Renters Insurance Florida Guide

Florida renters face a unique combination of risks that most tenants in other states never consider. Hurricanes, tropical storms, flooding, and high property crime rates make protecting your belongings more than an afterthought. Renters insurance in Florida covers your personal property, liability, and living expenses when disaster strikes your apartment or rental home.

Get a free renters insurance quote from Insurance Underwriters today and protect everything you own for less than the cost of a streaming subscription.

Renters insurance in Florida is a type of property insurance policy, formally known as an HO-4 policy, designed specifically for people who rent their living space rather than own it. Unlike homeowners insurance in Florida, which covers the physical structure of the building (see our house insurance page for details), renters insurance protects what belongs to you inside the property: your furniture, electronics, clothing, and other personal possessions. It also provides liability coverage if someone is injured in your rental unit and pays for temporary living expenses if your home becomes uninhabitable after a covered event.

What Does Renters Insurance Cover in Florida?

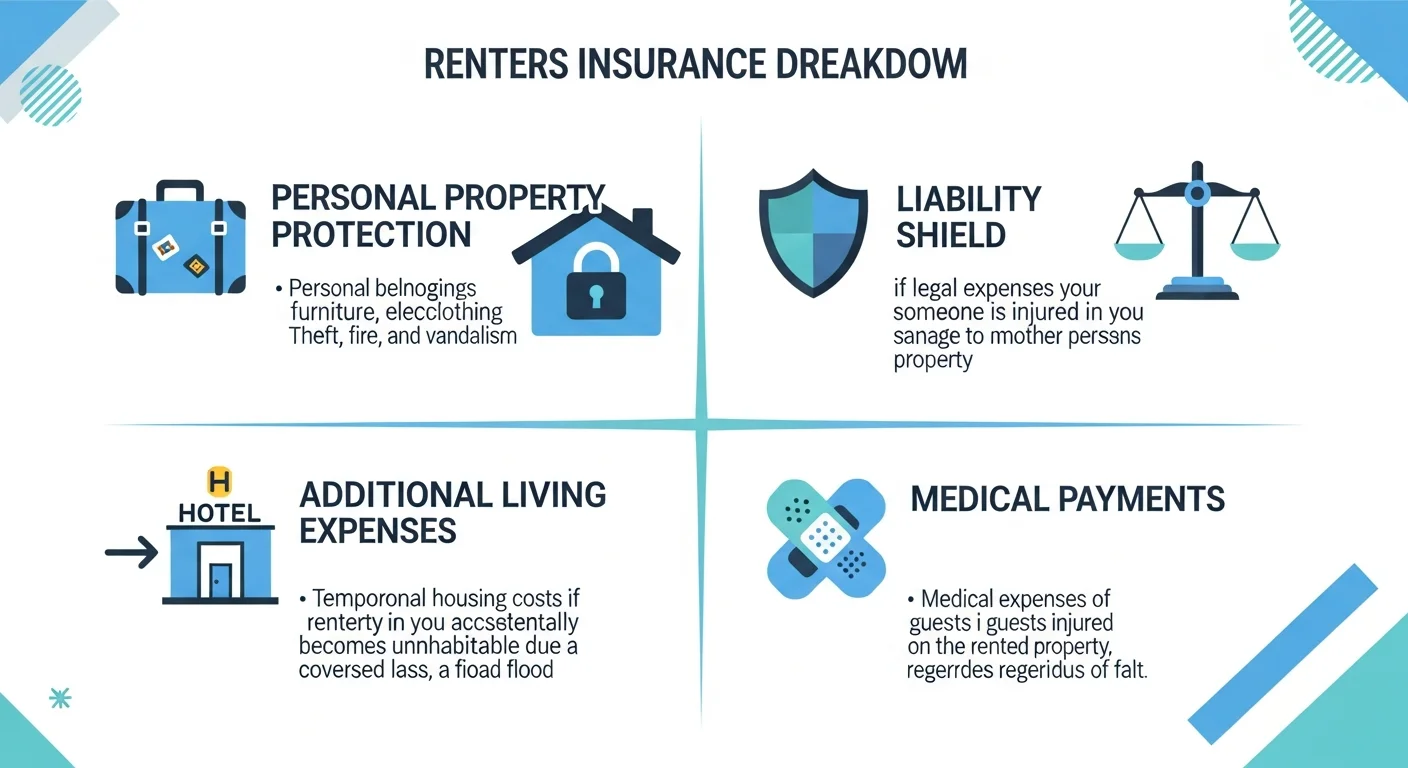

Renters insurance in Florida provides four core categories of protection through a standard HO-4 policy. Understanding each coverage type helps you determine how much protection you actually need.

