect your company, read our small business insurance. Learn more about contractor insurance. Learn more about surety bonds.

What Exactly Is a Business Owners Policy?

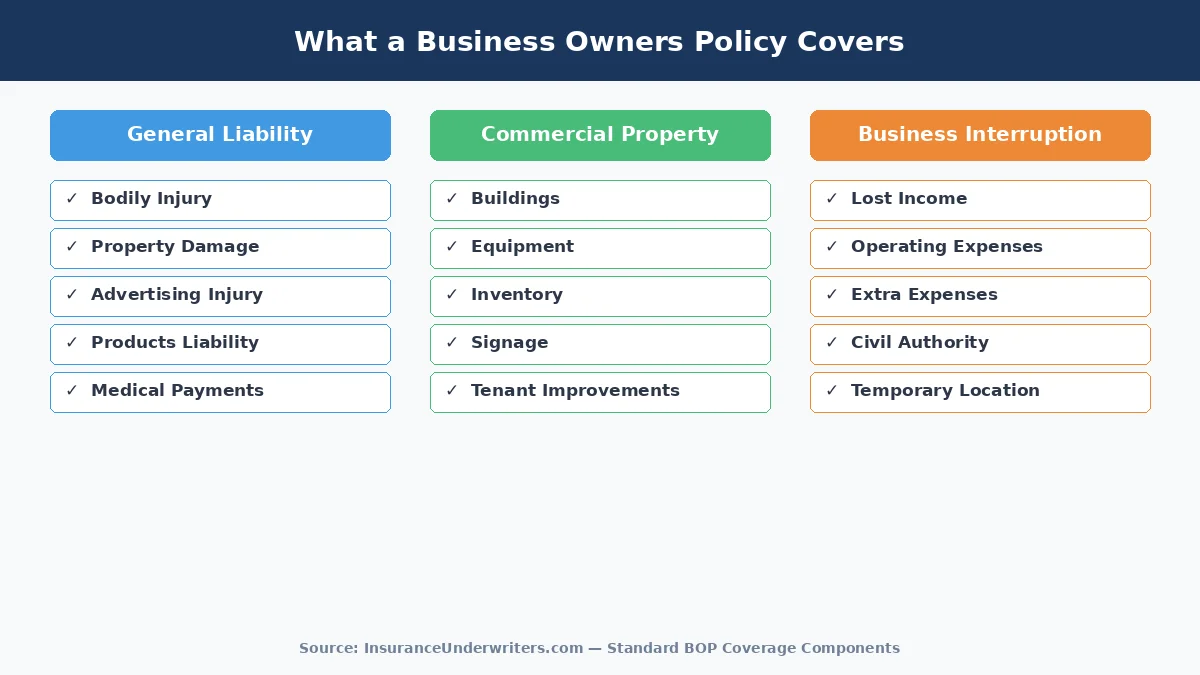

A business owners policy, commonly called a BOP, is a packaged insurance product that bundles two or three core coverage types into a single policy. Insurance carriers designed BOPs specifically for small and mid-sized businesses that need broad protection without the complexity and cost of purchasing each coverage line individually.

The standard BOP includes:

- General liability insurance — covers third-party bodily injury claims, property damage, and advertising injury (such as libel or slander)

- Commercial property insurance — protects your building, equipment, inventory, furniture, and other business-owned physical assets against fire, theft, vandalism, and certain natural disasters

- Business interruption insurance — reimburses lost income and covers ongoing operating expenses when a covered event forces your business to temporarily close

Think of a BOP as a starter package for business insurance. It addresses the most common risks that small business (including LLCs)es face, all in one policy with one premium payment and one renewal date. For many businesses, a BOP provides the same coverage they would get purchasing general liability and commercial property policies separately, but at a significant discount.

The Insurance Services Office (ISO) created the standard BOP form, and most carriers base their policies on it. However, many insurers offer enhanced or customized BOP versions with additional endorsements.