Renters insurance in Florida is an HO-4 policy that protects tenants’ personal property, provides liability coverage, and pays for temporary living expenses after covered events like hurricanes, fires, and theft. Insurance Underwriters helps Florida renters customize coverage to match the specific risks in their area, from coastal wind damage to inland flooding concerns.

Personal Property Coverage

Personal property coverage is the core of every renters insurance policy. It reimburses you for the cost of repairing or replacing your belongings if they are damaged or destroyed by a covered peril. In Florida, covered perils typically include fire, lightning, windstorm (including hurricanes), hail, theft, vandalism, smoke damage, and water damage from burst pipes or appliance leaks.

Most Florida renters carry between $20,000 and $50,000 in personal property coverage. When choosing your limit, walk through your rental and add up what it would cost to replace everything you own: furniture, electronics, kitchen appliances, clothing, jewelry, sporting equipment, and anything else of value. Many people underestimate this figure significantly.

You will need to choose between two valuation methods:

| Valuation Method | How It Works | Example: 5-Year-Old Laptop ($1,500 New) | Best For |

|---|---|---|---|

| Actual Cash Value (ACV) | Pays current depreciated value | Payout: ~$500 | Lower premiums, budget-conscious renters |

| Replacement Cost Value (RCV) | Pays full cost to buy a new equivalent item | Payout: $1,500 | Full protection, recommended for most renters |

Replacement cost coverage costs slightly more but pays significantly more at claim time. For most Florida renters, the extra $20 to $40 per year is worth the peace of mind.

Liability Coverage

Liability coverage protects you financially if someone is injured in your rental unit or if you accidentally damage someone else’s property. This includes legal defense costs if you are sued. Standard policies start at $100,000 in liability coverage, though many landlords and umbrella insurance advisors recommend $300,000 or more.

Common liability scenarios for Florida renters include a guest slipping on a wet floor, your dog biting a visitor, or water damage from your unit leaking into a neighbor’s apartment below you.

Additional Living Expenses (Loss of Use)

If a covered event makes your rental uninhabitable, loss of use coverage pays for temporary housing, meals, and other necessary expenses above your normal cost of living. In Florida, this coverage is critical because hurricane damage can displace renters for weeks or even months. Most policies cover 20% to 30% of your personal property limit for additional living expenses.

Medical Payments to Others

This coverage pays for minor medical expenses when a guest is injured in your rental, regardless of who is at fault. Limits typically range from $1,000 to $5,000. It is designed to cover small incidents without requiring a liability claim, such as a friend who trips on a loose rug and needs an emergency room visit.

What Renters Insurance Does Not Cover in Florida

Understanding the exclusions in a Florida renters insurance policy is just as important as understanding what it covers. Several major risks that Florida renters face are not included in a standard HO-4 policy.

- Flooding. Standard renters insurance does not cover flood damage. Florida is the most flood-prone state in the country, and even renters who do not live in a designated flood zone can experience flooding from heavy rainfall or storm surge. You need a separate flood insurance policy through the National Flood Insurance Program (NFIP) or a private insurer.

- Earthquake and sinkhole damage. While earthquakes are rare in Florida, sinkholes are a genuine risk in certain areas, particularly Central Florida. Standard policies exclude ground movement. You may need a separate sinkhole endorsement.

- Your landlord’s building. Your renters insurance policy covers your personal belongings and liability, not the physical structure of the building. That is your landlord’s responsibility.

- Roommate’s belongings. Unless your roommate is listed on your policy, their possessions are not covered. Each tenant should carry their own renters insurance.

- High-value items beyond policy sub-limits. Most policies cap payouts for individual categories such as jewelry ($1,500), electronics ($2,500), and fine art ($2,500). If you own items exceeding these sub-limits, you need a scheduled personal property endorsement or a separate floater policy.

- Intentional damage or neglect. Any damage you cause intentionally or through gross negligence is excluded.

- Pest damage. Damage from termites, bed bugs, rodents, or other pests is not covered.

How Much Does Renters Insurance Cost in Florida?

Renters insurance in Florida is remarkably affordable compared to other types of property insurance. The average annual premium ranges from $150 to $300 per year, depending on your location, coverage limits, and deductible. That works out to roughly $13 to $25 per month.

The average cost of renters insurance in Florida ranges from $150 to $300 per year, making it one of the most affordable types of property insurance available. Premiums vary based on location, coverage limits, deductible amount, credit score, and claims history. Miami renters typically pay more than Orlando or Tampa renters due to higher hurricane exposure and property crime rates.