What’s Covered in a Business Owners Policy?

Understanding exactly what a BOP covers helps you evaluate whether it meets your business needs. Here is a detailed breakdown of each coverage component.

Coverage for Everyday Business Risks

The general liability portion of your BOP protects your business when a third party claims injury or damage related to your operations. Specific coverages include:

- Bodily injury — A customer slips on a wet floor in your office and breaks their wrist. Your BOP pays their medical bills and any legal costs if they sue.

- Property damage — Your employee accidentally damages a client’s equipment while performing a service at their location. The policy covers repair or replacement costs.

- Personal and advertising injury — A competitor accuses your business of making defamatory statements in a marketing campaign. Your BOP covers legal defense costs.

- Products and completed operations — A product you sold causes injury after the customer takes it home. Coverage applies to claims arising from your products or completed work.

- Medical payments — Covers minor medical expenses for third-party injuries at your premises, regardless of fault, typically up to $5,000 per person.

Standard general liability limits in a BOP typically start at $1 million per occurrence and $2 million aggregate. Many businesses can increase these limits or add an umbrella insurance policy for broader protection.

Insuring Your Office, Equipment, and Inventory

The property component protects your physical business assets. Coverage typically applies to:

- Buildings you own or are responsible for under a lease

- Business personal property (furniture, equipment, computers, inventory)

- Outdoor signage and fixtures

- Tenant improvements and betterments

- Electronic data and records (limited coverage)

- Valuable papers and records

Property coverage under a BOP usually operates on a “special form” basis, meaning it covers all perils except those specifically excluded. Common exclusions include floods, earthquakes, and intentional damage. You may need separate flood or earthquake insurance depending on your location.

Most BOPs cover property at replacement cost value rather than actual cash value, which means the insurer pays to replace damaged property with new, comparable items without deducting for depreciation.

Standard vs. Special Form Policies

When you look at property insurance, policies generally come in two flavors: “named perils” and “open perils.” A named perils policy, often called a standard or basic form, only covers losses from specific events listed in the policy, like fire or theft. If a risk isn’t on the list, it’s not covered. In contrast, a special form policy provides much broader “open perils” coverage. It protects against all direct physical losses *except* for those specifically listed as exclusions. This is a key advantage, as it shifts the burden of proof from you having to show a loss was caused by a covered event to the insurer having to show it was caused by an excluded one. Most BOPs use this superior special form for their property coverage. Common exclusions you’ll see are events like floods, earthquakes, and intentional damage, which often require separate, specialized policies.

Coverage for When You Can’t Open Your Doors

This is one of the most valuable components of a BOP, and one that many business owners overlook until they need it. Business interruption insurance covers:

- Lost net income — the revenue your business would have earned during the shutdown period

- Continuing operating expenses — rent, utilities, loan payments, and employee wages that continue even while your doors are closed

- Extra expenses — additional costs incurred to minimize the shutdown period, such as renting a temporary location or expediting equipment repairs

- Civil authority coverage — lost income when a government order prevents access to your premises (for example, a road closure after a fire in a neighboring building)

Business interruption coverage activates only when the shutdown results from a covered property loss. If a fire destroys your office and you cannot operate for three months, the policy reimburses the income you lost during that period.

Typical Coverage Duration

The duration of business interruption coverage isn’t a fixed number of days but is tied to what’s known as the “period of restoration.” This is the reasonable length of time it takes to repair, rebuild, or replace your damaged property so you can resume normal operations. The clock starts immediately after the covered physical loss occurs and stops once your business is back on its feet. During this time, the policy covers your lost net income and continuing operating expenses like rent and payroll. Some policies also offer an “extended period of indemnity,” which continues coverage for a set time after you reopen to help your business recover its pre-loss revenue levels. It’s a crucial feature that supports your financial stability even after the physical repairs are complete.

Do You Need a Business Owners Policy?

BOPs are designed for businesses that meet certain eligibility criteria. While each carrier sets its own guidelines, most BOPs target businesses with:

- Fewer than 100 employees

- Annual revenue under $5 million

- Physical premises under 35,000 square feet

- Low to moderate liability risk

Common business types that benefit from a BOP include:

- Retail stores — clothing shops, bookstores, specialty retailers

- Professional offices — accounting firms, consulting agencies, law offices

- Service businesses — cleaning companies, salons, repair shops

- Restaurants and cafes — small food service establishments

- Technology companies — small software firms, IT consultancies

- Nonprofit organizations — charities, community organizations

- Contractors — small construction firms and trade businesses

- Medical practices — small healthcare offices and clinics

If your business operates from a physical location, owns equipment or inventory, and interacts with customers or the public, a BOP almost certainly makes sense as your baseline coverage.

Not sure if a BOP is right for your business? Request a personalized quote or call 305-900-2823 — our advisors will review your operations and recommend the right coverage package.

What a Business Owners Policy Won’t Cover

Knowing the gaps in your BOP is just as important as understanding what it covers. A standard business owners policy does not include:

- Workers’ compensation — Required in most states for businesses with employees. You need a separate workers’ compensation policy.

- Commercial auto insurance — Any vehicles used for business purposes require a separate commercial auto policy.

- Professional liability (E&O) — Claims arising from professional advice, errors, or negligence are not covered. Service-based businesses should consider a separate professional liability policy.

- Employment practices liability (EPLI) — Wrongful termination, discrimination, or harassment claims require separate EPLI coverage.

- Cyber liability — Data breaches, ransomware attacks, and cyber incidents need a dedicated cyber liability policy.

- Directors and officers (D&O) — Personal liability claims against company leadership require separate D&O coverage.

- Flood and earthquake damage — Standard property coverage excludes these perils.

- Employee dishonesty and crime — Theft by employees or third-party crime typically requires a separate crime policy or endorsement.

Many of these exclusions can be addressed through endorsements added to your BOP or through standalone policies. A comprehensive risk management strategy often starts with a BOP and layers additional coverage based on your specific exposures.

Common Policy Exclusions

Beyond the major coverage areas that require separate policies, a standard BOP also contains specific exclusions for certain types of losses. An exclusion is a policy provision that eliminates coverage for a particular risk or cause of damage. Reading the fine print is essential, as these details define the boundaries of your protection. Understanding what isn’t covered helps you implement better risk management practices and identify where you might need specialized endorsements to fill critical gaps in your coverage strategy.

Government Actions and Political Risks

One of the less common but critical exclusions relates to government intervention. A standard business owners policy will not cover losses or damages that result from government actions like confiscation, nationalization, or expropriation. This means that if a government entity lawfully takes control of your business property, your BOP is not designed to cover the financial fallout. While this scenario might seem unlikely for most domestic businesses, it’s a fundamental exclusion that highlights how policies are designed to respond to specific commercial perils, not political or sovereign risks.

Maintenance and Gradual Damage Issues

Insurance policies are built to cover sudden and accidental events, not issues that arise from a lack of upkeep or the natural aging of property. BOPs almost always exclude damage caused by gradual deterioration. This includes problems stemming from pests, mold, rust, normal wear and tear, or poor workmanship. For example, if a leaky pipe goes unfixed for months and causes significant water damage and mold growth, your claim could be denied. This exclusion underscores the importance of proactive maintenance as a core part of your risk management plan.

Workforce-Related Exclusions

This is a crucial point of clarification for any business with a team: a BOP’s general liability coverage does not protect your employees if they get hurt on the job. Liability coverage is for third parties, like customers or vendors. To cover medical expenses and lost wages for work-related employee injuries, you need a separate Workers’ Compensation policy. This is a mandatory coverage in nearly every state, making it a non-negotiable addition to your insurance program if you have even one employee.