Here is what Florida renters can expect to pay based on location:

| Florida City | Average Annual Cost | Average Monthly Cost | Key Cost Driver |

|---|---|---|---|

| Miami | $199 – $280 | $17 – $23 | Hurricane risk, high property crime |

| Fort Lauderdale | $163 – $240 | $14 – $20 | Coastal wind exposure |

| Tampa | $150 – $220 | $13 – $18 | Moderate hurricane risk |

| Orlando | $140 – $200 | $12 – $17 | Inland location, lower wind risk |

| Jacksonville | $145 – $210 | $12 – $18 | Moderate coastal risk |

| Tallahassee | $130 – $190 | $11 – $16 | Lower overall risk profile |

Several factors directly influence your renters insurance premium in Florida:

- Location. Coastal areas with higher hurricane and flood exposure pay more. Miami-Dade, Broward, and Palm Beach counties have the highest premiums statewide.

- Coverage limits. Higher personal property and liability limits increase your premium proportionally.

- Deductible amount. Choosing a higher deductible ($1,000 vs. $500) lowers your premium but increases your out-of-pocket expense at claim time.

- Credit score. Florida insurers use credit-based insurance scores to set rates. Renters with good credit pay significantly less.

- Claims history. Previous insurance claims can increase your premium for three to five years.

- Pet ownership. Certain dog breeds classified as high-risk can increase liability premiums or result in coverage exclusions.

Do You Need Renters Insurance in Florida?

Florida law does not require tenants to carry renters insurance. However, your landlord or property management company almost certainly does. The vast majority of Florida landlords include a renters insurance requirement in their lease agreements, typically mandating at least $100,000 in liability coverage.

Even if your landlord does not require it, renters insurance is one of the smartest financial decisions a Florida tenant can make. Consider this: if a hurricane forces you out of your apartment and destroys your furniture, electronics, and clothing, you would be responsible for replacing everything out of pocket without insurance. That could easily exceed $15,000 to $30,000 for an average household.

Compare that to paying $15 to $25 per month for a comprehensive policy. The math is overwhelmingly in favor of coverage.

Talk to Insurance Underwriters about customizing a renters insurance policy that fits your budget and protects everything you own.

Renters Insurance vs. Condo Insurance in Florida

Florida tenants sometimes confuse renters insurance with condo insurance (HO-6 policies). While both cover personal property and liability, there are important differences.

| Feature | Renters Insurance (HO-4) | Condo Insurance (HO-6) |

|---|---|---|

| Structure coverage | None (landlord’s responsibility) | Interior walls, floors, fixtures |

| Personal property | Yes | Yes |

| Liability | Yes | Yes |

| Loss assessment | Not typically included | Covers HOA special assessments |

| Average annual cost | $150 – $300 | $500 – $1,500 |

| Who needs it | Tenants renting any property | Condo unit owners |

If you rent a condo unit, you need renters insurance, not condo insurance. The condo association’s master policy and the unit owner’s HO-6 policy do not cover your personal belongings as a tenant.

Florida-Specific Risks Every Renter Should Know

Renting in Florida comes with risks that renters in most other states never face. Understanding these threats helps you build the right coverage strategy.

Hurricane and Windstorm Damage

Florida averages a direct hurricane hit every three years, and tropical storms are even more frequent. Standard renters insurance covers wind damage to your personal property, but many policies include a separate hurricane or windstorm deductible that is higher than the standard deductible. This is typically 2% to 5% of your personal property coverage limit.

For example, if you have $30,000 in personal property coverage and a 2% hurricane deductible, you would pay the first $600 out of pocket before insurance kicks in. Review your policy carefully to understand your hurricane deductible.

Flood Risk

Florida accounts for more flood insurance claims than any other state. As a renter, you can purchase flood insurance through the NFIP or a private insurer. Flood policies for renters typically cost $100 to $300 per year and cover personal property up to $100,000. If you live in a ground-floor apartment or a flood-prone area, this coverage is essential.

Theft and Property Crime

Florida’s property crime rate is higher than the national average, particularly in urban areas like Miami, Orlando, and Jacksonville. Renters insurance covers theft of your belongings both inside and outside your home. If your laptop is stolen from your car or your bicycle is taken from a locked storage unit, your renters policy covers the loss (minus your deductible).

Water Damage

Florida’s high humidity and aging building infrastructure make water damage one of the most common renters insurance claims in the state. Burst pipes, leaking water heaters, and air conditioner condensation overflow are all covered by a standard renters policy. However, gradual water damage from neglected maintenance is not covered.

How to Calculate Your Coverage Needs

Calculating the right amount of renters insurance requires a systematic inventory of your belongings. Follow these steps:

- Room-by-room inventory. Walk through every room and list everything you own. Include furniture, electronics, appliances, clothing, books, kitchenware, and decorations.

- Estimate replacement costs. For each item, note what it would cost to buy a brand-new replacement today, not what you originally paid.