Interpreting Policy Language

It’s important to understand how exclusions function within the policy document. An exclusion is a specific statement that carves out certain losses from coverage, even if other parts of the policy seem to imply that the loss would be covered. This is why you can’t just read the highlights; the exclusions define the true scope of your protection. Working with an experienced advisor is key to making sure you fully grasp these details. A thorough policy review can prevent major surprises when you need to file a claim and ensures your coverage aligns with your actual business risks.

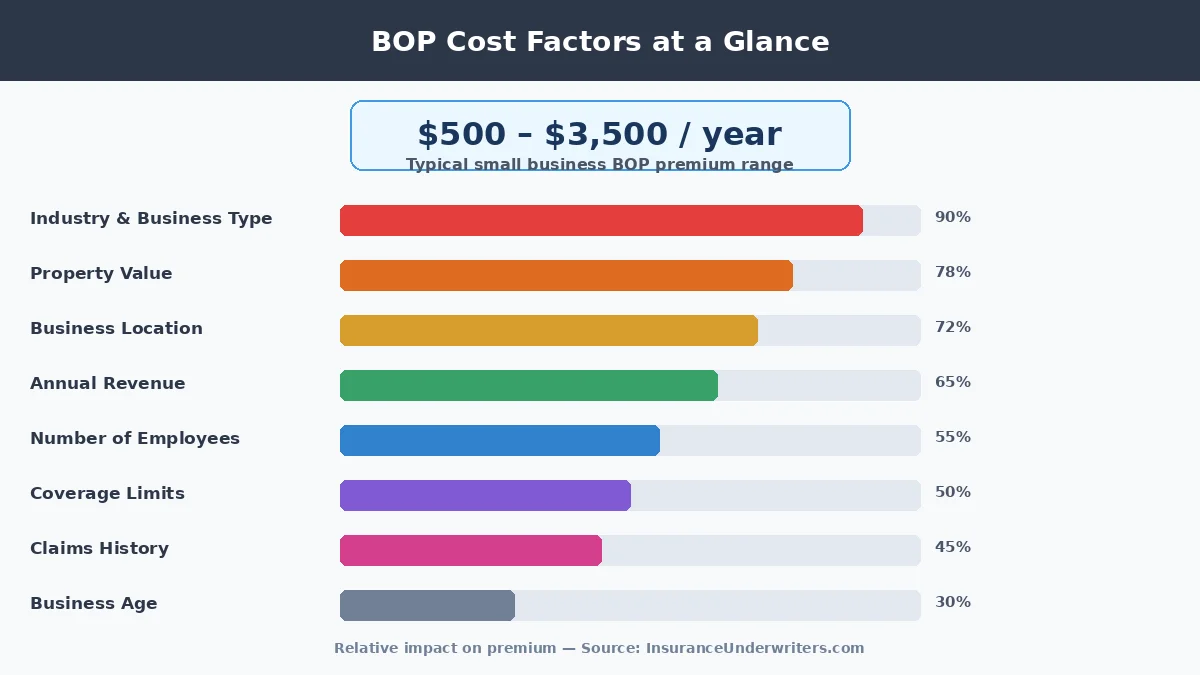

How Much Will a Business Owners Policy Cost?

BOP pricing varies based on several factors, but most small businesses can expect to pay between $500 and $3,500 per year. Here is what drives the cost:

| Cost Factor | How It Affects Your Premium |

|---|---|

| Industry and business type | Higher-risk industries (restaurants, contractors) pay more than low-risk businesses (consulting firms, bookstores) |

| Business location | Urban areas with higher property values and crime rates typically have higher premiums |

| Property value | More valuable buildings, equipment, and inventory increase the property coverage premium |

| Annual revenue | Higher revenue generally correlates with greater liability exposure |

| Number of employees | More employees increase your general liability risk |

| Claims history | Prior claims can raise your premium or limit carrier options |

| Coverage limits | Higher limits and lower deductibles increase the premium |

| Business age | Newer businesses may pay slightly more due to limited operating history |

Understanding Average BOP Costs

While the average cost of a BOP falls between $500 and $3,500 annually, your specific premium depends entirely on your business’s unique risk profile. Think of it this way: a downtown restaurant with expensive kitchen equipment and high foot traffic faces different risks than a solo consulting firm operating out of a small office. Insurers calculate your rate by looking at your industry, the value of your physical assets, your location, and your operational scale, including annual revenue and employee count. A business with more valuable property, higher revenue, or more employees will naturally have greater exposure, which is reflected in the premium. The best way to determine your actual cost is to get a personalized quote that evaluates these specific factors.

Smart Ways to Lower Your BOP Premium

- Bundle additional coverages — Adding workers’ compensation or commercial auto to the same carrier often unlocks multi-policy discounts.

- Increase your deductible — A higher deductible reduces your premium, but make sure you can afford the out-of-pocket cost if you file a claim.

- Implement safety measures — Fire alarms, security systems, and employee safety training programs can qualify you for discounts.

- Maintain a clean claims record — Avoiding claims for three or more years often results in lower renewal premiums.

- Review annually — Your business changes each year. An annual coverage review ensures you are not over-insured or paying for coverage you no longer need.

BOP vs. Other Insurance: What’s the Difference?

Understanding how a BOP compares to other common policies helps you build the right coverage stack.

BOP or General Liability: Which Do You Need?

A standalone general liability policy covers only third-party injury and property damage claims. A BOP includes general liability plus commercial property and business interruption coverage. For businesses that own property or lease space, a BOP is almost always the better value.

Choosing Between a BOP and a CPP

A commercial package policy offers more customization than a BOP. While a BOP is a pre-packaged product with standardized coverages, a CPP lets you select individual coverage forms and limits for each line. Larger businesses or those with complex risk profiles often need a CPP, while small to mid-sized businesses typically find a BOP sufficient.

BOP or Standalone Property Insurance?

Standalone commercial property insurance covers only your physical assets. A BOP adds general liability and business interruption coverage at a bundled price that is usually lower than buying property and liability policies separately.

Finding the Right Business Owners Policy

Selecting the right business owners policy requires evaluating your specific risks and coverage needs. Follow these steps:

Step 1: Understand Your Business Risks

Start by cataloging your business assets, operations, and potential liability exposures. Consider:

- What is the total value of your property, equipment, and inventory?

- How many customers visit your physical location each day?

- What services do you provide, and what could go wrong?

- How long could your business survive without revenue if a disaster forced you to close?

Step 2: Decide How Much Coverage You Need

Match your risks to coverage requirements:

- If you lease space, check your lease for minimum insurance requirements.

- If you have valuable inventory, ensure property limits are adequate.

- If a shutdown would devastate your finances, prioritize strong business interruption limits.

Step 3: Shop Around for Quotes and Plans

Not all BOPs are identical. Compare:

- Coverage forms — Is it a named-perils or special-form policy?

- Endorsement options — Can you add cyber liability, equipment breakdown, or hired/non-owned auto?

- Carrier financial strength — Check AM Best ratings to ensure the insurer can pay claims.

- Claims process — Ask about the carrier’s claims response time and settlement record.

Step 4: Get Expert Advice from a Broker

An independent insurance broker like Insurance Underwriters has access to multiple carriers and can compare BOP options across the market. This ensures you get the best coverage at the most competitive price, rather than being limited to a single carrier’s product.

The Benefit of a Unified Approach

Think of a BOP as the ultimate efficiency tool for your risk management. Instead of juggling multiple policies for liability, property, and business interruption, a BOP combines them into a single, streamlined package. This unified approach means you have one policy to manage, one premium to pay, and one renewal date to track. It simplifies your administrative workload so you can focus on running your business. Beyond the convenience, this bundling strategy is also incredibly cost-effective. Carriers offer discounted rates for BOPs, making it more affordable than purchasing each coverage separately. By addressing the most common risks like fire, theft, and customer accidents in one place, a BOP provides a strong, comprehensive foundation for your company’s protection.