- Total your assets. Add up all replacement costs. This is your target personal property coverage limit.

- Document everything. Take photos or video of your belongings. Store this documentation in the cloud or somewhere outside your rental unit so it survives a disaster.

- Review annually. Update your inventory after major purchases or lifestyle changes.

Most Florida renters find their belongings are worth between $20,000 and $50,000. If you own high-value items like expensive jewelry, electronics, or musical instruments, your total may be higher.

How to File a Renters Insurance Claim in Florida

When disaster strikes, knowing how to file a claim quickly and correctly can mean the difference between a smooth payout and a prolonged battle. Here is the process:

- Document the damage immediately. Take photos and videos of all damaged or stolen items before cleaning up or making repairs. This evidence is critical for your claim.

- File a police report. If your claim involves theft, vandalism, or a break-in, file a police report within 24 hours. Your insurer will require a copy.

- Contact your insurer. Report the claim as soon as possible. Most Florida insurers have 24/7 claims hotlines and mobile apps for filing.

- Provide your inventory. Submit your personal property inventory, photos, and receipts. The more documentation you have, the faster and more complete your payout will be.

- Get repair estimates. If items can be repaired rather than replaced, obtain written estimates from qualified service providers.

- Track all expenses. If you are displaced, keep receipts for temporary housing, meals, and other additional living expenses.

Florida law requires insurers to acknowledge your claim within 14 days and make a decision within 90 days. If you believe your claim was unfairly denied, you can file a complaint with the Florida Department of Financial Services.

Tips for Saving Money on Renters Insurance in Florida

While renters insurance is already affordable, there are several ways to reduce your premium further:

- Bundle with auto insurance. Most insurers offer a 5% to 15% discount when you bundle renters and auto policies.

- Increase your deductible. Raising your deductible from $500 to $1,000 can reduce your premium by 15% to 25%.

- Install safety devices. Deadbolt locks, smoke detectors, fire extinguishers, and security systems can qualify you for discounts.

- Maintain good credit. Florida insurers use credit scores to set rates. A strong credit score can save you hundreds over time.

- Choose a claims-free record. Avoid filing small claims that you can cover out of pocket. A clean claims history keeps your premium low.

- Ask about discounts. Many insurers offer discounts for paperless billing, paying annually instead of monthly, being a non-smoker, or having a protective device.

- Compare quotes. Rates vary significantly between insurers. Get quotes from multiple providers to find the best rate for your coverage needs.

Contact Insurance Underwriters for a free renters insurance comparison and find out how much you could save on comprehensive personal insurance coverage for your Florida rental.

Frequently Asked Questions About Renters Insurance in Florida

Is renters insurance required by law in Florida?

No. Florida does not legally require tenants to carry renters insurance. However, most landlords and property management companies in Florida require it as a condition of the lease, typically with at least $100,000 in liability coverage. Even without a legal mandate, renters insurance protects your finances against theft, fire, hurricanes, and liability claims.

Does renters insurance cover hurricane damage in Florida?

Yes, standard renters insurance covers wind damage to your personal property from hurricanes. However, it does not cover flood damage, which requires a separate flood insurance policy. Most Florida renters policies also include a separate hurricane deductible, typically 2% to 5% of your personal property limit, which is higher than the standard all-peril deductible.

How much renters insurance do I need in Florida?

Most Florida renters need between $20,000 and $50,000 in personal property coverage, at least $100,000 in liability coverage (though $300,000 is recommended), and a loss of use limit equal to 20% to 30% of their property coverage. Conduct a home inventory to determine the exact replacement cost of all your belongings.

Does renters insurance cover my belongings if I live in a flood zone?

Renters insurance covers your belongings against fire, theft, wind, and many other perils, but not flooding. If you live in a flood zone in Florida, you need a separate flood insurance policy. Even renters outside designated flood zones should consider flood coverage, since 25% of flood claims come from low-to-moderate-risk areas.

Can my landlord require me to have renters insurance in Florida?

Yes. Florida landlords can legally require renters insurance as a condition of the lease. For a detailed look at what landlord insurance protects from the property owner’s perspective, see our complete guide. This is a standard practice, and most Florida lease agreements include specific coverage minimums. If your landlord requires it, you must provide proof of insurance, typically a declarations page or certificate of insurance naming the landlord as an interested party.

What is the difference between actual cash value and replacement cost coverage?

Actual cash value (ACV) pays the current depreciated value of your damaged or stolen item. Replacement cost value (RCV) pays the full cost to buy a new equivalent item at today’s prices. RCV policies cost slightly more but provide significantly better payouts at claim time. For most Florida renters, replacement cost coverage is worth the additional premium.

Comments

Comments are closed.