Popular Add-Ons for Your Business Owners Policy

Endorsements let you customize your BOP to address risks that the standard policy does not cover. Popular endorsements include:

- Equipment breakdown — covers mechanical or electrical failure of business equipment (boilers, HVAC, computers)

- Hired and non-owned auto — provides liability coverage when employees drive personal vehicles or rental cars for business purposes

- Cyber liability — adds limited cyber coverage for data breaches and cyberattacks

- Employee dishonesty — protects against financial loss from employee theft or fraud

- Accounts receivable — covers losses when records of amounts owed to you are damaged or destroyed

- Spoilage coverage — essential for restaurants and food businesses to cover inventory loss from refrigeration failure

- Ordinance or law — pays increased costs to rebuild or repair your property to comply with updated building codes

Adding endorsements slightly increases your premium but can prevent significant out-of-pocket costs when uncommon events occur.

How to Get a Business Owners Policy

Securing a BOP involves a straightforward process:

- Gather your business details — legal business name, address, industry classification, annual revenue, employee count, property values, and any existing insurance policies.

- Request quotes from multiple carriers — or work with an independent broker who can shop the market for you.

- Review and compare proposals — pay attention to coverage limits, deductibles, exclusions, and endorsement options, not just the premium.

- Select your policy and bind coverage — once you choose a carrier, you can typically bind coverage within 24 to 48 hours.

- Review annually — business needs change. Schedule an annual review to adjust coverage limits and endorsements.

Insurance Underwriters works with multiple top-rated carriers to find the right BOP for your business. We handle the comparison process so you can focus on running your company.

Frequently Asked Questions

What’s included in a standard BOP?

A business owners policy is a bundled insurance product that combines general liability, commercial property, and business interruption coverage into a single, affordable package designed for small and mid-sized businesses.

What are the core coverages in a BOP?

A BOP covers third-party bodily injury and property damage claims (general liability), damage to your business property and equipment (commercial property), and lost income when a covered event forces your business to close (business interruption).

What factors influence the cost of a BOP?

Most small businesses pay between $500 and $3,500 per year for a BOP. Your exact premium depends on your industry, location, property value, revenue, number of employees, and chosen coverage limits.

How is a BOP different from general liability?

No. A BOP includes general liability insurance plus commercial property coverage and business interruption protection. General liability alone only covers third-party injury and damage claims.

Are there common exclusions in a BOP?

A standard BOP does not cover workers’ compensation, commercial auto, professional liability, employment practices liability, cyber liability, flood damage, or earthquake damage. These require separate policies or endorsements.

Do I need a BOP if I work from home?

If you operate a home-based business that stores inventory, uses business equipment, or receives clients at your home, a BOP may be appropriate. Your homeowners policy likely excludes business-related claims, leaving a coverage gap that a BOP can fill.

Can I customize my BOP with endorsements?

Yes. Most carriers offer endorsements to add coverages like equipment breakdown, cyber liability, hired and non-owned auto, employee dishonesty, and spoilage coverage to your BOP.

For restaurant owners, specialized coverage is essential. Our comprehensive restaurant insurance guide covers every policy your food business needs.

Ready to Find Your Business Owners Policy?

A business owners policy provides the essential protection that every small business needs. It is affordable, comprehensive for most operations, and simple to manage with a single premium and renewal date. But a BOP is just the starting point — your full commercial insurance program should address all the risks specific to your industry and operations.

Insurance Underwriters specializes in building complete coverage strategies for businesses across the United States. From your initial BOP to workers’ compensation, commercial auto, and employee benefits, we help you protect what you have built.

Get your free business owners policy quote today or call 305-900-2823 to speak with an advisor.

For businesses that sell physical products, a BOP may include basic product liability coverage, but manufacturers and retailers with higher risk may need standalone product liability insurance for adequate protection.

Comments

Comments are closed.